Alphabet (GOOGL) – Earnings Review

Demand

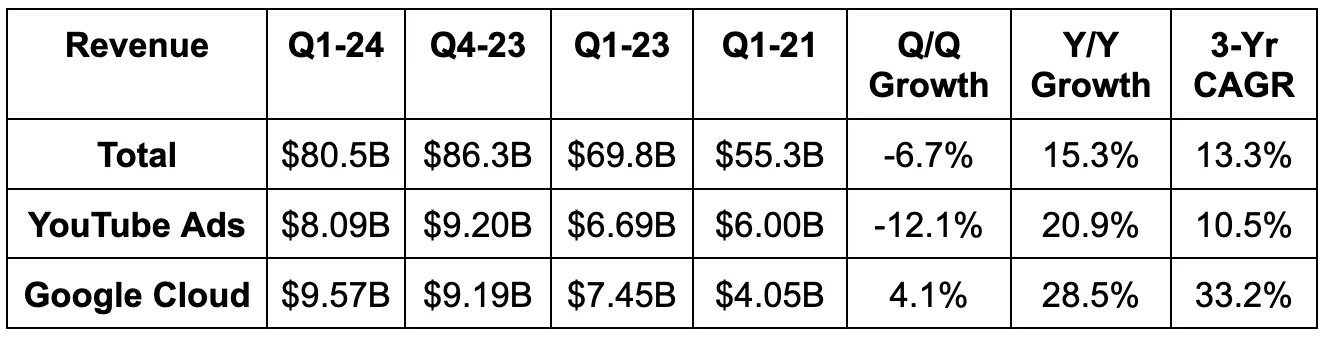

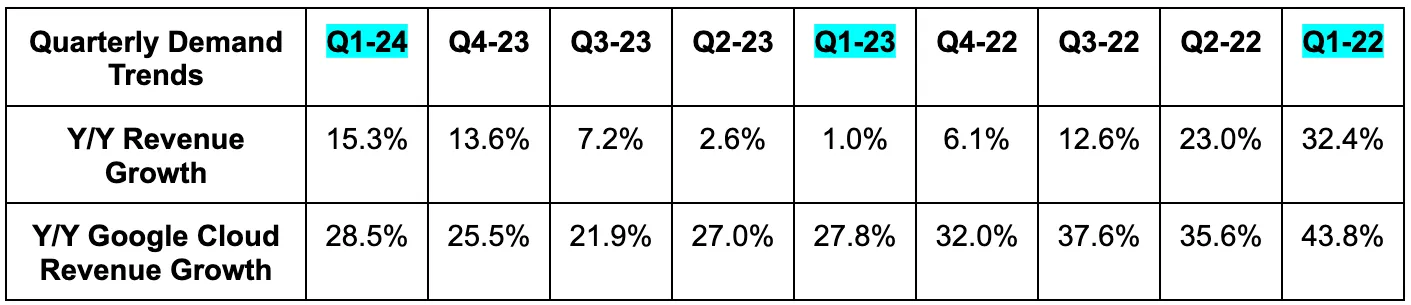

- Beat revenue estimates by 2.3%. Its 13.3% 3-year revenue compounded annual growth rate (CAGR) compares to 14.9% last quarter and 18.4% 2 quarters ago.

- Beat Google Cloud revenue estimates by 3.6%. Strong

- Beat YouTube revenue estimates by 4.9%. Strong again.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Margins & Profits

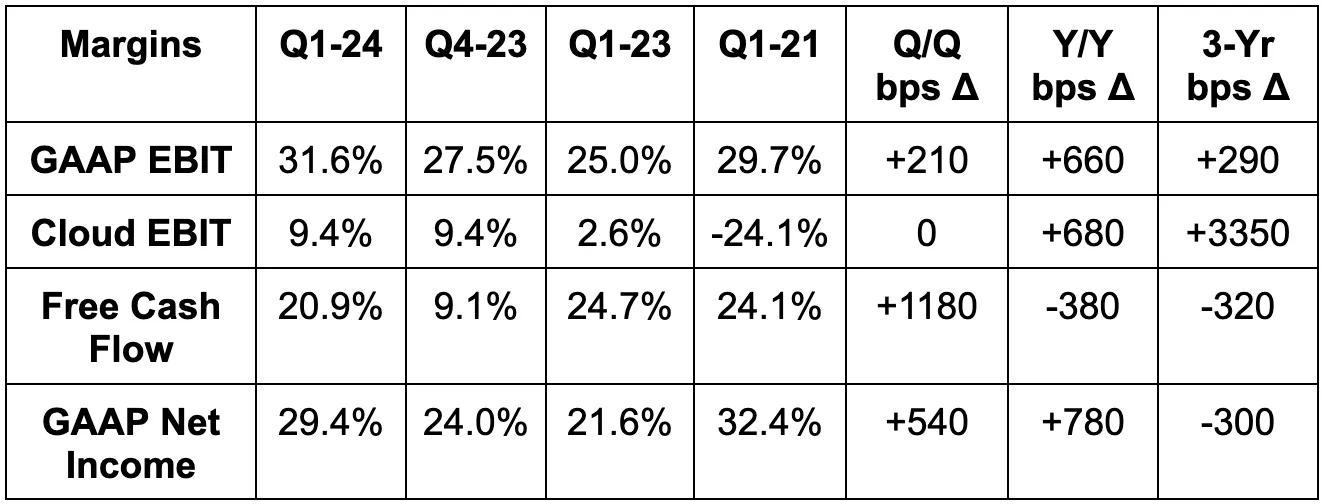

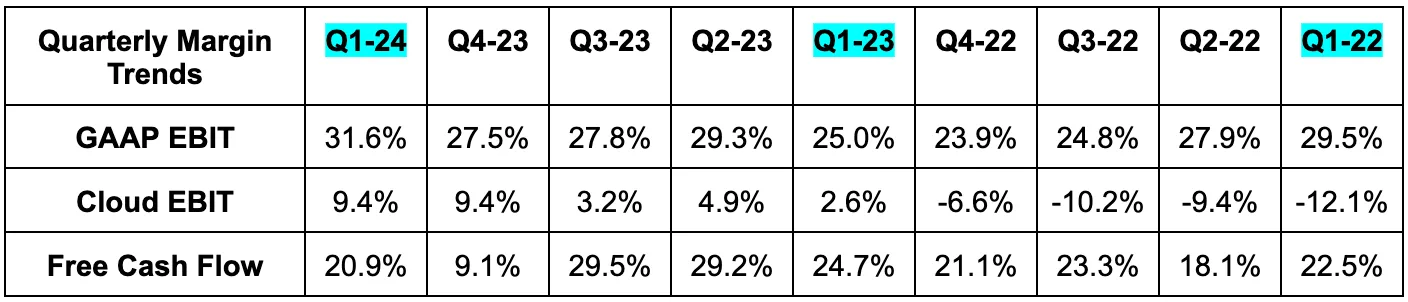

- Beat EBIT estimates by 15%. Rapid EBIT margin expansion was aided by lower severance and real estate charges vs. the Y/Y period. On an apples-to-apples basis, EBIT margin expanded by 390 basis points (bps; 1 bps = 0.01%) Y/Y.

- Operating expenses (OpEx) fell by 2% Y/Y, but would have grown by a modest 5% Y/Y without this help.

- Beat $1.51 GAAP EPS estimate by $0.38.

- Missed free cash flow (FCF) estimates by 9.5% as capital expenditures (CapEx) continued to ramp to support GenAI and cloud infrastructure.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Balance Sheet

- $107B in cash & equivalents.

- $13.2B in longer term debt.

- Share count fell by 2.3% Y/Y via continued stock repurchases. It added another $70 billion in buyback capacity this quarter.

Google also introduced its very first dividend. It’s a modest payout of $0.20 per share, but this does open the company up to more investment demand. Some investment vehicles exclusively invest in dividend-paying stocks.

Guidance & Valuation

Google told us that YouTube and Cloud will combine to exit 2024 with a $100 billion revenue run rate. Aside from that, all that Google offered was that CapEx would stay at or above the $12 billion Q1 2024 level. That’s nearly 100% higher than Q1 2023, as it invests aggressively in infrastructure (like everyone else).

Google trades for 24x 2024 earnings estimates. Earnings are expected to grow by 15% Y/Y for now, but I fully expect some modest upward revisions following the material EPS beat. Other commentary on offsetting rising depreciation expenses will help there too. More on that later.

Call & Release

CEO Sundar Pichai’s 6 Layers of the GenAI Opportunity:

Pichai spent the bulk of his talk diving through what he views as the 6 pieces of GenAI: leading in research, infrastructure and innovation are the first three pieces. Leveraging its global product footprint, execution and monetization areffrom the rest.

To drive faster, more impactful research (and to innovate faster), Google continues to consolidate teams under fewer leaders. It lumped all AI model-building teams into the DeepMind AI research branch. It also combined all machine learning teams and consolidated platform and device groups. The cost efficiency and communication from these moves early on are driving improved product development too. More with less.

Gemini is another instrumental piece in its aim to lead the innovation race. As a reminder, Gemini is Google’s series of foundational models used across its suite of products. The February update to Gemini yielded best-in-class “long context understanding” among other foundational model players. Leading in a key performance benchmark like this bodes well for confidence in Google’s ability to compete in GenAI. Gemini’s multi-modal (can process info from multiple modalities like images and text) models are already being used by several large customers to improve their own workflows and operations.

- Pichai is “pleased with Gemini and Gemini Advanced subscriptions” across app stores.

From a footprint point of view, Sundar sees Google as having the “best infrastructure for the AI era.” Its data centers are “some of the best performing and most secure and efficient in the world.” This architecture has been purpose-built for AI models since Google embraced being an AI first company in 2016. This is allowing it to rapidly debut AI models and algorithms that are enjoying 100x efficiency gains in just 1.5 years. It is committed to “making investments required to stay ahead” – just like we heard from Meta and just like you’ll hear from Microsoft in section 2 of this article. This means continued aggressive chip investments and CapEx staying at or above current levels for the rest of the year. For context, CapEx this quarter rose by 91% Y/Y. Google’s leadership explained this jump just like Meta’s did:

“So the increase in CapEx, as Sundar and I said, really reflects the opportunity we continue to see across the company.” – CFO Ruth Porat

Foundational models are quickly heading toward commoditization. The best way to compete in that future reality is to be the most efficient and lowest-cost provider out there — with the best first-party dataset. Google has the pre-existing scale and data to put it in a great position to lead. But? To keep leading, hefty upfront spend to support seamless and flexible capacity growth is vital. Bottlenecks will otherwise appear. It’s these investments that nurture economies (or queries) of scale and, for example, allow Google to cut search generative experience (SGE) query costs by 80% since inception. SGE directly pulls from Gemini to more conversationally surface answers to queries. Google is now implementing this (as many of you probably noticed) right in the core search process. For appropriate questions, with the help of Gemini, it is now populating answers above links in a conversational fashion. This is awesome for consumers and is already driving engagement and satisfaction gains. I wonder what kind of impact this will have on the media if consumers no longer need to click into other sites for answers to questions.

- Circle to Search (circle a virtual item to essentially activate a direct link) was another example of how Google aims to lead in search.

Advertising (GenAI monetization):

There’s one more piece of Pichai’s GenAI vision to cover: monetization. That, for now, will happen within its advertising business as it improves targeting and campaign management/automation.

Performance Max (PMAX) is Google’s campaign creation service with aggregated impression access. This past February, Gemini was (shockingly) added to PMAX to automate campaign creation and sharpen conversion predictions. Advertisers using PMAX’s asset generation tool are 63% more likely to design a “good or excellent” ad strength campaign; this classification yields a 6% boost to conversions. And if advertisers simply elect to allow Google to deliver automatically created assets (ACA), they’re enjoying another 5% lift to conversion and stable cost per impression. There’s more. Its demand generation product (called Dimension) is being used to uplift customer targeting and retargeting across all Google properties. With this, Lionsgate enjoys a “96% more efficient cost per page view.” Another good example of advertising and GenAI colliding is “Broad Match.” This uses Google’s foundational models to sharpen ad matching. Generally speaking, AI is already directly impacting return on ad spend (ROAS) for Google’s buyers.

Separately, like Meta, Google is enjoying a material boost in advertising revenue from APAC advertisers. This almost surely means Temu. Comps will get tougher with this item in Q3.

“We’re very pleased with the momentum in our ads businesses.” – CFO Ruth Porat.

A Q&A Quote About Investor Doubt Over Google’s Position in GenAI Search:

“But if you were to step back at this moment, there were a lot of questions last year, and we always felt confident and comfortable that we would be able to improve the user experience. People question whether these things would be costly to serve, and we are very, very confident we can manage the cost of how to serve these queries. People worried about latency. We feel comfortable there too. There are questions about monetization. And based on our testing so far, I’m comfortable and confident that we’ll be able to manage the monetization transition here as well. It will play out over time, but I feel we are well positioned. And more importantly, when I look at the innovation that’s ahead and the way the teams are working hard on it, I am very excited about the future ahead.” – CEO Sundar Pichai

Commitment to Efficiency:

Despite plans to keep aggressively leaning into CapEx to support capacity needs, Google reiterated its commitment to efficiency and continuing to optimize its cost base. Combining teams, as already mentioned, is an important aspect of that. While elevated CapEx will mean ramping depreciation expense, CFO Ruth Porat committed to expense discipline offsetting that margin headwind. That was great to hear.

Google Cloud Tools, GenAI & Infrastructure:

The strong revenue result was modestly helped by a larger AI contribution as well as strong Google Workspace usage and revenue per seat growth.

- 90% of GenAI unicorns are now Google Cloud customers as it continues to resonate with that cohort of innovators.

- Debuted Imagen 2.0 — an AI text-to-image generator.

- Debuted Google Vids as an app to easily create short-form video.

- Continued driving advancements in its Axion Central Processing Units (CPUs) and Tensor Processing Units (TPUs) for machine learning.

YouTube:

YouTube Shorts monetization is a big focus area like Reels is for Meta. According to leadership, monetization levels for this content form doubled Y/Y. They also see no reason why it won’t eventually monetize just as well as traditional TV. That would be great news for all short-form video players.

YouTube debuted a “pause ad” format for YouTube TV. This shows brand and performance placements when a viewer pauses a show. So far, the performance of these ads is “commanding premium pricing.” Overall, YouTube TV now has 8 million paid subscribers and reached 1 billion watch hours per day this quarter. Watch time continues to rise for both YouTube TV and Shorts as it leads the streaming race over the past year (per Nielsen). It’s also very pleased with advertising demand momentum for these impressions. Great combination.

- The Q/Q decline in YouTube revenue was due to 1 week of Sunday NFL ticket subscription revenue vs. 14 weeks in the Q/Q period.

- YouTube TV will lap price hikes in May, which will make comps more difficult.

Final Notes:

- Google One crossed 100 million subscribers.

- Waymo is expanding into LA and Austin.

- Google crossed 100 million music and YouTube premium subscribers.

Take

This was a strong quarter. The team is balancing hefty CapEx with strong income statement profit growth; the added context surrounding efficiency gains offsetting depreciation increases is important. The positive commentary on advertising demand bodes well for this company, and basically every other company left to report in the programmatic advertising space. It continues to turn Google Cloud into another quickly growing business with ample operating leverage. It continues to rapidly iterate in GenAI search. And? It continues to be one of the most iconic performers of the 21st century. Congratulations to shareholders on more profitable compounding.