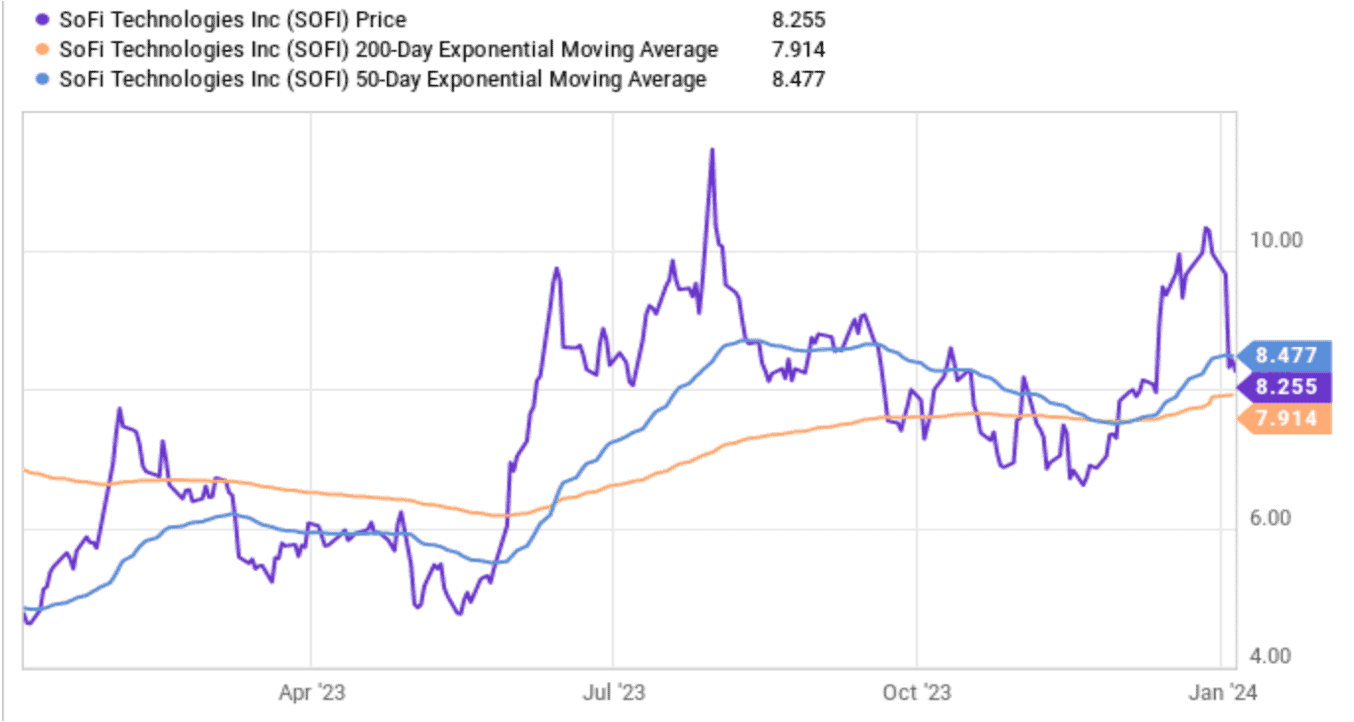

SoFi Technologies (SOFI) – Downgrade – January 5, 2024

Keefe, Bruyette & Woods (boutique research firm) downgraded SoFi this past week. It lowered its price target from $7.50 to $6.50. There are a few reasons for this. The first one is its recently positive stock movement leading to more downside stock risk. This is irrelevant and I don’t want to lend credence to this argument with further explanation. The other factors are what we need to focus on.

The firm sees a risk of lower fair value on incremental originations. This is due to falling rates leading to SoFi charging lower annual percent rates (APR). This entirely ignores multiple pieces of fair value measurement. It penalizes SoFi for lower APR WITHOUT rewarding future fair value for lower cost of capital and stellar loss rates. All three are variables in arriving at fair value.

Let’s dissect the APR and cost of capital pieces. SoFi has a unique FinTech edge (thanks to the charter) in its ability to use low-cost deposits for originations. This means lower cost of capital than those reliant on warehouse credit. SoFi also enjoys significant pricing power in its APR/weighted coupons. Why? Because of its excess credit demand and ultra-prime borrowers. It turns down 75% of applicants and enjoys heightened elasticity of demand from catering to the most affluent borrowers. The luxury of extreme selectivity helps too. That’s why its weighted average coupon rose faster than benchmark rates throughout 2022-2023. That’s also why its weighted average coupon will likely fall more slowly than rates during the dovish part of this cycle. So… structural cost of capital advantage and a structural weighted coupon advantage. This puts it in an ideal position, along with great loss rates, to maintain or even grow fair value of loans going forward.

There’s another vital point to cover. The fair value of loans is also based on the present value of the discounted cash flows of future repayments. As rates fall, that discounting becomes less intense. This directly props up fair value to offer more maintenance support.

The analyst also sees lower origination growth in 2024 as a risk. I agree that origination growth will slow, but not nearly as much as this firm implies in its revenue forecast. Why? Lower rates and easier monetary policy mean tighter credit spreads, better liquidity and more capital market demand. SoFi uniquely found capital market buyers at compelling gain on sale margin throughout 2022 and 2023 thanks to its pristine credit performance; it should find far more demand in 2024. That will mean more pocketed gain on sale margin, and more balance sheet flexibility to accelerate originations without approaching capital ratio minimums. It will also mean lower profit hurdle rates for capital market participants like hedge funds to clear. This could even potentially bolster its already strong gain on sale trends.

Separately, personal loan demand does fall with falling rates. That is 100% accurate. Most of this credit bucket is from refinancing variable credit to fixed rate credit. There’s little incentive to do that as rates fall. Still, that’s fully baked into leadership’s expectations of compounding revenue at 20%-25% in the years to come. Furthermore, this is exactly why SoFi being a one-stop-shop is so compelling. While falling rates hit personal lending demand, they bolster demand for student and home lending. Some will say student lending is not as attractive as personal because of the lower coupon rates. But this credit boasts significantly lower loss rates. It also comes with lower customer acquisition cost considering SoFi is the share leader here, with its brand still associated with student lending for many. For home lending, the company has gotten its tech stack and service levels to a good place right in time for the fun part of the cycle to commence. It also has a very large base of customers to cross-sell these products to, which it didn’t have during the last rate cut cycle.

Next, the firm cites SoFi’s premium book value multiple. They’re not wrong here, but book value is not the best multiple for this firm. It’s not just a bank. It’s a bank, a financial wellness company and a financial API vendor. As I’ve said before, we’ve had to use EBITDA in the past due to a lack of GAAP net income. Well? That GAAP net income is coming. Even if it ramps a bit more slowly than I think it will, the firm’s forward PEG is solidly below 1x. That is not expensive.

The analyst calls out risks to SoFi meeting its path to profits. Considering the team’s perfect track record of under-promise, over-deliver, this would mark a sharp break from current trends. The team gave zero indication of risks to Q4 guidance or 2024 profit guidance during its shareholder Q&A on December 4th. That was about 70% of the way through its calendar quarter.

Finally, the analyst has 2024 revenue estimates a full 9% below consensus. We now have nearly 3 years of SoFi effectively setting street expectations to be comfortably surpassed. I don’t find it realistic to think that as the backdrop gets easier, that trend will suddenly halt. It would be like expecting Mike Trout to only be good against major league pitching and to suddenly stink against minor leaguers. But let’s entertain this thought for a second.

Assume that lending remains around 68% of total revenue for 2023 and that it does $1.41 billion from that segment for the year. Then pessimistically assume 0% lending growth in 2024 despite easier policy, ramping home lending and the expectation to grow originations next year. To get to the firm’s $2.3 billion 2024 revenue estimate, the other two segments would need to grow to $890 million. Assume the company falls short on its objective to accelerate the tech platform to mid-teens growth in 2024 and only delivers 10% growth. That means about $405 million in tech platform revenue for 2024. That means financial services would need to contribute $485 million for 2024. That represents a slowing of revenue growth from 188% to 62% as the backdrop gets immensely easier for these products. Again, this assumes disappointment from its other two segments which is not what I expect. Yeah… I’ll take the over.

There are clearly risks to the bull case. Stock volatility and fair value risk as rates fall are not pressing risks in my view. Fair value was more vulnerable as rates rose, yet SoFi’s coupon elasticity of demand prevented that risk from coming to fruition. I expect a great Q4 and upbeat 2024 guidance. I could always be wrong.

Source: YCharts