Sea Limited (SE) – Earnings Review – Q3 2023

Demand

Sea Limited beat revenue estimates by 3.1%.

Please note that the financial services 3-yr CAGR is comping vs. a base period in which revenue was close to $0. This makes the comp overly easy and not important

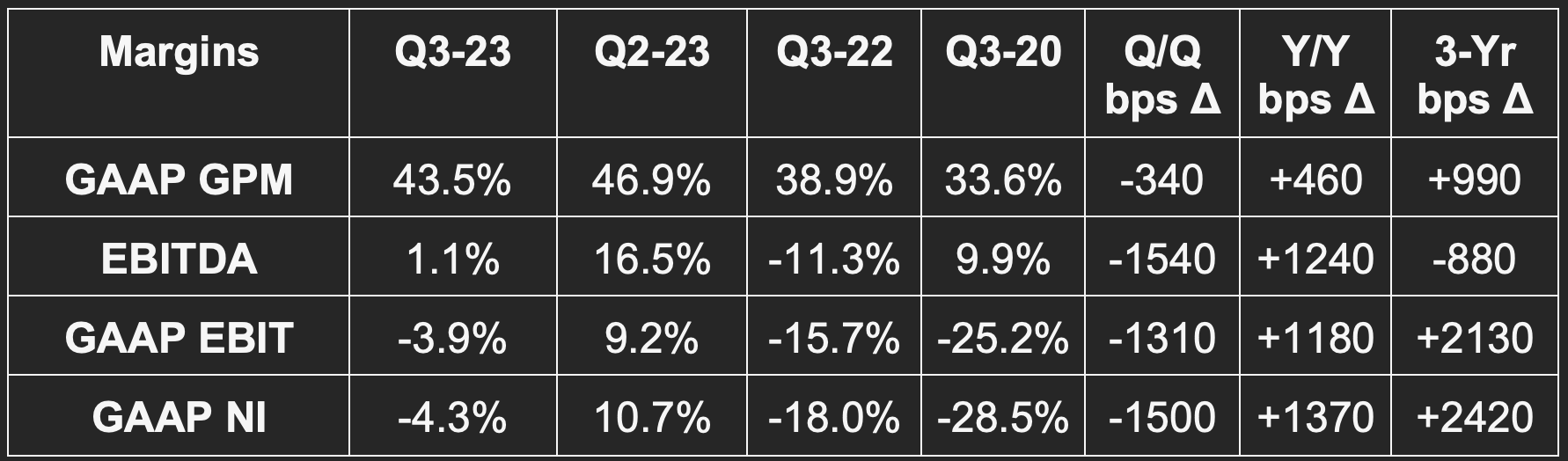

Margins

- Missed $180 million EBITDA estimates by $145 million.

- Missed -$55 million GAAP EBIT estimates by $72 million.

- Missed $0.00 GAAP earnings per share (EPS) estimates by $0.26.

- Missed 44.5% GAAP gross profit margin (GPM) estimates by 100 basis points (bps; 1 bps = 0.01%).

Most of the Y/Y leverage was from 30%+ declines in general/administrative and research/development costs.

Balance Sheet

- $6 billion in cash & equivalents. Including other investments & restricted cash, it has $7.9 billion in total liquidity.

- $800 million in debt.

- $3.3 billion in convertible notes.

- Share count rose by 1.4% Y/Y. Diluted share count rose by 7.0% Y/Y.

Call & Release Highlights

The Balancing Act

Earlier in the year, Sea Limited pivoted in its operational approach. It went from a philosophy that predominantly sought more revenue to one that balanced future growth with current profit. The macro backdrop changed, and so Sea Limited changed too.

It fixated on “self-sufficiency” and funding operations without external cash raises. It strengthened its balance sheet and streamlined operations significantly. The recent explosion in margins is the result. You’ll notice, however, that the sequential margin trend turned materially negative this quarter. This is intentional. With SE now on firmer footing, it’s ready to re-accelerate growth spend. It will not return to its 2020-2021 spending philosophy, but it will lean back in a bit.

The catch 22 is that investors want profits, and massive e-commerce footprints need massive scale to generate those profits. So? It’s pushing forward with scaling its under-penetrated markets, but with more fiscal responsibility than in the past. Balance. As an aside, live streaming was called out as a significant focus area for supporting future growth.

E-Commerce

Core marketplace revenue rose 31.7% Y/Y compared to 37.6% Y/Y growth last quarter. Value added services revenue rose by 4.2% Y/Y compared to 11.3% Y/Y growth last quarter. Interestingly, its rightsizing of logistics is negatively impacting value added service growth. Gross orders rose by 13.2% Y/Y to foster 5.1% Y/Y gross merchandise value growth. It believes that it took more market share in all of its geographies this quarter.

EBITDA margin for the segment was about -16% vs. roughly 7% Q/Q and -26% Y/Y. This is the effect of its re-accelerating growth spend. I’d love to see the coinciding margin contraction complemented by accelerating growth, but it’s likely too early to expect that.

Part of its recent shift to a profit-focused strategy is based on competition. Per the team, new entrants are intensifying that competition. It wants to support the e-commerce business with needed investments to ensure it maintains a strong category position. It seems that SE can support these investments while getting more efficient simultaneously. For evidence, cost per order fell 17% Y/Y.

Live Streaming

Within e-commerce, it’s pushing heavily into live content streaming to juice market engagement. Shopee live, the streaming platform, is greatly expanding creator collaborations. This is already working in Indonesia where 20% of its daily platform users are watching live streaming. Overall, average daily streamers, hours streamed, and daily sessions rose by 300% from June to October.

Logistics Investments

SE continues to build more sort centers and enhance its last-mile delivery coverage across all markets. Specifically, the firm is enjoying strong growth in Brazil with improving unit economics there as well. It continues to build out its footprint in that region and those investments continue to bear fruit.

Digital Entertainment

- Quarterly active users and payers continued to fall Q/Q. Payer ratio also continued to fall.

- Garena bookings specifically rose Q/Q with quarterly active users and EBITDA stable Q/Q.

- Free Fire was the most downloaded game in Q3 across the globe per Sensor Tower. The firm upgraded Free Fire in an attempt to make it more social.

- EBITDA was 52.2% of bookings vs. 54% Q/Q.

Financial Services

Its credit portfolio overall rose 5% Q/Q to $2.9 billion. This includes $500 million in loans from other financial institutions through its platform. The credit book “stayed healthy” per the team. Specifically, the rate of non-performing loans (NPL) 90+ days due improved sequentially to 1.6% of gross receivables. Rate of loans 30+ days past due also improved Q/Q. Finally, the firm is actively expanding funding supply sources to lower overall cost of capital. Its own deposits and asset backed lending deals with 3rd parties are the two main examples.

StockMarket Nerd’s Take

Fine quarter. This company remains in “prove it” mode. The cost cutting to prop up margins is nice, but it will need to reignite spending (like it’s starting to do) to juice demand. That spending must result in growth rather than another instance of costs spiraling out of control. With ramping competition across all of its markets, it’s unclear how sticky its business truly is. Can they keep cutting costs while taking share, re-accelerating demand and expanding margins? I’m not sure. That’s what needs to happen for this to work.

Step one was right-sizing the cost base. To the firm’s credit, it completed this step very quickly. Now onto step 2.

To see the complete earnings report, check the SEC filings here.