Progyny (PGNY) – The Stock Market Nerd’s Q3 2023 Earnings Review

Demand

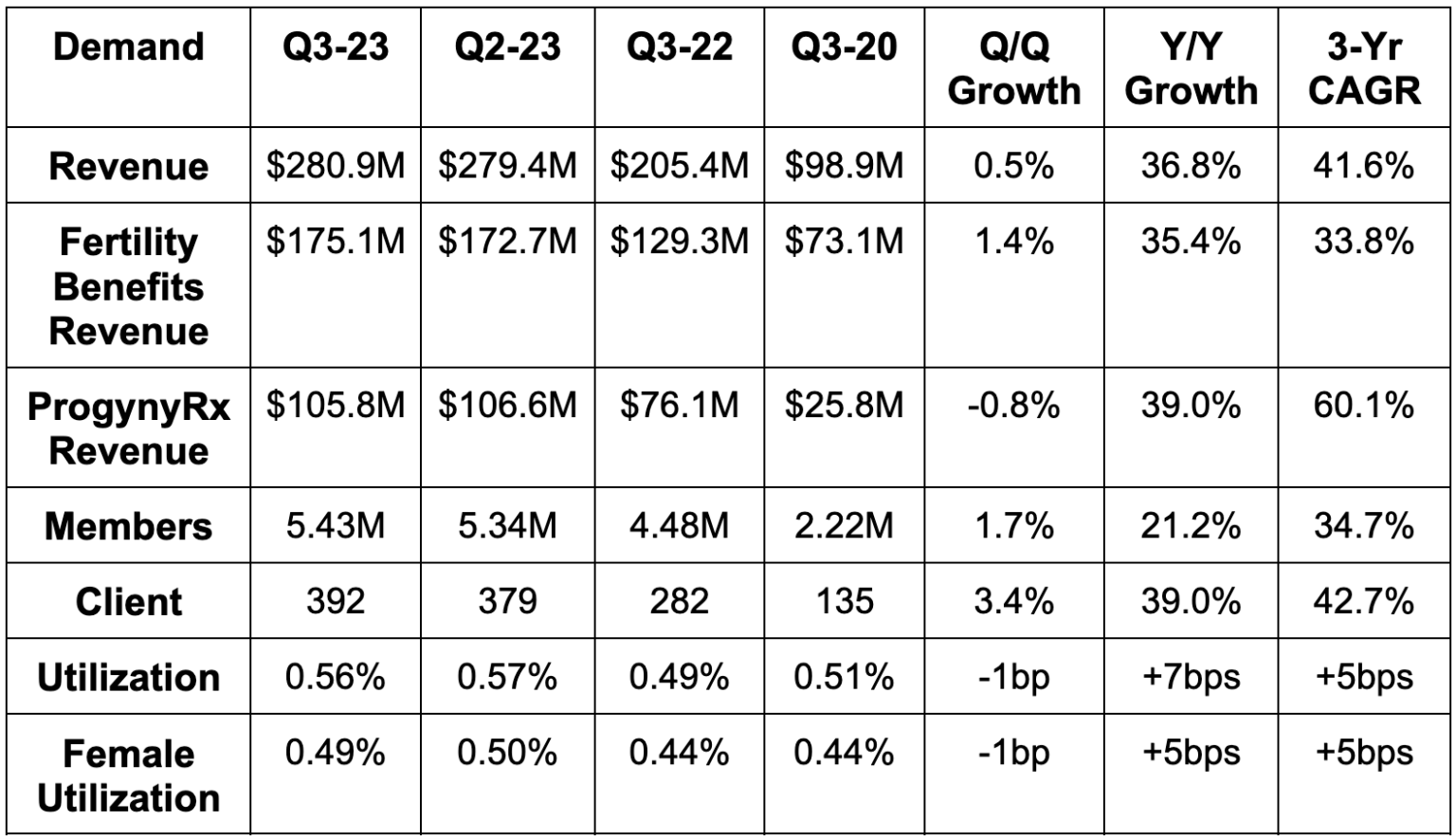

Progyny beat revenue estimates by 3.5% & beat guidance by 3.8%. Its 41.6% 3-year revenue CAGR compares to 62.9% Q/Q & 47.2% 2 quarters ago.

Note that member growth experienced a uniquely tough comp. In Q3 2022, Progyny added an abnormally large chunk of early covered lives in the range of 250,000. This threw off typical seasonality for the quarter.

Profitability

- Progyny beat EBITDA estimates by 8.9% and beat its EBITDA guidance by 9.9%. It also beat GAAP earnings before tax (EBT) estimates by 42%.

- Its incremental EBITDA margin was 19.9% vs. 17.3% Q/Q & 21.7% Y/Y. This directly points to more leverage ahead.

- Its $0.16 in GAAP earnings per share (EPS) was $0.05 ahead of estimates and $0.07 ahead of its guidance.

- EPS and net income rose by 23.1% Y/Y despite a $5 million tax charge vs. a $1.7 million tax benefit in the Y/Y quarter. With the same tax impact Y/Y, EPS would have risen by 71% Y/Y.

Guidance

Progyny’s Q4 guidance was 0.8% light on revenue and 5% light on EBITDA. It was in line with estimates on GAAP EPS. Importantly, full year guidance was raised across the board. This points to the “Q4” miss being more related to timing of revenue and profit recognition than anything. It makes the large Q3 beat a tad less impressive, but still impressive.

Progyny expects to add 85+ new clients to reach “at least” 460 in 2024. It also expects to add 1.3 million covered lives for 2024 with near-100% client retention. This represents 24.3% Y/Y client growth as well as 24.1% Y/Y member growth. Analysts were expecting 474 clients for 2024 with this guidance keeping that firmly on the table. It usually adds a handful of smaller clients that go live early during that same year. Analysts were also expecting 6.4 million covered lives with Progyny’s guidance about 4.2% better than that estimate.

Importantly, 300,000 of these members are from its first federal government agency. This deal includes only its patient care advocates and case management. Meaning? It will come with a lower revenue contribution during year one with Progyny optimistic that it can up-sell more services thereafter. This revenue will also be higher margin than the rest of its business. Without this help, member guidance was roughly in line. But again, Progyny generally adds more clients and members within a given year. It’s not solely last year’s selling season that feeds next year’s growth for the firm.

Margins will fall Q/Q in the fourth quarter as it adds the talent needed to support all clients going live in 2024. This is typical.

The Q4 revenue guide, conversely, represents negative Q/Q growth which is different from last year. This bothered me, but I reached out to my contact with the firm to clear things up. The abnormally large batch of early go-lives in Q3 2022 impacted seasonality. When a client launches, it takes a while for coinciding members to work through courses of treatment. These members also start with lower dollar services (like diagnostics) vs. higher-value treatment. The development of cycles takes time. So? Because so many early launches happened in Q3 2022, Q4 2022 revenue was abnormally high. The same abnormally large early-go-live factor played out in 2019; the pandemic threw off seasonality in 2020 and 2021 via clinic closures and subsequent re-openings. This is Progyny finally getting back to normal seasonality. And again, the full year raise is really what I care about.

Balance Sheet

- $336 million in cash & equivalents. This is over 10% of its entire market cap.

- Share count rose 1.0% Y/Y.

- No debt.

Call & Release Highlights

Overall demand environment & wrapping up the 2023 selling season

Member engagement remains healthy as family building remains a top priority for younger employees. Progyny’s better treatments with 7 years of growing outcome leads, better cost structure, better support and better specialist network is all helping to continue to drive robust demand. Secular tailwinds like the later age of average pregnancy and rising same-sex marriage rates are helping too. Its value proposition is best in class in an industry ripe for improvement and growth. Good spot to be in.

“Given the results of the sales and renewal season we just completed, we are entering 2024 well positioned to deliver another strong year of growth.”

CEO Pete Anevski

Competition seems to be falling further behind. Anevski thinks the sector is getting “less competitive” as “known losses were way lower than last year.” It continues to briskly take more market share.

Labor Market Health

As the team has told us would be the case, it’s seamlessly overcoming layoff headwinds from 2023. Meta, Microsoft, Amazon and several other giants are all Progyny clients who have conducted large layoffs to right-size the cost base. This led to investor concern about its membership growth. Just like we were told, the hit from these layoffs was as expected and more than offset by non-tech clients adding more employees.

Domino Effect

Progyny leadership constantly talks about a domino effect for its industry penetration. After it lands a bellwether from a certain sector, competition generally follows suit to ensure they remain competitive in talent recruiting. This year, winning its first sports team soon led to it winning an entire sports league. It’s also gaining rapid traction within labor union populations after landing its first contract there last year. Today, it has clients representing 46 sectors overall.

Up-Selling

Up-selling momentum continues. Its new clients went with 2-3 treatment cycles per employee on average which is consistent with previous years despite heightened budget focus. Notably, 20% of existing clients are adding more services for 2024 vs. 25% doing so last year. This decrease is simply because its Rx penetration is now much closer to 100%. 98% of its new clients selected ProgynyRx for its highest attach rate ever. In 2024, its overall Rx attach rate will rise to a new record of 93%. It just keeps climbing. This is why it’s so important that Progyny not only fosters better outcomes but also cuts significant costs. Its better practices mean less NICU usage, less treatment per fertilization and better adherence to fertility meds. All of this helps Progyny outperform when times demand budget scrutiny like right now.

Its pre-conception, maternity support, postpartum and menopause offerings will go live in 2024 to create more up-selling potential. Its male infertility product just recently went live this year.

Today’s Not-Nows are Tomorrow’s Wins

Progyny’s “Not-Nows” are clients that want to launch but aren’t yet ready to do so. The proportion of not-nows in its selling season this year may have ticked higher. It was unclear in the call if that rate was steady or modestly elevated. Either way, this is not a concern considering robust 2024 member and client guidance.

Not-now motivation is (or might be) elevated because of a few items. First, poor macro leads to sales cycle elongation and budget tightening. Progyny, with the non-discretionary nature of its service, is insulated but not immune from this. Furthermore, this budget tightening trend is coinciding with an explosion in weight loss drug demand. This means another priority for employers to gauge in a growingly complex balancing act. Benefit plans have finite budgets.

“Even with these factors, we’ve seen fertility remain a significant priority as we enter 2024 with meaningful tailwinds behind us.” – CEO Pete Anevski

Whatever it is… again… it’s not concerning even if the rate did tick higher. Why? Every year, Progyny’s not-nows represent a large chunk of its client wins in the following year. We have years of evidence pointing to not-nows actually being not-nows rather than not-evers. In 2021, it cited this same factor due to pandemic issues and that backlog converted into accelerating client growth as forecasted. It expects 2024 to be no different with most early client wins coming from this bucket.

“We have a very healthy pipeline of advanced opportunities… pipeline is larger than a year ago which is really positive.” – CEO Pete Anevski

Margins

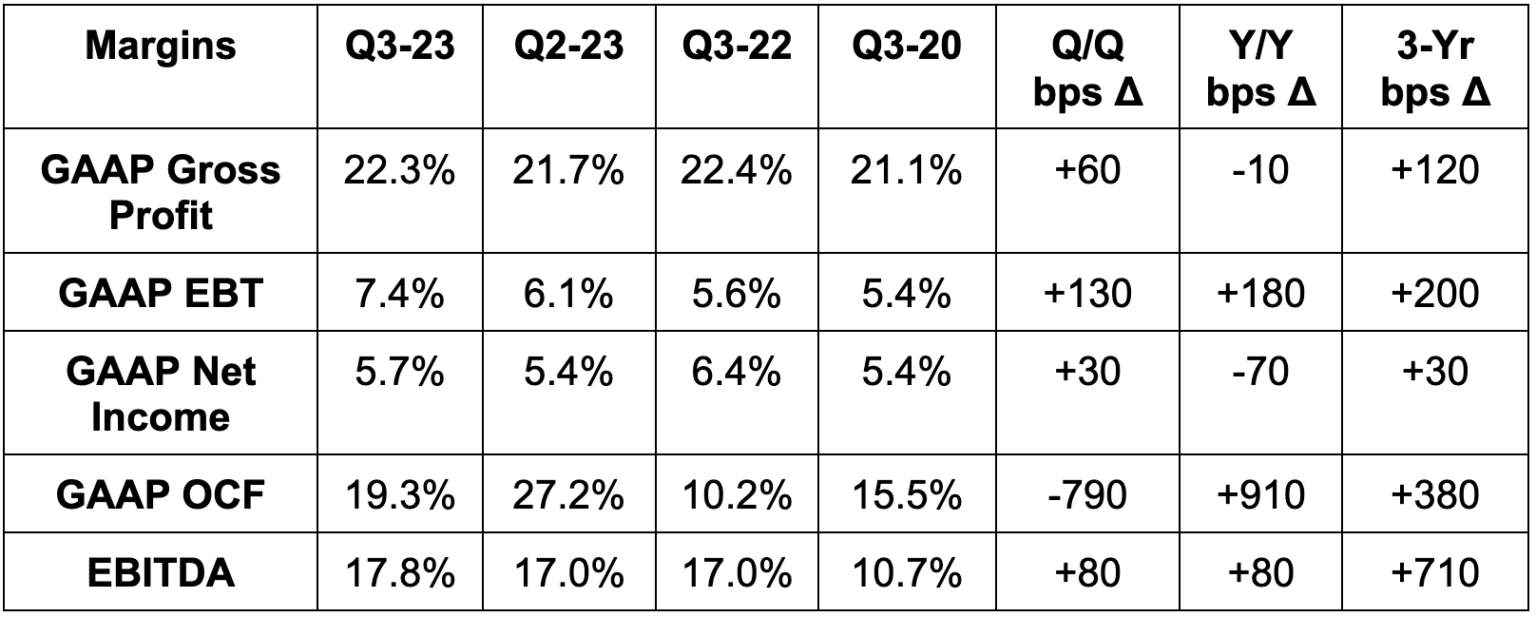

Progyny continues to generate operating leverage within the general & administrative (G&A) cost bucket. Specifically, G&A was 10.5% of sales vs. 11.5% Y/Y. More leverage here is expected to come. This is powering Progyny’s 20%+ incremental EBITDA margin expectation for 2023. That expectation offers concrete evidence of more overall margin expansion to come.

The income statement leverage is more telling and relevant than cash flow statement leverage. Operating cash flow is being positively influenced by new Rx contracts changing cash collection seasonality. I do love more free cash flow, but this needs to be called out.

StockMarketNerd’s Take

Great quarter. The Q4 revenue number is the lone weak spot which becomes somewhat meaningless given the strength of 2023 and 2024 overall. I care more about 8 quarters than 1. The sector is big enough to support rapid growth for years to come while not being too big to invite more competition. It’s a great spot for Progyny as the employer cost, employee cost and patient outcome leader. Rock-solid execution from a talented team with a defensible value prop.

To see the complete earnings report, check the SEC filings here.