Microsoft (MSFT) – Earnings Review – April 25, 2024

Demand

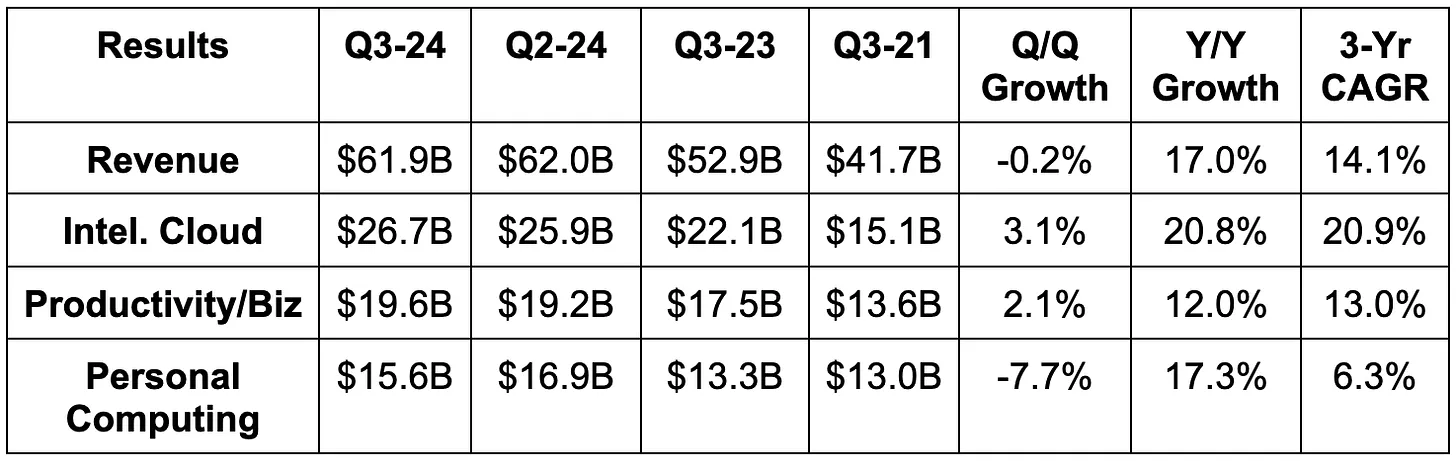

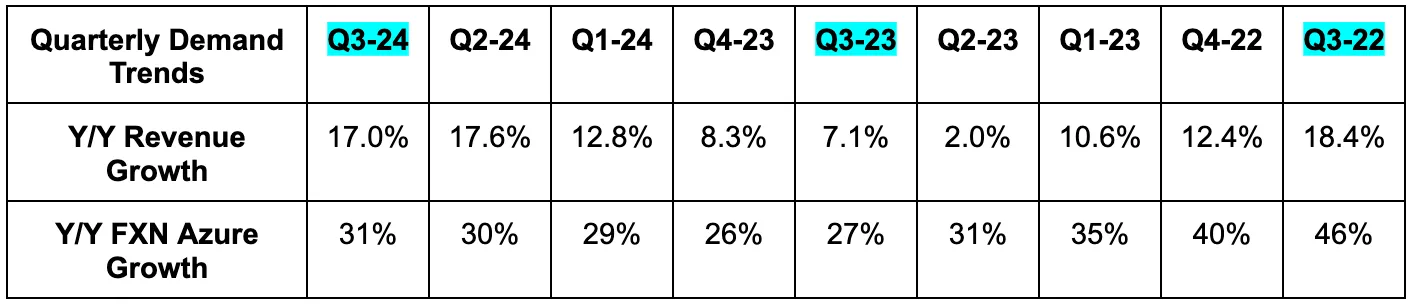

- Beat revenue estimates by 1.6% & beat guidance by 2.3%. Its 14.1% 3-year revenue CAGR compares to 12.9% last quarter and 14.9% 2 quarters ago.

- All three revenue segments were ahead of expectations.

- Beat Azure FX neutral (FXN) growth estimate by 250 bps & beat guidance by 300 bps. Strong.

- Commercial bookings rose by 29% Y/Y vs. 17% Y/Y last quarter and 14% Y/Y the quarter before that. This was much better than expected. Larger and longer Azure contracts were cited as the reason.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Profitability & Margins

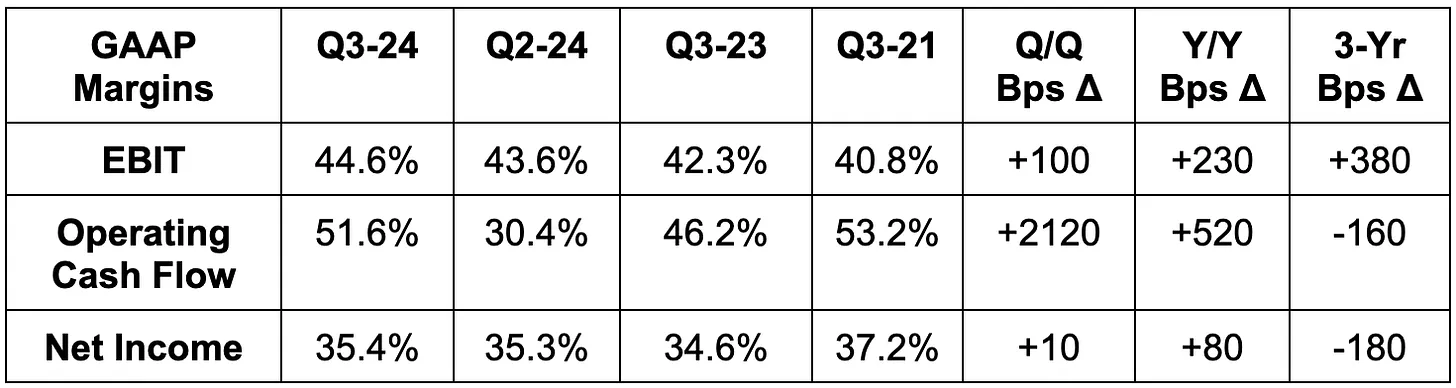

- Beat EBIT estimate by 4.9% & beat EBIT guide by 6.4%.

- Activision Blizzard shaved 200 bps off of its EBIT margin. Operating expenses rose by 10% Y/Y or 1% Y/Y ex-Activision M&A.

- Intelligent cloud EBIT margin was 46.8% vs. 42.9% Y/Y. Intelligent Cloud gross margin was 72% vs. 72% Q/Q & 72% Y/Y. It decreased ever so slightly (rounding error), but increased slightly when excluding a change in the estimate of the useful life of some infrastructure.

- Productivity and Businesses EBIT margin was 51.8% vs. 49.3% Y/Y.

- Beat $2.83 GAAP EPS estimate by $0.10.

- Activision Blizzard reduced EPS by $0.04.

- EPS rose by 20% Y/Y.

- FCF rose by 18% Y/Y.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Balance Sheet

- $80 billion in cash & equivalents.

- $62.5 billion in total debt.

- Dividends rose by 10.1% Y/Y.

- Diluted shares rose slightly Y/Y.

Guidance & Valuation

Next quarter:

- Revenue guidance missed by about 1%. This seemed to be entirely related to $700 million in incremental Q/Q FX headwinds. Without this headwind, revenue would have been slightly ahead.

- Azure will maintain a 30%-31% FXN growth rate. This is despite some infrastructure capacity restraints that it’s currently dealing with.

- Commercial bookings growth is expected to remain solid.

- CapEx will again rise meaningfully Q/Q to support infrastructure investments. It’s getting aggressive here just like Alphabet and Meta are. For context, CapEx this quarter rose by 80% Y/Y to reach $14 billion.

- Cloud gross margin should fall by 200 bps Y/Y and will fall slightly when excluding the tough comp impact from extending the useful life of some infrastructure.

- EBIT was 1.1% better than expected, and Microsoft raised its annual EBIT margin expansion guidance from 150 bps to 200 bps.

For 2025, it offered some preliminary guidance. It sees 10%+ revenue and EBIT growth for the year, which keeps 14% Y/Y growth estimates for both on the table. Conversely, it also sees 100 bps of EBIT margin contraction Y/Y due to rising investments and depreciation costs to support infrastructure. This is technically 100 bps worse than expected, but 2024 EBIT margin will be better than currently expected, so the true miss is smaller.

Call & Release Highlights

GenAI:

Microsoft has taken the most aggressive approach to monetizing GenAI in the cloud and software space. GenAI is already propping up Azure’s overall revenue growth by a full 7 points as its Copilot offering builds meaningful traction. Copilot is essentially Microsoft’s GenAI assistant that is used across products like GitHub (software development), Azure, Office 365 and basically everything else that it does. Copilot is even being used for dedicated sales and customer resource management (CRM) automation. Overall, it’s used by 60% of the Fortune 500 today.

Copilot is also a foundation for creating more local, custom assistants for customers. Copilot Studio is essentially its new playground for customers to integrate their own data to create more relevant assistants. Studio enjoyed 175% Q/Q growth — off of a small base.

Azure:

Azure Arc is its platform to access applications and data in a multi-cloud environment. This is a key tool in removing cloud migration friction for customers like Dick’s Sporting Goods as most companies don’t want to use a single public cloud. They want to use multiple; this makes that easier. So? Migration frequency for Azure is accelerating partially thanks to Arc. All in all, Arc grew its customer count by 100% Y/Y to reach 33,000.

Impressively, 65% of the Fortune 500 already uses Azure AI while spend per customer here just keeps rising. These Azure AI customers are also using its data and analytics tools at a 50% clip. Popular cross-selling products here so far include Cosmos Database (DB), which is Microsoft’s fully managed, multi-model database service. Multi-modal here means diverse querying structures. Its next-gen data analytics framework (Fabric) is another popular example. The point is that Azure AI is directly creating better, incremental use cases to make other products more compelling for clients. This is why Azure accelerated Q/Q yet again while the demand and cloud optimization environment remained steady. Large deals, partially due to this increasingly strong cross-sell lever, are facilitating acceleration… as are market share gains. While it’s not just AI driving Azure’s growth, AI is improving demand for all Azure cloud services.

- $10 million deals more than doubled for Azure Y/Y.

- Azure is enjoying an acceleration in multi-billion contracts secured.

- Cloud usage optimizations are still happening, but the bulk of the optimization wave is behind us.

GitHub:

GitHub is killing it for Microsoft. 90% of the Fortune 100 are clients. GitHub Copilot (automated coding) subscriptions rose by 35% Q/Q and revenue overall accelerated yet again to 45% Y/Y. Copilot subscribers like AT&T are accelerating usage based on this assistant as Copilot “bends the productivity curve.” From coding experts to dummies, its wide set of source code tools is freeing developers to create powerful software packages in a more automated, managed fashion. It’s now to a point where, for simple code creation, users can just tell Copilot exactly what they want to be written.

Productivity & Business Processes (Microsoft Teams, Dynamic, LinkedIn & 365 etc.)

Microsoft is rolling out a new version of Teams that is 2x faster while using 50% less memory vs. the old version. Y/Y usage growth for this tool continued to be positive. Teams crossed 1 million rooms for the very first time.

Office Commercial Product and Cloud Service growth was 13% Y/Y, thanks to 15% Y/Y 365 Commercial growth (4% for Consumer). Office Commercial Products specifically saw revenue fall by 20% Y/Y as clients continued to migrate to the cloud.

- LinkedIn grew by 10% Y/Y. This was its 7th straight quarter of LinkedIn hiring marketplace share gains. The muted job market is, for now, diminishing the positive impact of this progress.

- Dynamics Products and Cloud Services revenue rose by 19% Y/Y.

- The Office consumer suite reached 80.8 million subscribers vs. 70.8 million Y/Y.

- Bing now has 140 million daily active users (DAUs); the team said they took more share of overall search during the quarter.

Personal Computing (PC):

- The PC demand environment was better than expected.

- Activision was the source of the 61% Y/Y Xbox revenue growth. Organic gaming growth was 0% Y/Y. Still, this gaming segment outperformed expectations as Call of Duty performed very well.

Take

Like Google, Microsoft is second to none in terms of consistent execution and drama-less profitable compounding. And like Google and Meta, CapEx will continue to soar to support GenAI infrastructure. Still, margin preservation is strong, shareholder returns are growing and this company just keeps executing… quarter after quarter. Another great report. Enough said.