Credit Earnings — Visa; American Express; Capital One — January 27, 2024

Visa (V)

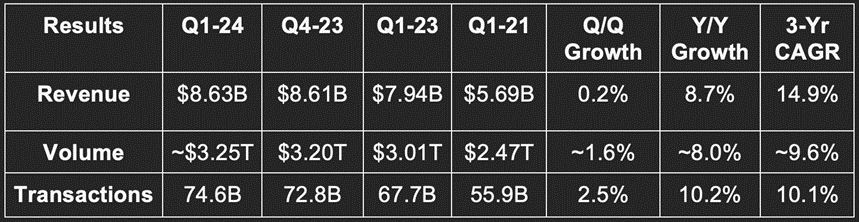

Results:

- Beat revenue estimates by 1%.

- Beat earnings before interest & tax (EBIT or AKA operating income) estimates by 1.1%.

- The 14.9% 3-year revenue compounded annual growth rate (CAGR) compares to 19.1% as of last quarter & 18.8% 2 quarters ago.

- Beat $2.31 GAAP earnings per share (EPS) estimate by $0.08.

Non-GAAP EPS, which excludes litigation provisions, mark-to-market equity investment fluctuations and amortization of acquired intangible assets, rose by 11% Y/Y. Non-GAAP net income rose by 8% Y/Y with buybacks the source of the faster EPS growth. These items are also why GAAP operating expense (OpEx) fell by 6% Y/Y while non-GAAP OpEx rose by 7% Y/Y.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Bps = basis points; 1 basis point = 0.01%.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Balance Sheet:

- About $21.4 billion in total cash & equivalents.

- $20.7 billion in total debt.

- $3.58 billion in buybacks vs. $3.12 billion Y/Y.

- Share count fell by 2.7% Y/Y.

- Dividend payments rose 12.2% Y/Y for the quarter.

Guidance:

Q2:

- “Upper mid to high single digit Y/Y revenue growth” roughly met expectations of 8.6% Y/Y growth.

- “High teens” non-GAAP EPS growth beat expectations of 14.2% Y/Y growth.

2024:

- “Low double digit Y/Y revenue growth” beat expectations of 10.1% Y/Y growth. Strong.

- “Low teens non-GAAP EPS growth” roughly met expectations of 13.2% Y/Y growth. Strong again.

- This represented a reiteration of previous guidance which assumes no recession. Analysts were clearly expecting modest downward revisions.

Quarter to date, U.S. spend slowed from 5% Y/Y to 4%. This was not due to a weakening consumer, but instead “severe weather conditions.”

Visa trades for 22x next 12 month (NTM) EBIT and 27x NTM EPS. EBIT is expected to grow by 16.0% this year while EPS is expected to grow by 18.2%.

Call & Release Highlights:

The Consumer Entering 2024 & Quarterly Results Context:

Visa’s fiscal year 2024 is “off to a solid start.” It told us last quarter that U.S. volume growth had slowed from 6% Y/Y to 5% Y/Y quarter-to-date. The slowing was “largely due to less favorable mix of weekends and weekdays” rather than a more fragile consumer. That’s where the overall quarter ended up. Debit spend growth specifically slowed from 7% to 5% while credit spend stayed at 6% Y/Y. The 6% credit growth actually represents an intra-quarter acceleration; the team told us credit growth had slowed to 5% Y/Y for the quarter-to-date on its last call. October was its quietest month, November was the busiest and December was roughly between the first two.

Internationally, Y/Y volume growth was steady compared to last quarter at 12%. Per CEO Ryan Mclnerney, consumer spending “remains resilient.” That’s great to hear from a card network representing trillions in quarterly volume.

Acceptance locations rose 17% Y/Y. Notable wins include Brazil’s Caixi which hosts 10,000 lottery locations for things like bill pay and payment vouchers. Lowe’s also added tap-to-pay acceptance during the quarter. The list of renewal and new customer highlights across the globe was quite long. One of the most notable wins was adding Visa’s loyalty program service to Bank of America’s product suite. Value-add services continue to be a key growth lever. The other juiciest highlight was a newer Visa Direct partnership with Meta. Visa Direct is its peer-to-peer money transfer product, which competes with Venmo, Zelle and Cash App.

- Cross-border growth of 16% Y/Y was a notable standout. It inked a new deal with Western Union to turbocharge traction here.

- Service revenue rose 11% Y/Y.

- Data processing revenue rose 14% Y/Y.

“Consumer spend across all segments has remained stable. Our data does not indicate any meaningful behavior change across consumers.” – CFO Christopher Suh

Holiday Season:

U.S. spend for the holiday was right around 5% Y/Y. Consumer retail spending growth was stable Y/Y, but accelerated during Black Friday-Cyber Monday.

M&A:

Visa plans to buy Prosa to expand further into Mexican payment processing. It also completed its aforementioned Pismo M&A. Pismo is a cloud native issuer and a multi-core banking platform. It competes with players like SoFi’s Galileo/Technisys. With Pismo, Visa will provide cloud-native processing APIs and support for more emerging payment methods.

Take:

The upbeat commentary about the global consumer put a subtle grin on my face. I trust non-anecdotal data representing a large chunk of the U.S. GDP much more than random data points from anonymous accounts on social media. Let them talk and bicker amongst themselves. Visa sees continued consumer resilience; Visa has a far better pulse on consumer health than you or I do. Good quarter.

American Express (AXP)

Results:

The firm missed revenue estimates by about 0.9%. It met GAAP EBT (not EBIT) estimates and also met GAAP EPS estimates.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Guidance:

Annual 2024 revenue guidance was 1% ahead of expectations. Annual 2024 EPS guidance of $2.90 was $0.58, or 4.7%, ahead of expectations. This, paired with solid Visa guidance, is great news for what the largest consumer credit players in the world are currently seeing. This quote is great news too:

“Going forward, we expect to see delinquency and write-off rates remain strong with modest increases in 2024.” – CEO Stephen Squeri

Credit Health & Balance Sheet:

Notably, its net write-off rate was 2.0% vs. 1.8% Q/Q & 1.2% Y/Y as its credit performance (like everyone else’s) continues to normalize. Encouragingly, this performance is still right in line with pre-pandemic levels, which hovered right around 1.8%-2.2%. And as the quote above indicates, no incrementally sharp worsening from here is expected.

Furthermore, its 30+ day past due credit rate of 1.3% still compares favorably to the 1.4%-1.6% rates it experienced in 2019. Its credit has not deteriorated beyond pre-pandemic levels like we’ve seen for lower credit quality originators like Discover and Capital One. These metrics (and credit provisions rising by a modest $400 million Y/Y and $210 million Q/Q) offer evidence.

AmEx is the highest credit quality name in my coverage network. Its average borrower quality is more similar to the SoFi’s of the world than Capital One or Discover. Visa is right in the middle (but it doesn’t take credit risk).

- $49B in cash & equivalents.

- $49B in total debt ($1b is current).

- Dividend rose 15.4% Y/Y.

Share count fell by 2.7% Y/Y.

Capital One (COF)

While Capital One’s results weren’t awful (small beat on revenue and misses on profit across the board), the deterioration in its credit metrics was notable. Its 30+ day delinquency rate rose to 3.99% vs. 3.71% Q/Q and 3.21% Y/Y. Unlike AmEx, 3.99% is above the 3.84% peak that it saw in the quarters before the pandemic. It’s not significantly worse, but it is worse. Net charge-off rate also rose to 3.21% vs. 2.56% Q/Q and 1.86% Y/Y. That’s the concern here as its peak rate in the quarters before the pandemic was 2.67%. Its credit loss allowance is also 4.77% of loans vs. 4.75% Q/Q and 4.24% Y/Y. The modest sequential rise is a silver lining as it points to a lack of abrupt and incremental worsening in future credit performance expectations. Provision allowance is the leading indicator here. Delinquency rate is more of a real-time indicator, while charge-off rate is more of a trailing indicator.

“Based on the stability we’ve seen in our delinquencies since August and extrapolating from our current delinquency inventories and flow rates, we believe the charge-off rate is stabilizing now and settling out to about 15% above 2019 levels.” – CFO Richard Fairbank

As macro becomes more fragile, like it did in 2023, the poorest consumers are always the least insulated. This is the reality for a credit card issuer with lower average consumer credit quality. Worsening was entirely expected. The rate of worsening was a bit sharper than I was personally hoping for. Conversely, expectations of stabilization are also better and earlier than I was hoping for. All in all… the higher end consumers continue to do well while the middle/lower end seems a bit more fragile.