Taiwan Semiconductor (TSM) – Earnings Review – January 20, 2024

Taiwan Semi builds chipsets for other companies like Nvidia and Qualcomm. It does so in its highly expensive, highly complex chip fabrication plants. These are called “fabs” for short.

Needed Definitions:

- Fab means a factory

- Nanometer (NM) describes the chip technology. Smaller NM is more advanced as it uses smaller transistors. Its newest 3 NM technology also includes an upgraded transistor technology to bolster the capacity. This means TSM can add more transistors to a single chip while making those chips more energy efficient and cost-effective.

- “Advanced Technology” Revenue = revenue from 3nm, 5nm & 7nm technology.

- Wafer refers to the raw materials (like silicon) that are used to manufacture chips and manipulate the materials with desired tasks.

Results

- TSM beat revenue estimates by 0.3% & beat its guidance by 2.2% at the midpoint. Its 15.7% 3-year revenue compounded annual growth rate (CAGR) compares to 12.3% as of last quarter & 14.7% 2 quarters ago.

- Met GAAP gross profit margin (GPM) estimates & beat its 52.5% GAAP GPM guidance by 50 basis points. (bps = basis point; 1 bps = 0.01%)

- Beat 41% GAAP EBIT margin estimates by 60 bps & beat its guidance by 80 bps.

- Beat $1.39 GAAP earnings per share (EPS) estimates by $0.05. It trades for about 18x next 12-month earnings.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

ROE = Return on Equity

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Guidance

Next Quarter:

- Beat revenue estimate by 0.9%.

- Beat 39.4% GAAP EBIT margin estimate by 160 bps.

- Beat 51.3% GAAP GPM estimate by 170 bps.

- Dividend growth will be roughly 17% Y/Y next quarter & will continue growing from there.

2024:

- It also expects CapEx of $30 billion for the full year vs. $30.4 billion in 2023.

- Guided to mid 20% Y/Y revenue growth, which compares very nicely to consensus looking for 21.3% Y/Y growth.

Balance Sheet

- $54.3 billion in cash, equivalents & marketable securities.

- $30 billion in bonds payable.

- Inventory rose 13.6% Y/Y. Still, days of inventory fell 11 days Y/Y due to strong 3NM demand.

- Dividends rose 2.3% Y/Y in 2023 vs. 2022.

- Accounts receivable fell 4 days Y/Y to 31 days.

Call & Release Highlights

Demand & Macro Context:

A strong ramping of 3NM tech was credited with the demand outperformance this quarter. It was a “tough year for the industry” per the team. Weakening macro, high inflation and soaring cost of capital all “prolonged the global semiconductor inventory adjustment cycle.” Still, its tech leadership powered its outperformance of -8.7% Y/Y growth vs. -13% for its overall sector. Furthermore, based on the 2024 guide, it sees growth sharply recovering in the quarters ahead as it’s “well positioned to capture AI and high performance compute growth opportunities” with its advanced technology. Its mid 20% 2024 revenue growth guide compares to overall industry growth of 10% and 20% Y/Y for its foundry category.

Inventory levels across the industry are now, finally getting back to “healthier levels.” The company is confident that its “business has bottomed out Y/Y.” All in all, leadership reiterated its 15%-20% annual revenue growth target first offered in January 2022.

Margins:

The gross margin decline for the year (contracted 520 bps for all of 2023 Y/Y) was as expected. It’s based on 3NM volume ramping to a point of margin maturity. That takes time. For now, it’s a continued gross margin headwind while becoming a larger portion of its overall revenue.

TSM also continues to invest heavily in R&D to “extend its tech leadership.” It always invests ahead of expected demand opportunities and does not shy away from doing so if end markets weaken for a few quarters. It takes the extremely long term view, which is needed when its fab plant expansion takes several years to deliver. It decided to keep the pedal to the metal here in 2023 despite weakening demand. This led to EBIT margin falling 690 bps Y/Y for 2023.

For 2024, better capacity utilization will help margins as demand recovers. Its continued investments in 3 nanometer will hurt gross margin by 300-400 bps for the year. Furthermore, it’s working on converting some N5 capacity to N3 capacity to support the multi-year demand ramp. This will mean heightened margin pressure in 2024 by another 100-200 bps. It will mean lower costs thereafter. Over the long haul, ex-volatile foreign exchange, it remains confident in a 53%+ gross margin.

New 3NM Tech & N2:

Taiwan Semi continues to iterate on its 3NM node. Its N3E, N3X and N3P chips are all in the works and began volume production this quarter. These offer higher performance and different use cases for its end customers. All are key pieces in its expectation of 200%+ Y/Y revenue growth within its 3NM revenue bucket.

For its newest 2NM node, “consumer interest and engagement” compared to N3 is “much higher.” The first iteration of its 2NM technology will begin volume production next year. To cater to high performance computing use cases, it will offer a chip with a backside power rail solution by 2026. Traditionally, power is transferred to transistors from the front of the chip. By moving it to the back, energy efficiency and heat management are both improved. TSM is always innovating.

AI:

“A surge in AI-related demand in 2023 supports our already strong conviction that the structural demand for energy-efficient computing will accelerate in an intelligent and connected world. TSMC is a key enabler of AI applications. No matter which approach is taken, AI technology is evolving to use more complex AI models as the amount of computation required for training and inference is increasing.” – TSM Leadership

Global Factory Footprint:

- In Japan, it expects its 12-28 nanometer tech facility to open in February and begin volume production in Q4 2024.

- In Arizona, it remains in “close contact with the U.S. government on incentives and tax credit support.” It’s making “strong progress” with Arizona labor groups and is now installing equipment at its first planned fab in the states. Volume production is expected to begin in early 2025.

- In Germany, it continues to work towards a new factory in Dresden for auto and industrial end markets.

In Taiwan, it’s greatly expanding 3NM capacity to meet demand.

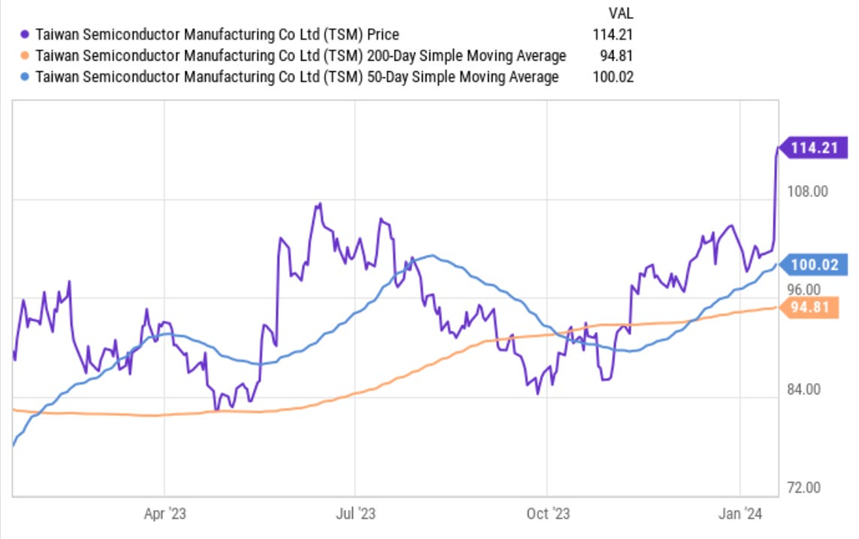

Source: YCharts