Shopify (SHOP) — Earnings Review — February 14, 2024

Shopify is a web-builder on steroids. It automates the creation of slick, powerful store design. It provides ubiquitous channel integrations and offers several other product buckets to round out its niche as a merchant’s “commerce operating system.” Its goal is to remove the headaches associated with building a business and to allow merchants to focus on growth rather than system maintenance. It gives merchants of all sizes the tools previously reserved for the largest enterprises in the world – and calls many Fortune 500 brands its customers too. If you’d like to learn more about this firm, my deep dive can be found here.

“We are operating at an unparalleled level in our history from the incredible work of Shopify team members… For 2024, we will not slow down. We will be relentless in our craftsmanship and foundation to keep us at the center of commerce.” – Shopify President Harley Finkelstein

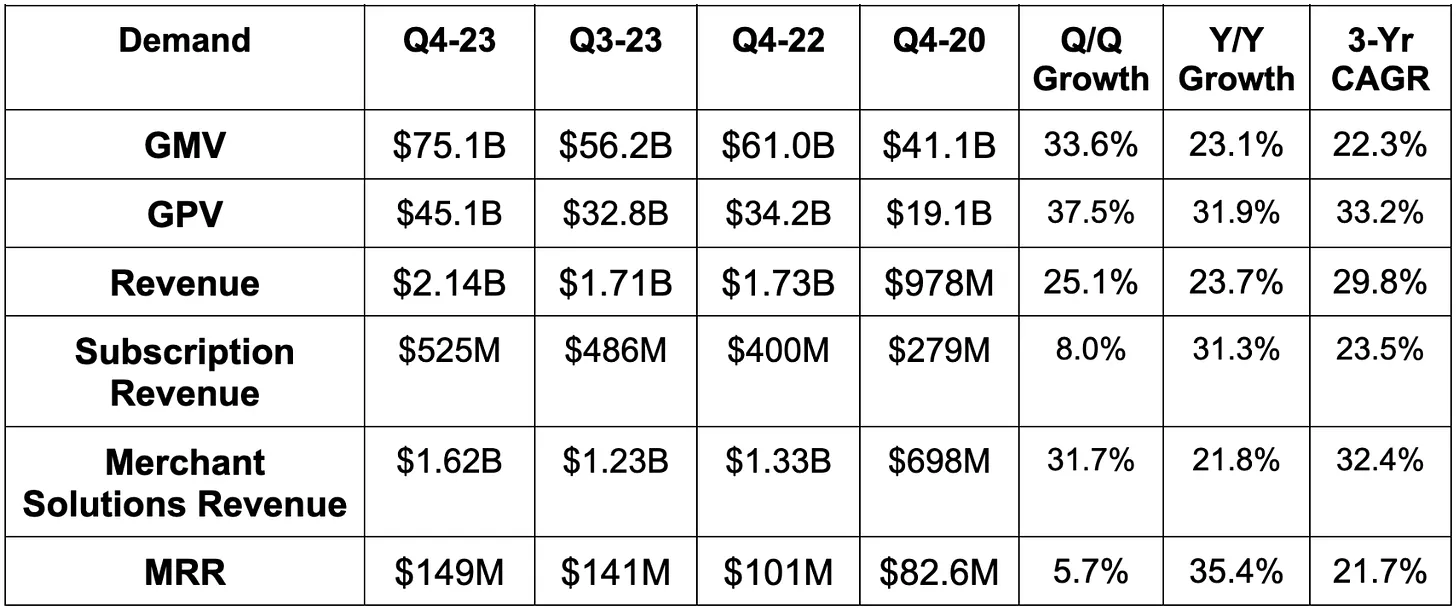

Demand

- Beat gross merchandise volume (GMV) estimates by 4.9%.

- Beat revenue estimates by 3.1% & beat its guidance by 4.4%.

- Revenue growth excluding the sale of its fulfillment business was about 30% Y/Y.

GPV = Gross Payment Volume; MRR = Monthly Recurring Revenue

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Margins

- Shopify slightly missed GAAP gross profit margin (GPM) estimates, but met its GAAP GPM guide.

- Shopify beat EBIT estimates by 1.9%. Considering its vague quarterly revenue guidance, GPM guidance and vague GAAP operating expense (OpEx) guidance, it comfortably beat its EBIT estimates.

- Beat free cash flow (FCF) estimates by 17.1% and beat its FCF guidance by 22.9%.

- Beat $0.30 earnings per share (EPS) estimates by $0.04. It crushed GAAP EPS estimates; this was aided by equity investment gains. For this reason, I prefer to focus on non-GAAP for EPS.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Balance Sheet

- $5 billion in cash & equivalents.

- $916 million in senior notes.

- Diluted shares rose 2% Y/Y; Basic shares rose 1% Y/Y. Basic shares only include common equity that can be openly transacted. Diluted includes options and more.

Guidance & Valuation

Shopify’s guidance assumes a stable macro environment, measured headcount growth and “leaning into delivering a compelling mix of growth and profit.” The guide also assumes that the recently announced Shopify Plus price hike mainly boosts 2024 results in the back half of the year. New pricing doesn’t go live for existing merchants until May 8th; those merchants can lock in a 3-year contract at old rates before then if they’d like to.

Its low 20% Y/Y revenue growth guide for Q1 compares favorably to expectations of 20.2% Y/Y growth. Its mid-to-high 20% Y/Y revenue growth guide for Q1, when excluding the sale of its fulfillment business, also compares favorably to expectations of about 26% Y/Y growth.

It guided to a 51% GAAP GPM for Q1 vs. expectations of 51.3% and told us to expect 13%-14% Y/Y GAAP OpEx growth. This is GAAP OpEx guidance, while the analyst data I have access to is in non-GAAP. Its implied non-GAAP EBIT guide is a tad light vs. consensus. The reason didn’t bother me. Shopify has identified new marketing opportunities at strong payback periods for Q1 2024 and will accelerate spend to capture that potential. AI is the source of this new opportunity as Shopify has cut acquisition costs by 30% using GenAI models. Its Q1 FCF guidance was roughly in line and its vague full year FCF commentary keeps the annual FCF estimate firmly on the table.

Shopify trades for 86x 2024 EBIT and 94x 2024 FCF. EBIT is expected to grow by 80% Y/Y while FCF is expected to grow by 53% Y/Y.

Call & Release Highlights

Winning Globally:

Shopify continues to effectively localize its product suite, build its global partner roster and thrive across the world. It enjoyed 35% Y/Y growth in merchants outside of the USA and is taking market share everywhere. Europe now represents 27% of its total merchant base, as growth accelerated to 40%+ there for the first time in years. It won its largest UK merchant ever in Boden and added other notable brands like On Running and Oceans Apart.

I expect international momentum to remain strong in 2024 as the firm debuts its Shopify Markets outside of North America. This is its full-service, cross-border product allowing merchants to add new selling geographies with a click of a button… and without handling any parts of regulatory compliance. This should offer more upside to the 14% of Shopify’s total volume coming from cross-border sales today. Cross-border volume is higher margin volume than domestic. Other merchant solutions like its tax platform will debut globally this year to add to Shopify’s global take rate and overall success. The firm took years to perfect product market fit across its important markets. Now, it’s ready to “hit the ground running.”

Hydrogen:

As a reminder, Hydrogen is Shopify’s headless commerce offering. Headless simply means separation of back and front end functions to enhance customization and accelerate store innovation. This offering crossed $1 billion in Q4 GMV, which rose 600% Y/Y off of a very small base. ButcherBox and Tecovas are both now using it, with momentum expected to continue into 2024.

The Payments Suite & Consumer App:

Shop Pay, the company’s checkout accelerator, enjoyed 58% Y/Y volume growth as it continues to take share from PayPal, guest checkout and everyone else. Shopify recently opened Shop Pay to the entire internet, which is expected to meaningfully accelerate traction even more. Per a Big 3 survey, Shop Pay is by far the best converting checkout accelerator on the market, with double digit conversion leads compared to all others. Its move to one-page checkout in 2023 should keep this motor humming.

The Shop App is its consumer app, which directly supports Shopify Payments and Shop Pay usage. It crossed $100 million in monthly volume for the first time. Shopify ran a campaign with Mr. Beast during the holidays, which pushed it to #3 on the App Store during that time.

Shop Cash is a rewards program that runs through the Shop App. It was just consolidated into “Shop Campaigns” with the rest of its marketing tools like Shopify Audiences. Speaking of Shopify Audiences, that product just got an algorithm upgrade to cut customer acquisition cost (CAC) by 50%. Nike Strength, Netflix and Caraway are already using Shop Campaigns to reduce CAC and boost growth.

AI:

Shopify debuted 12 new AI tools within its Shopify Magic GenAI suite this year. It added AI-generated product descriptions, enhanced product image editing and continued sharpening the use cases for Sidekick – its AI-enabled commerce assistant.

“Our strategy involves integrating AI at the heart of our platform, simplifying merchant business expansion and adapting to the evolving commerce landscape. — Shopify President Harley Finkelstein

Winning the Big Boys:

The National Retail Federation’s (NRF) 2024 kick-off event was a great showing for Shopify. The firm’s “pipeline of GMV opportunities” was “remarkably different” compared to last year as Shopify is “gaining widespread recognition” from giants. Shopify also announced Google Cloud as another channel partner at that event. Whether it’s through Commerce Components by Shopify (CCS), Shopify Plus or Hydrogen, it now has the best-in-class tools to win these larger contracts.

Business to Business (B2B) is a big part of its Global 2000 merchant pursuit. Most of the big boys have established B2B channels, but Shopify didn’t really have a full-service product for them until last year. Now it does. With Shopify B2B, merchants can run B2B selling through the Shopify Admin like they would any other channel. Just click to turn it on. Shopify supports custom staff permissions, granular volume discounts and an overarching view of selling activity, as always. Growth here in Q4 was 150% Y/Y. This year, Shopify will turn its focus to landing new merchants through this offering. Up until now, most of its B2B success has come from existing merchant up-selling.

Offline:

Offline volume growth was 28% Y/Y. This accelerated vs. 26% last quarter and 23% in the quarter before that. Its offline revenue for 2023 was $441 million, representing a 4-year compounded annual growth rate (CAGR) of about 50%. Its new Point of Sale (POS) Pro subscription delivers all of the utility online selling enjoys to offline settings. With this software and a recent boost to the number of stores and terminals it can support, offline growth is set to continue its rapid growth trajectory.

Margins & Take Rates:

Price hikes from 2023 helped Shopify’s subscription gross margin, while the Plus price hike announced last week didn’t impact results this quarter. The fulfillment sale helped its merchant solutions gross margin. Ex-fulfillment sale, merchant solutions GPM was actually down a bit Y/Y. This was due to Shopify Payments continuing to outgrow the rest of the business. Importantly, while Payments has a lower GPM than other products, its EBIT margin profile is similar to the subscription bucket due to lower relative OpEx. Higher margin solutions like Markets Pro and the tax product also helped merchant solutions margins this quarter. All in all, OpEx fell by 22% Y/Y as expected. A lack of real estate impairment charges helped the negative growth.

Attach rate was stable Y/Y and fell a bit Q/Q. This falling is due to typical seasonality as Shopify Payments over indexes in Q4 and drives down attach rate a bit. Importantly, the fulfillment sale also weighed on take rate. Excluding it, take rate continued its trend of Y/Y increases. This was ignored by the buy-side notes that I read after the call. It shouldn’t have been.

Take

I see what the share price did, and I still think this was a very strong quarter. The light Q1 EBIT guide isn’t ideal, but the 2024 FCF commentary and the reasoning behind the miss made that unconcerning to me. As I’ve been talking about for a few months, Shopify the company is in fantastic shape. It has expeditiously and successfully morphed from a cash drain to a cash printer. Shopify the stock has been on an absolute tear, rising 100%+ in the last 11 months, and likely needs to digest those gains a bit. That’s why I’ve been trimming as I tell readers in the weekly newsletter.

The parabolic stock and expensive multiple meant this quarter probably needed to be perfect and free from any negatives to pick at. The slightly disappointing margin flow through is the negative; some will pick at as an excuse for this stock to cool off like it needs to. Analysts wanted the size of the revenue beat to lead to a slightly larger EBIT beat, which didn’t happen.

To me, that’s missing the forest through the trees. Just ~only~ expanding its EBIT margin from 3.5% to 18.5% Y/Y (with an explosive GAAP EBIT margin inflection) works just fine for me. The long term thesis is firmly intact. If this sell-off gets sharper, I’d consider adding. Not yet.