Lululemon (LULU) – Earnings Review – December 8, 2023

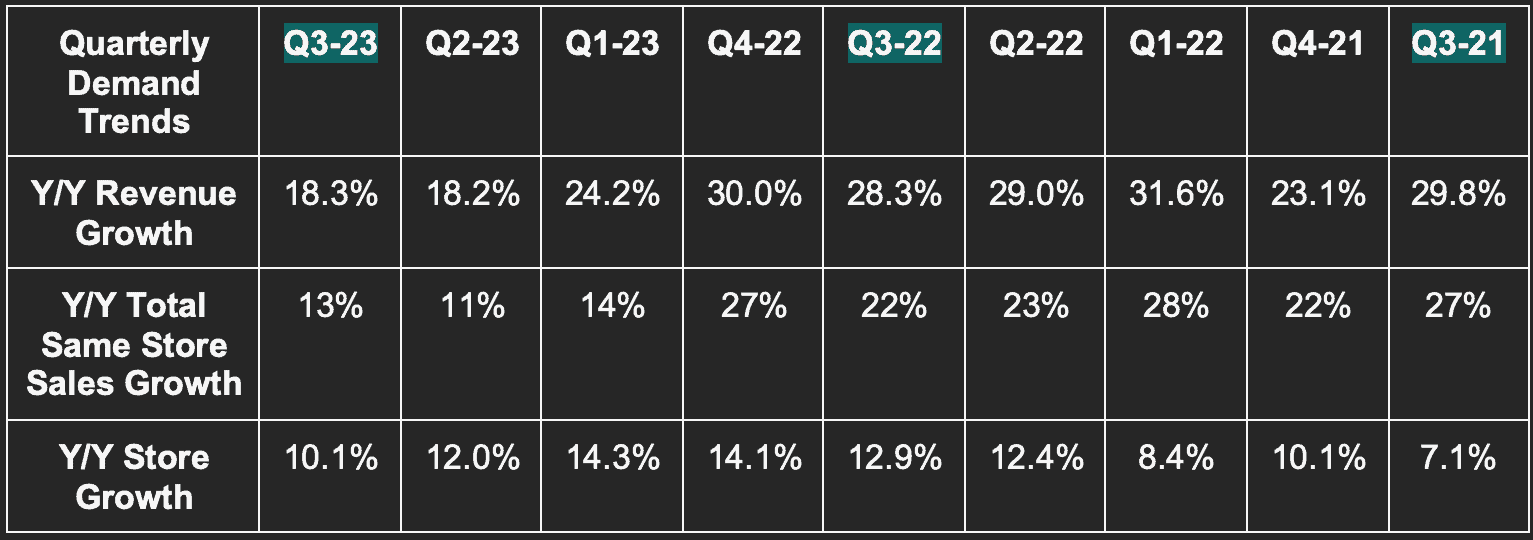

Demand

The company beat revenue estimates by 0.8% and beat its guidance by 1.2%. Please note that 3-year compounded annual growth rate (CAGR) comps remain very easy due to the pandemic. The firm, with normal comps, expects 15% annual revenue compounding.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

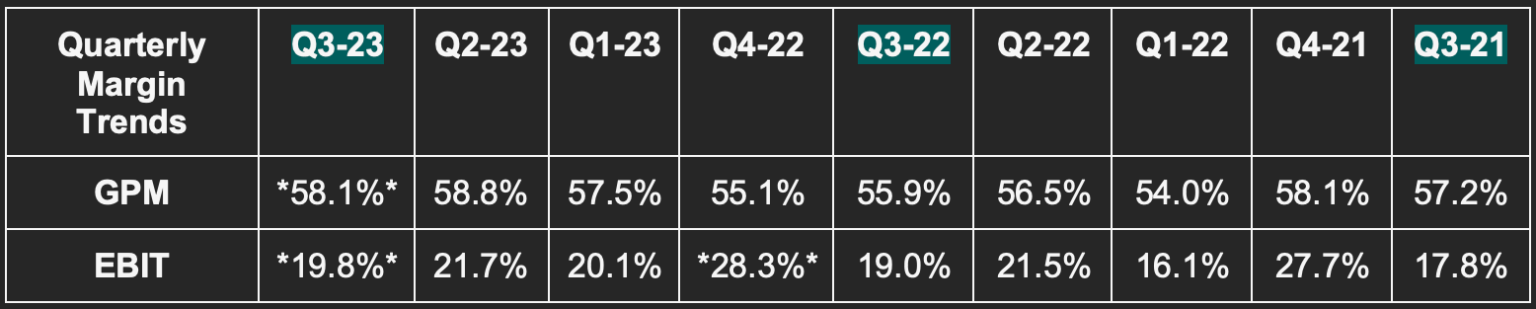

Margins

Lululemon doesn’t always offer non-GAAP profit metrics. It did this quarter due to provisions and restructuring costs related to its failed Mirror acquisition. The margins listed for Q3-2023 are adjusted for these items. Without this adjustment, gross margin would be 57.0%, EBIT margin 15.3% and net income margin 11.3%. These materially missed estimates which did not include these charges as timing for incurring this type of cost is uncertain. As you can see below, non-GAAP was well ahead across the board when removing this temporary noise.

- Beat earnings before interest and tax (EBIT) estimates by 6.2%.

- Beat $2.29 earnings per share (EPS) estimates by $0.24.

- Beat 57.7% gross profit margin (GPM) estimates by 40 basis points (bps; 1 bps = 0.01%) and beat its GPM guide by 50 bps.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

* adjusted for mirror related impairment and restructuring charges.

Guidance

Q4 revenue guidance was 0.8% below expectations and represents 13.5% Y/Y growth at the midpoint. EPS guidance of $4.89 was $0.06 worse than expected.

For the full year, Lululemon slightly raised revenue guidance by 0.3% which would represent 18% growth at the midpoint. This was related to Q3 outperformance as Q4 was again a tad light. For full year EPS, Lulu raised its guidance from $12.10 to $12.38. This is $0.19 ahead of estimates and would represent 22.9% Y/Y growth. Please note that the $12.38 guide excludes the same provision and restructuring charges already mentioned.

These charges were not in the guidance it offered last quarter, and were not baked into analyst estimates. Without this adjustment, its guidance of $11.81 is $0.29 light. I say this purely for your information. As the charges weren’t in previous guidance or estimates (and considering the nature of them), I consider this a raise. Mirror impairment charges will go away and are now entirely unrelated to the underlying operating profitability of this business.

- It now sees 70 bps of annual EBIT leverage vs. 50 bps as of last quarter and vs. 60 bps expected by analysts.

- It reiterated expectations of 200 bps of GPM leverage for the year.

- Inventory will be flat to slightly down Y/Y next quarter.

Finally, its 5 year financial targets first set back in 2021 were again reiterated.

Balance Sheet

- $1.1B in cash & equivalents.

- $400M in credit capacity.

- Inventory fell 4% Y/Y. This was better than its 8%-12% Y/Y growth expectation due to strong demand. Mirror inventory provisions helped too. It continues to expect markdown rates in 2023 to be stable vs. pre-pandemic periods.

- Share count fell slightly Y/Y.

- New $1B buyback (roughly 1.6% of float). It has $243 million left of its current buyback program.

“We remain comfortable with both the quality and quantity of our inventory.” – CFO Meghan Frank

Call & Release Highlights

Q4 Thus Far & Macro

The team is “pleased” with its holiday weekend and quarter-to-date performance. It’s seeing strength across e-commerce and brick and mortar with new and existing product lines all working. Full price merchandise continues to perform very well as consumers largely overcome economic anxiety. This is despite materially “deeper discounting” Y/Y from competition during the quarter. Lulu, as always, did not have to match that promotional intensity to find demand – and it didn’t.

“I definitely saw a more promotionally driven environment by some of our peers, by some of the new entries into this category. We didn’t deviate. We didn’t change. And our results I talked to indicate that we didn’t need to. Guests respond to innovative products and that’s what our pipeline is full of.” – CEO Calvin McDonald

The one soft spot was men’s apparel in North America – a key growth segment. The team blamed uncertain macro and men being more prone to cutting apparel costs amid that uncertainty vs. women. While this sounded. like an excuse, continued strong market share gains for men in North America point to it being a legitimate one. The market share data is per Circana, not internal claims. This makes it more meaningful. The firm is also taking share across the globe, but there aren’t great data sources allowing it to precisely quantify those gains.

The moderate men’s softness (and still having 2 months left in its quarter) led to leadership’s continued prudent, conservative guidance methodology for Q4. This was repeated several times during the call as a wink to Wall Street. Under-promise, over-deliver. I expect this beat- and-raise machine to beat-and-raise once more in three months.

A Promising New Marketing Lever

Members of Lululemon “Essentials Tier” continue to grow briskly. It doesn’t update the total every quarter, and didn’t this time, but likely will early next year. This is creating a large, highly relevant base of passionate fans to specifically target. That led to it debuting an early access Black Friday promotion for members. The promo resulted in an app downloadincrease of 250,000 without materially adding to marketing costs. These subscription bases will be highly efficient marketing pools as they continue to scale successfully.

More Growth Metrics

- Growth was strong in August, cooled in September due to lack of marketing activity and product launches, and again re-strengthened in October.

- Direct-to Consumer (DTC) revenue represented 41% of total revenue vs. 41% Y/Y.

- Other revenue (wholesale, licensing and Lululemon Studio) represented 10% of total revenue vs. 10% Y/Y.

- Company operated stores represented 49% of total revenue vs. 49% Y/Y.

- Women’s revenue rose 19% Y/Y while men’s rose 15% Y/Y.

- North American revenue rose 12% Y/Y which is in line with its long term targets despite the added macro uncertainty. International rose 49% Y/Y including 53% Y/Y growth in China. China stores continue to outperform internal expectations.

- Every market in Asia Pacific and Greater Europe grew by 10%+ Y/Y.

Peloton

As previously announced, Peloton and Lululemon have a new 5 year partnership. Peloton is now the exclusive fitness content provider for Lulu’s various subscription tiers while Lulu is Peloton’s exclusive apparel provider. As a result, Lulu will halt content creation just like it halted Mirror hardware sales. This led to impairment charges discussed already in the margin section.

Margins

Gross margin outperformed thanks to lower freight costs and utilization. Foreign exchange offset some of this strength.

Sales, general & administrative expenses accounted for 38.2% of revenue vs. 36.8% Y/Y. This was actually 50 bps better than expected. The contraction was well-telegraphed and is due to “strategic growth and brand investments.” It’s leaning in.

Product Line Highlights

Its new Wundermost women’s line is its softest fabric to date. This blends Lulu’s edges in “raw material creation, technical construction and fabric innovation to engineer a new sensation and feel for guests.” These competitive edges are highly subjective. What isn’t subjective is Lulu’s consistently strong results.

Men’s shoes will launch in Q1 2024. Its new men’s product lines like Steady State and Soft Jersey performed so well that it’s now “chasing into more inventory.”

“We’re seeing enough positive guest signals that we think we have an opportunity in this shoe category. We’re going to take a long-term view and build it, but we’re excited about what we’re seeing so far.” – CEO Calvin McDonald

Brand Building

Lulu has ample room for rising brand awareness. This is why it’s investing so heavily in growth at this stage. Brand awareness in the USA is at 25% overall and just 13% for men. Total awareness is under 10% in every other market besides Canada (where it started) and Australia. This minimal awareness/long runway for growth with men led Lulu to introduce a successful national joggers campaign in North America for men.

Take

This would be a great quarter for nearly every other player in the space. It’s an average quarter for Lulu simply based on the consistently elite execution & results we’ve all come to expect. The Q4 miss is clearly based on guidance sandbagging while market share gains remain brisk. Was this perfect? No. Is this concerning? Not in the least. Annual guidance was raised and the ambitious 5 year growth targets were reiterated. More execution, more success, and another all-time high for the stock.