AI-Themed Earnings Round-Up – AMD (AMD) & Supermicro (SMCI) – February 3, 2024

AMD (AMD) – Earnings Review

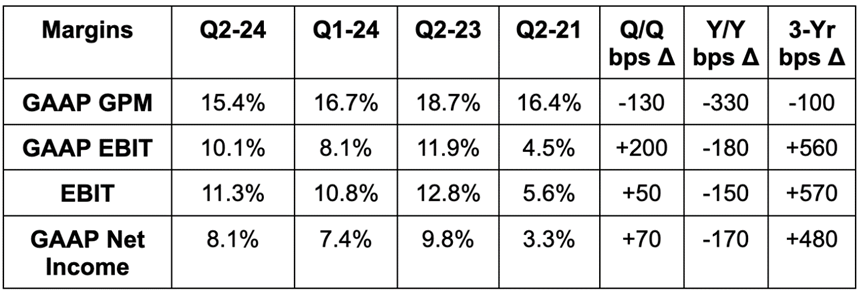

Results:

- Beat revenue estimates by 0.5% & beat guidance by 1.1%. Its 24% 3-year revenue CAGR compares to 27.5% Q/Q & 40.6% 2 quarters ago.

- Missed GPM guide & identical estimates by 70 bps.

- Met $0.77 EPS estimates.

- Missed EBIT estimates by 1.4%.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Balance Sheet:

- $5.77 billion in cash & equivalents.

- $2.47 billion in total debt.

- Inventory rose 15% Y/Y, but fell 2% Q/Q.

- Share count is flat Y/Y.

Next Quarter Guidance & Valuation:

- Revenue was 6.1% light.

- GPM was in line with expectations at 52%.

- EBIT was 1.4% light.

AMD trades for 40x next 12-month EBIT and 47x next 12-month EPS. EBIT is expected to grow by 39% Y/Y in 2024 while EPS is expected to grow by 38%.

Quick Highlights:

Segment Performance:

- Data center revenue rose 38% Y/Y in Q4 vs. 7% Y/Y growth in 2023 as a whole. The Q4 acceleration was thanks to its data center GPUs and embedded high-performance computing CPUs. EBIT fell 31% Y/Y for 2023.

- GPU: Graphics Processing Unit. This is an electronic circuit to display screen images.

- Client revenue rose 62% Y/Y thanks to strength from its high-performance desktop CPUs. For 2023, revenue fell by 25% Y/Y due to PC market weakness. EBIT fell 104% Y/Y for 2023 (turned negative).

- CPU: Central Processing Unit. This is a different type of electronic circuit that carries out tasks/assignments and data processing from applications.

- Gaming revenue fell 17% Y/Y in Q4 vs. -9% Y/Y growth for 2023 as a whole. This was related to semi-custom revenue weakness. Its gaming GPUs helped offset this weakness. EBIT rose 2% Y/Y for 2023.

- Embedded revenue fell 24% Y/Y in Q4 due to inventory reductions. It rose 17% Y/Y in 2023 due to enjoying the first full year of Xilinx revenue post-acquisition. EBIT rose 17% Y/Y for 2023.

Thoughts:

I don’t cover the semiconductor space. Candidly, the science behind the actual efficacy of one chip vs. another is over my head. I think it’s over most investor heads too, which is why I think those wanting exposure should take the thematic ETF route. I put the sector in my too hard pile along with Pharma. Still, I know many of you follow this name closely, so I did want to offer thoughts and value where I actually can here – financials. I will leave commentary on the actual chips to others.

In my view, AMD is racing to catch Nvidia GenAI training & inference chips. The absolutely insane ramp in demand Nvidia enjoyed throughout 2023 leaves many to wonder: Will the entire market be theirs forever? The answer is probably not; AMD is already starting to collect some notable customers in the space like Meta and Tesla. Still, it’s unclear how quickly AMD’s GenAI-related revenue will ramp in 2024. It has released its GPU for AI and “expects a strong ramp” to come this year. I wouldn’t bet against Lisa Su delivering on her promises… but I certainly wouldn’t bet against Nvidia either. In reality, the pie is massive and any meaningful traction within it should be very material for AMD. That’s why it’s receiving one of the steepest multiples that it ever has despite what appear to be lackluster results. I just don’t think its results for Q4 2023 matter all that much. The results are backward-looking. They don’t reflect the anticipated ramp for what are inherently forward-looking markets. Investors are looking ahead to 2024 and gawking at the potential for AMD to even sort of, kind of come close to mimicking Nvidia’s rise. We shall see if that happens.

Supermicro (SMCI) — Earnings Snapshot

Results:

SMCI already pre-announced results, so these numbers aren’t a surprise. What is a very positive surprise? The robust forward guidance that it gave.

Source: Brad Freeman – SEC Filings, Company Presentations, and Company Press Releases

Guidance & Valuation:

SMCI raised its annual revenue guidance by 26.1% to $14.5 billion. That is not a typo. Next quarter revenue guidance was a whopping 44% ahead of estimates. GAAP net income guidance was 38% ahead of estimates. Net income guidance was 20% ahead of estimates. Strong.

Even following explosively positive price action, SMCI trades for 17x 2024 EBIT and 22x 2024 net income. EBIT is set to grow by 94% Y/Y and net income is set to grow by 90% Y/Y.

Balance Sheet:

- $726 million in cash & equivalents.

- $376 million in debt.

- Diluted share count rose 3.4% Y/Y. Basic share count rose 1.8% Y/Y.

Thoughts:

This quarter was simply incredible. If you own this name, take a bow and enjoy your incredible returns. It is time for you to take the victory lap. You have earned it. I’m unfortunately watching from the sidelines. The only thing that I’ll say is that it’s likely not realistic to expect this rate of growth to continue for the long haul. The GenAI boom is real, and SMCI is among the best positioned to take early advantage. Nvidia and Microsoft are the only others in that same conversation in terms of direct financial impact today. Does it matter if SMCI’s growth slows? Not really. 2025 revenue growth estimates of 29% Y/Y will do just fine considering the firm trades at valuation growth multiples well below 1x. From this point of view, it’s still somehow one of the cheapest names in growth land.