Dear Investor,

I’d like to tell you about an investing product that’s taking the world by storm – making up nearly 50% of all ETF inflows recently – why it matters to you, and how you can get started enjoying its benefits with exclusive access to an index from a research firm.

It’s called smart beta.

You may know about it already. Smart beta is just indexing, but unlike market capitalization-weighted indexes like the S&P 500, smart beta indexes use other factors.

One in particular blew my mind – in a subdued, smart beta way. I’ll tell you about it in a moment.

But back to factors. They’re the magic of smart beta. A smart beta strategy could be as simple as equally weighting the stocks in an index – or as complicated as optimizing across dozens of factors.

Importantly – and newbies seem to miss this – smart beta targets the most important part of your portfolio: your baseline, biggest-building-block investments.

A “Boring” Investing Method Made Investors a Fortune

Novice investors tend to fixate on finding the one big winner. Or maybe a few. But same idea.

Moonshot investing (or is it gambling?) is tempting. It’s even OK to pursue in a right-sized portion of your portfolio – but it’s probably not an ideal main course, per prevailing financial advisor wisdom as well as academic studies.

In “Contrarian Investment, Extrapolation, and Risk,” Josef Lakonishok, Andrei Schleifer, and Robert Vishny – I’ll call them “LSV” for short) sorted stocks into deciles, or groups of 10, by two factors: earnings yield (E/P, which is simply the inverse of the P/E ratio) and historical sales growth.

What they found was amazing – and broadly lends support to “boring” investing methods like the smart beta strategy we’re about to get to.

First, LSV found that low P/E stocks beat high P/E stocks by 4.3 percentage points per year.

Sure, this happens more in some years and not at all in others, but this alone is a powerful finding.

Next, they sorted stocks by historical sales growth. Again, companies with the slowest historical sales growth – the boring, unloved “nobodies” – outperformed their faster-growing counterparts by 7.3 percentage points per year.

Take that in.

But – brace for it – the real magic happened when LSV combined these two factors. A portfolio based on low P/E and low sales growth outperformed its “glamorous” opposite by 11.3 percentage points per year!

These results were so good that LSV started their own fund – LSV Asset Management – that now manages roughly $100 billion.

An introduction is in order…

Carlos Diez is a name you may not know yet, but he’s the founder of MarketGrader, a firm that aims to harness this very same power of combined factors, in a smart beta format.

Rather than just E/P and sales growth, Carlos’ team of researchers uses 24 factors – mostly fundamental factors, of the same ilk as E/P and sales growth – to create large portfolios, often of hundreds of stocks. By leveraging many factors and many stocks, Carlos aims less to “throttle” the market like LSV, but rather to reliably outperform it on a risk-adjusted basis.

And it’s worked: A full 47 out of MarketGrader’s 52 indexes have outperformed their benchmarks, generally for more than five years. And MarketGrader’s indexes have beaten their benchmarks by more than 4 percentage points, on average, annually, for more than a decade.

At BBAE, we challenged Carlos to give our investors a smart beta index based on a strategy that’s tested to beat its benchmark.

Carlos returned with three. We spun them into portfolios available in the MyAdvisor section of the BBAE app: the MarketGrader Core Portfolio, the MarketGrader Growth Compounding Portfolio, and (BBAE co-founder Barry Freeman’s favorite) the MarketGrader Growth and Income Portfolio. You can learn more about them here.

BBAE’s smart beta: all about performance

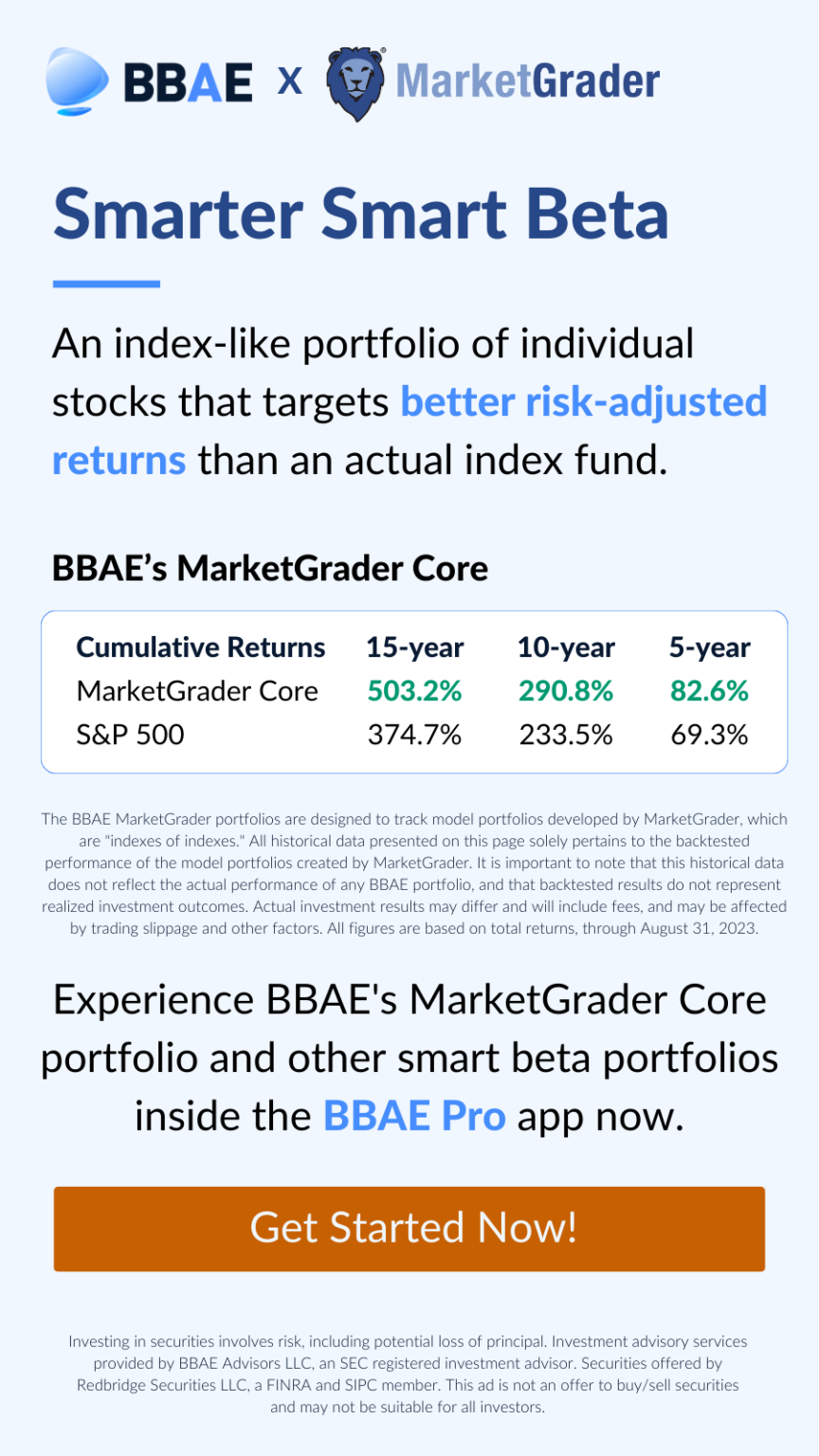

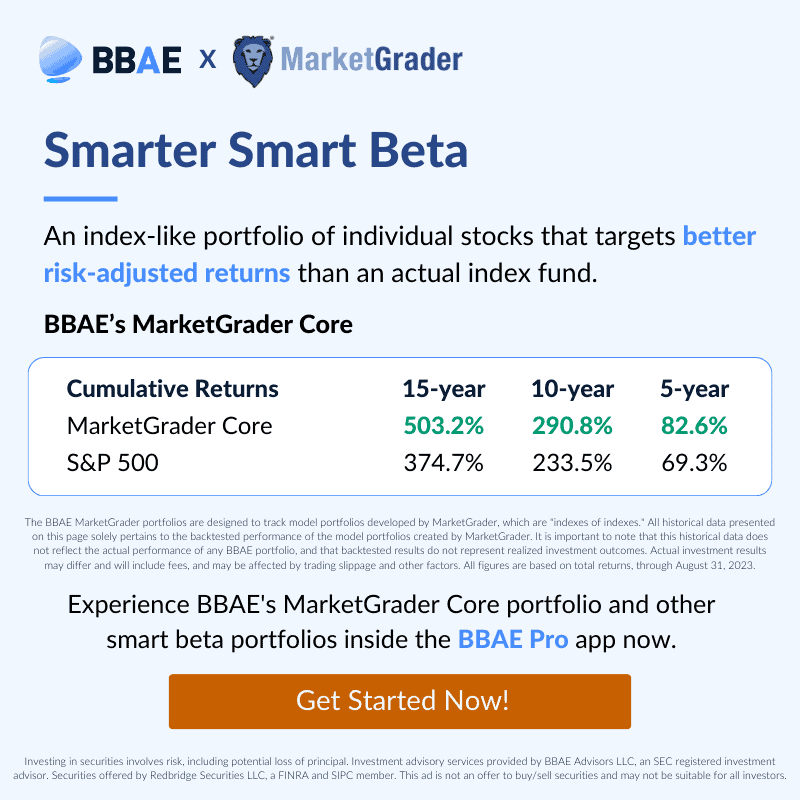

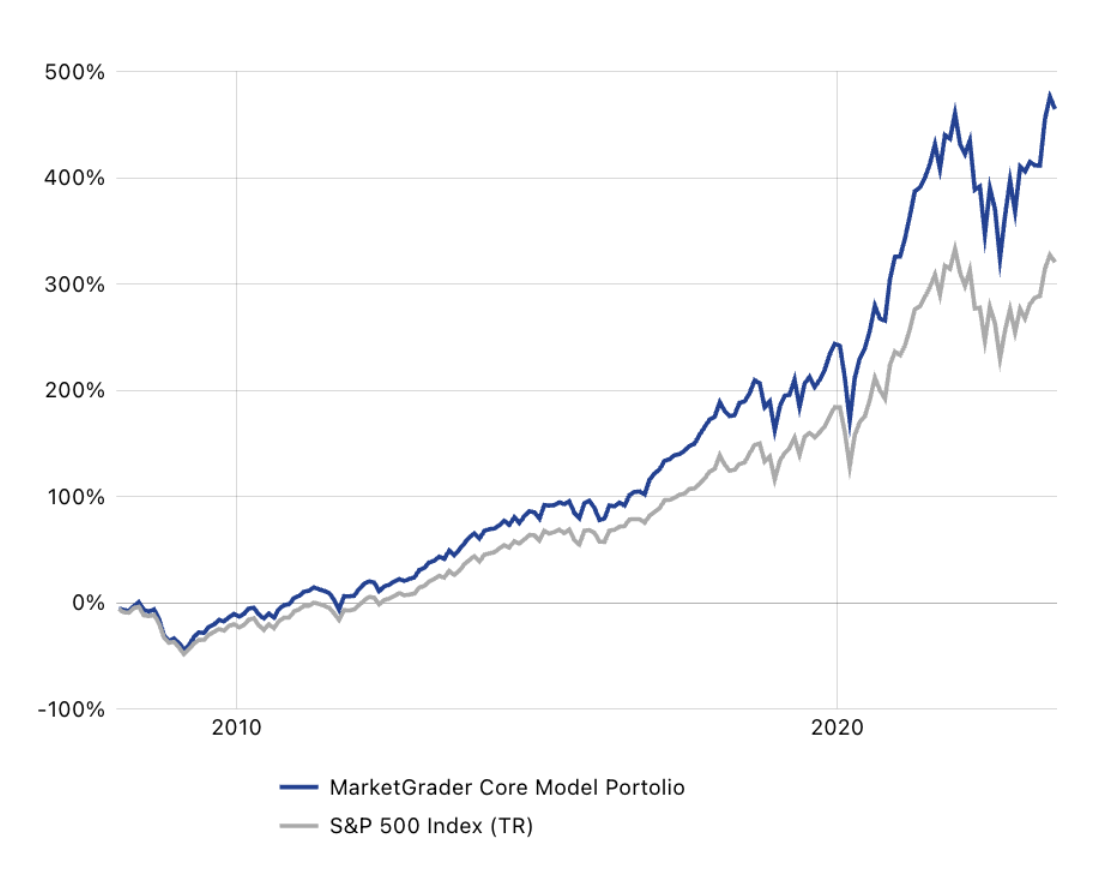

The backtested results of the MarketGrader index that we base our Core Portfolio on, for approximately the past 15 years, are below. As you can see, it’s doing exactly what we’d want smart beta to do: beat the benchmark on a risk-adjusted basis.

The main reason to consider BBAE’s smart beta specifically is performance: if – and I should stress that the portfolios are new – the portfolio performance continues to match the outperformance above, investors will benefit rather massively from better long-term returns (achieved with similar-to-market risk, as proxied by standard deviation).

Look at the difference seemingly modest yearly outperformance makes when compounded over decades:

Why else would you choose BBAE’s smart beta portfolios?

- Low minimum managed account investments: If you know about managed accounts, you know that minimum balances of $100,000 or even $20,000 are not uncommon. BBAE lets you get started with $2,000.

- Transparency: Unlike with a fund, you actually own all the shares (or fractions of shares) in your BBAE managed account, meaning you can see exactly what you own at any time.

- Affordable, straightforward fees: Your entire balance is managed for a fair 0.50% yearly management fee.

And here’s the backtested performance of the indexes BBAE’s three smart beta portfolios are based on:

| MarketGrader-BBAE Smart Beta vs. Benchmarks (15+ year backtest through August 2023) | |||

| Cumulative Return | Annual Return | Standard Deviation | |

| MarketGrader- BBAE Core | 465% | 11.7% | 17.1% |

| MarketGrader-BBAE Growth | 502% | 12.1% | 17.9% |

| MarketGrader-BBAE Income | 461% | 11.6% | 17.2% |

| S&P 500 | 321% | 9.6% | 16.2% |

| Dow Jones Select Dividend Index | 234% | 8.0% | 16.4% |

We’re excited about the BBAE’s new smart beta portfolios. We believe they’re among the best smart beta offerings out there.

To check out BBAE’s smart beta offerings, first open a BBAE account – it’s easy, and you can get up to $400 in BBAE Dollars just for opening it!

Click here to explore BBAE’s smart beta portfolios.