Nvidia Is Now the World’s Largest Company – or Is It?

If you needed a reminder about the power of luck in the financial world, it’s Nvidia.

I’m not taking anything away from Nvidia (Nasdaq: $NVDA) or people who invested in Nvidia, but if you read its history, it’s clear that Nvidia was a well-run company that was all about video game graphics units – and those GPUs were accidentally positioned to catch the AI wave.

Hey, luck is fine – virtually no person or company gets really successful without some luck. (Many people were accidents, too, and most probably turned out well.)

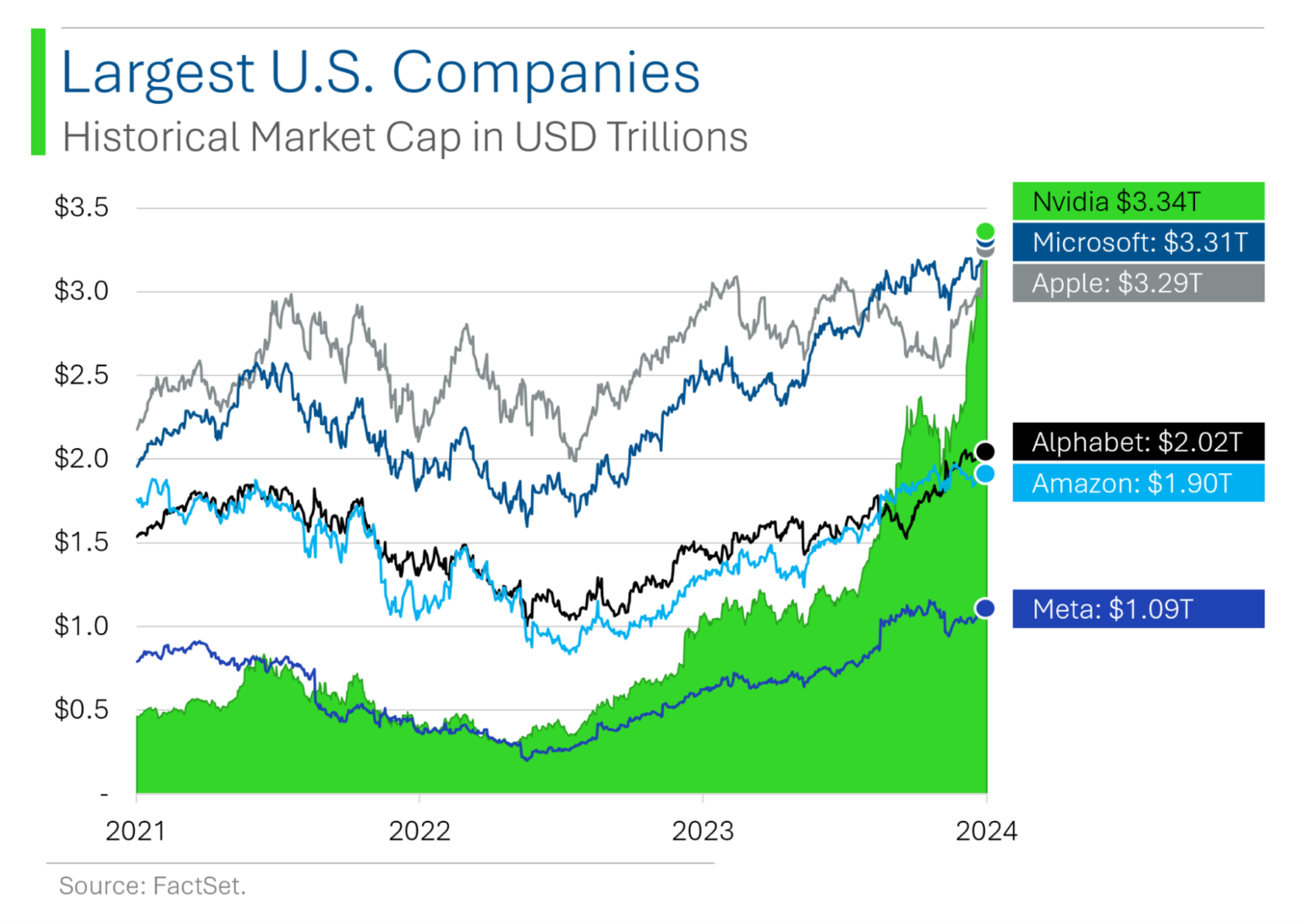

But what I want to highlight is that while Nvidia surpassed Apple (Nasdaq: $AAPL) and Microsoft (Nasdaq: $MSFT) to become the largest company in the world by market capitalization, market cap is only one way to measure the size of a company.

The other two main ways are revenue and employees.

If we’re OSHA, if we’re a labor union, or if we’re selling long-term care insurance policies, we care very much about employee count.

If we’re investors, we prefer revenue, because employees are a cost center and revenue is closer to what we “own” – in a theoretical sort of way – as investors.

Now, how we define “biggest” can make all the difference, as the following two charts show:

- Walmart (NYSE: $WMT) – which is the largest company in the world by both revenue and number of employees, looks miniscule compared to Nvidia on a market cap basis.

- Nvidia looks miniscule compared to Walmart on a revenue (and employee) basis.

If we consider this data and nothing else, Nvidia looks ridiculously overvalued.

Walmart’s 2023 revenues were 10.6 times higher. Yet Nvidia’s market cap is more than 6 times Walmart’s.

Put differently, Nvidia’s price-to-sales (P/S) ratio (from Ycharts, which uses LTM revenue figures, which will differ a bit from calendar or fiscal year sums) is 42.4 as I type this, whereas Walmart’s is 0.83.

Nvidia’s P/S ratio is 51 times that of Walmart’s.

Walmart isn’t sexy, but it’s clearly a good business – one of the best retailers on the planet. Nvidia may be a better business, but is it 51 times better?

That’s one perspective. In fact, to further it, I’ll paraphrase a point made my former colleague Eoin Treacy when we spoke today (catch our interview on the BBAE Blog, or on YouTube): Would you buy a business that, pretending it had no costs whatsoever (and of course it will have costs in real life), would take you 42.4 years (P/S ratio) just to return your original purchase price? This is before any investment return – it’s just getting your purchase price back.

Of course, nobody would buy such a business. But, yet, people are buying Nvidia.

In investing, there’s always an opposing view

There is another perspective.

The other perspective is that the former perspective ignores two things:

- Profitability

- Growth

Sales won’t stay the same for 42 years, this more optimistic perspective goes. They’ll grow. And as equity investors, we really shouldn’t focus on sales too much anyway. What we really care about is earnings.

And on an earnings basis, Nvidia is bigger.

This is a plot twist.

First, it shows the uselessness of the P/S metric – rightfully regarded as the lowest-quality (i.e., least information-containing) valuation metric.

Second, it shows the power of profitability. Nvidia’s revenue nearly looks like rounding error compared to Walmart’s, but Nvidia is squeezing twice as much absolute profit out of its “tiny” revenue than Walmart is from its world-leading revenue.

Profit matters far more to shareholders because they “own” it, at least conceptually.

And then there’s growth. Equity investors do not actually buy trailing profit (or trailing sales, or any trailing stream). Those are just proxies for future growth.

And on earnings growth rate, Nvidia has been thumping Walmart:

What will Nvidia’s future earnings growth be, and will be enough to justify the stock price?

This is likely the key question for any current or prospective Nvidia shareholder. Everyone knows that AI will be big, and everyone knows that Nvidia is a great company. Those two things alone are not enough to buy Nvidia, though (still, I’d guess that a lot of investors are buying Nvidia for just those two reasons).

In fact, it’s easy to identify the best of something: the best restaurant, the best car, the best rookie player to add to a sports franchise. It’s much harder to decide if the “best” is worth the current market price.

That dynamic becomes more difficult still with stocks, because the benefit is probabilistic and generally comes years into the future. Because the reinforcement loop is so vague, delayed, and imprecise in investing, balancing price vs. benefit is especially hard. But that also means there’s disproportionate reward potential for investors with the discipline to learn to do it well.

I have not dug into Nvidia well enough to comment, other than to say that at current prices, my guess is that AI would have to really take off as a percentage of the global economy for Nvidia’s valuation to be cheap.

A covered call option play on Nvidia?

Enrique Abeyta, founder of HX Research (and friend of BBAE; catch our interview here), pointed out today that month-out calls on Nvidia with a strike price of $140 (which is roughly $10 more than the $130-ish Nvidia trades at today, meaning these one-month calls are out of the money), trade for $4.35 per share, or $435 per contract, given that options trade in contracts of 100.

(Depending on when you’re reading this, the prices will have likely moved somewhat, but I trust you’ll get the general idea.)

That price feels mighty expensive to Enrique, and frankly to me, too (Enrique and I haven’t discussed this and he has no idea I’m writing this column). While I’d be scared to short Nvidia, if I owned the stock, which I don’t, I’d likely be looking to write some covered calls to take advantage of what feel like very high near-term option prices.

I’m saying this neither as a recommendation (we don’t make them at BBAE, and don’t infer it to be one from Enrique, either), nor as the focal point of this article – rather, I’m trying to guide readers to two principles:

- NEVER take a one-sided view of an investment. There’s always another side. Usually (not always) it has at least some merit. (This doubles as good life advice, too.) And if the stock is “perfect,” then the price is usually too high. To quote Charlie Munger’s quoting of German mathematician Carl Jabobi: “Invert. Always invert.”

- You can do more than buy or sell. Stocks aren’t one-dimensional, and neither are your investment options. Avoiding a stock unless you have high conviction is usually the best option. But if you’re nearly sure it’s ridiculously overpriced, you could consider short selling it. Or if you own it and feel it (or at least call options on it) are a little rich, you could benefit by writing covered calls. BBAE has ample option resources at your disposal if you decide to explore that path with any stock.

There’s always more than one way to look at an investment, and usually more than one way to seek to profit from it.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.