News Roundup: S&P 500 2025 Predictions, Lousy Retail Investor Performance, Europe Wanes, Simple ETFs

S&P 500 predictions for 2025: Still of little value

Santa Claus. The Tooth Fairy. Accurate S&P 500 predictions.

There are things that people want to believe in – for fun, for a primal desire for the comfort of order and certainty, or for some other reason – but which simply don’t exist.

Evidence shows that stock market price targets belong in that bucket.

But with 2025 on the near horizon, prognosticators are doing their jobs of predicting anyway, or at least trying to. Problem is, as Sam Ro of Tker.co points out, their forecasts a) don’t tend to be accurate, and b) tend to assume “average year” returns – which is defensible and understandable from a career perspective, even if the market itself seldom delivers average returns.

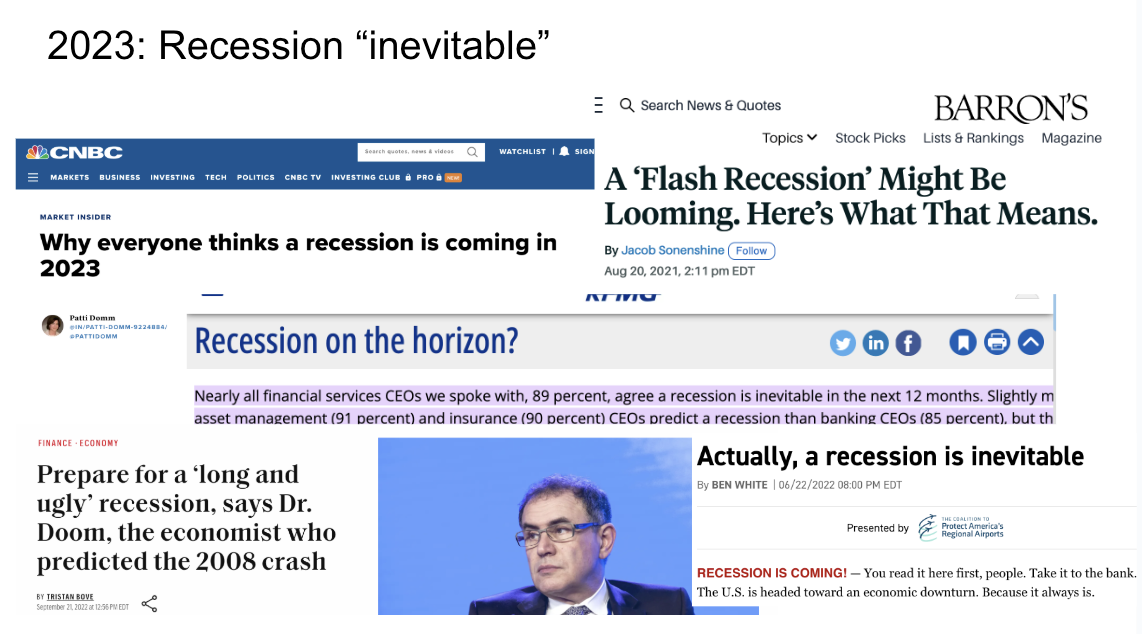

See the below slide from a presentation I gave in December 2023, showing opinions (from 2022) that a recession was coming in 2023; additionally Bloomberg-collected estimates were for the S&P 500 to drop.

In reality? No recession in 2023. Inflation abated. Wage growth even surpassed inflation. And the S&P 500 rose 23%.

“Experts” were completely wrong.

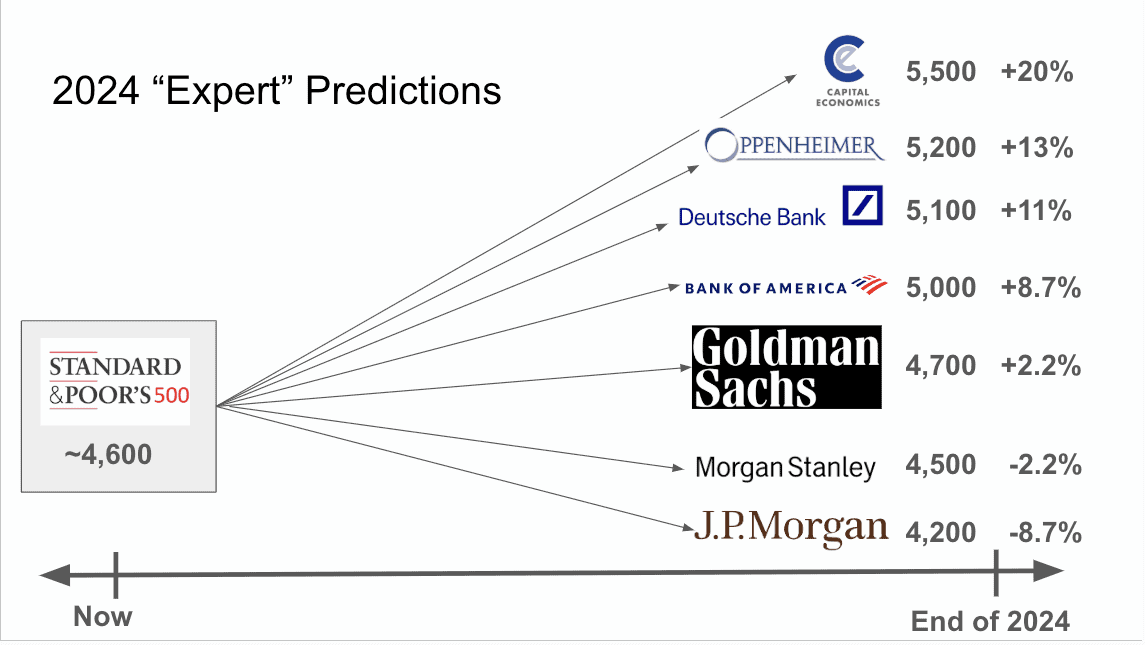

Another slide I showed was where Wall Street “experts” thought the S&P 500 would end the year at.

It’s currently at 5,917, surpassing even the most bullish of the bullish forecasts.

“Experts” were completely wrong, again.

The forecasters are smart people. They have lots of data, and fancy computer models. I’m sure they mean well, and put a lot of effort into what they do (if only to show defensible logic).

But economics is a social science. Price targets have the allure of specificity, but not much more.

Retail investors up 3.7%. S&P 500 up 25%

That the S&P 500 is up 25% year-to-date should be great news.

It’s certainly great news for investors owning S&P 500 index funds.

But it might make the average retail investor feel a little bad by comparison – because, according to JP Morgan, the average retail investor is up just 3.7% year-to-date.

That’s sad and fascinating at the same time.

If you’ve been reading the BBAE Blog, you know that retail investors tend to chase things – especially past performance. Chasing things might work out when there’s a ton of momentum in a market, but in general, over time, it hasn’t worked well and retail inventors have consistently underperformed passive indexes – usually by a large margin.

Dalbar Research has similarly looked at US mutual fund investors over trailing 20-year periods, and has found that while the S&P 500 has tended to deliver around 10% annually (returns in theory available (minus relatively small fund fees) to anyone who buys and holds an S&P 500 index fund), the average mutual fund investor scored just 4% annual returns.

This is depressing, but this is also inspiring, because it shows how much cognitive bias the average investor succumbs to – that means more money to be made, at least potentially, by investors with the savvy to not succumb to cognitive bias. Warren Buffett’s steely, rational demeanor isn’t an act – it’s a major asset in investing.

The problem retail investors face is, not coincidentally, the same trick exploited by casino and lottery folks: There’s always some moonrocket stock that did well in short order, or some young investor who went all in on something and made a fortune.

Rick Guerin was the “Fifth Beatle” of Berkshire Hathaway. He helped Berkshire find many of its early successful investments. But as Buffett explained in a 2013 interview, he had less patience than Warren and Charlie:

“Charlie and I knew we were going to be rich. But we weren’t in a rush.

Rick Guerin was just as smart as us. But he was in a rush to get rich. He was levered with margin loans, and in the crash of 1973 he had to sell his Berkshire stock to me for $40 a share.”

With patience, Rick would have been a multi-billionaire: The Berkshire Hathaway A shares that Rick sold for $40 currently trade for $710,000 each. It’s hard to not succumb to cognitive biases, but that’s also why the rewards of avoiding them are so great.

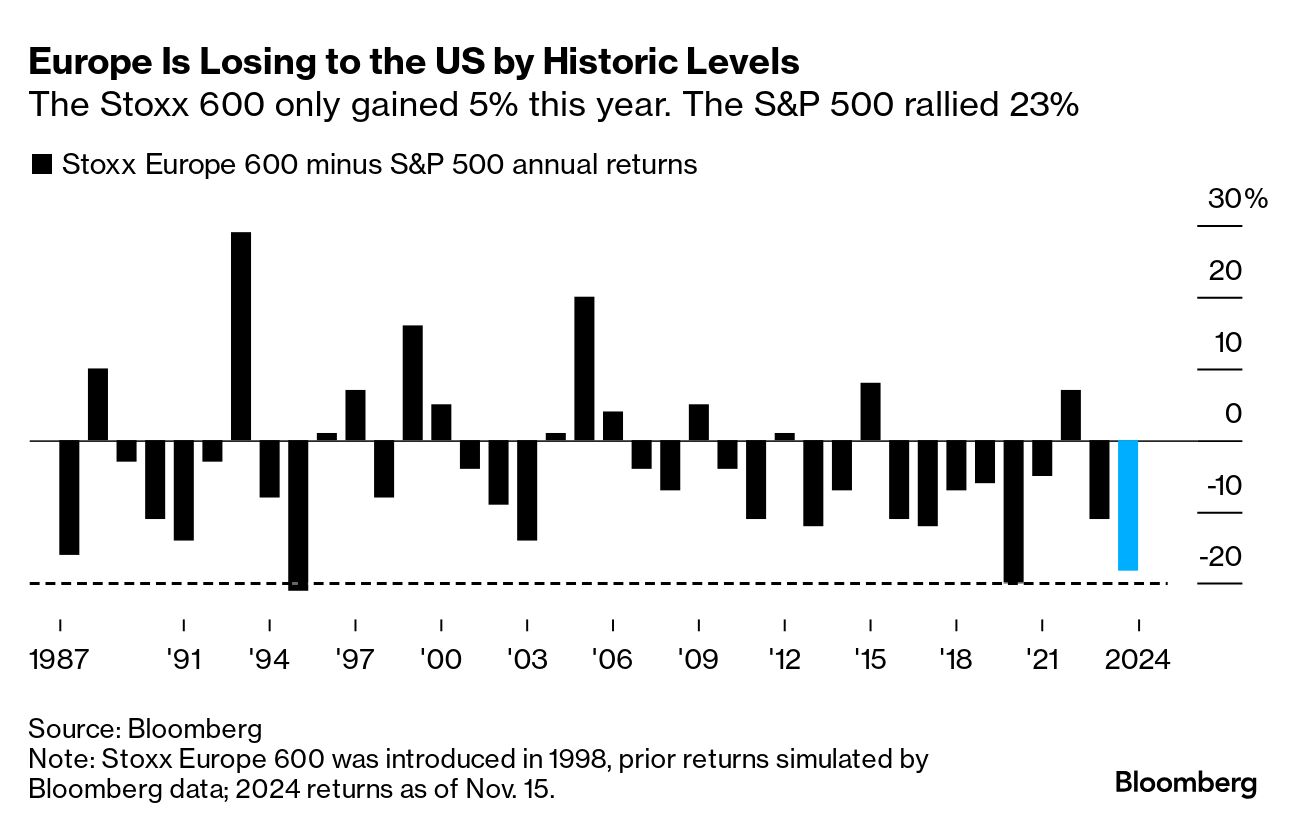

European stocks: Performing almost as poorly as American retail investors

This doesn’t need much explanation – especially to anyone who’s waited until Monday to receive a reply to a Friday email sent to a European.

Europe has massive productivity problems (I mentioned this topic getting airtime at the Yahoo! Finance Invest conference last week). I don’t see a catalyst for change. And, from a certain perspective, it’s their choice to slow down. Just don’t expect good returns from investing there.

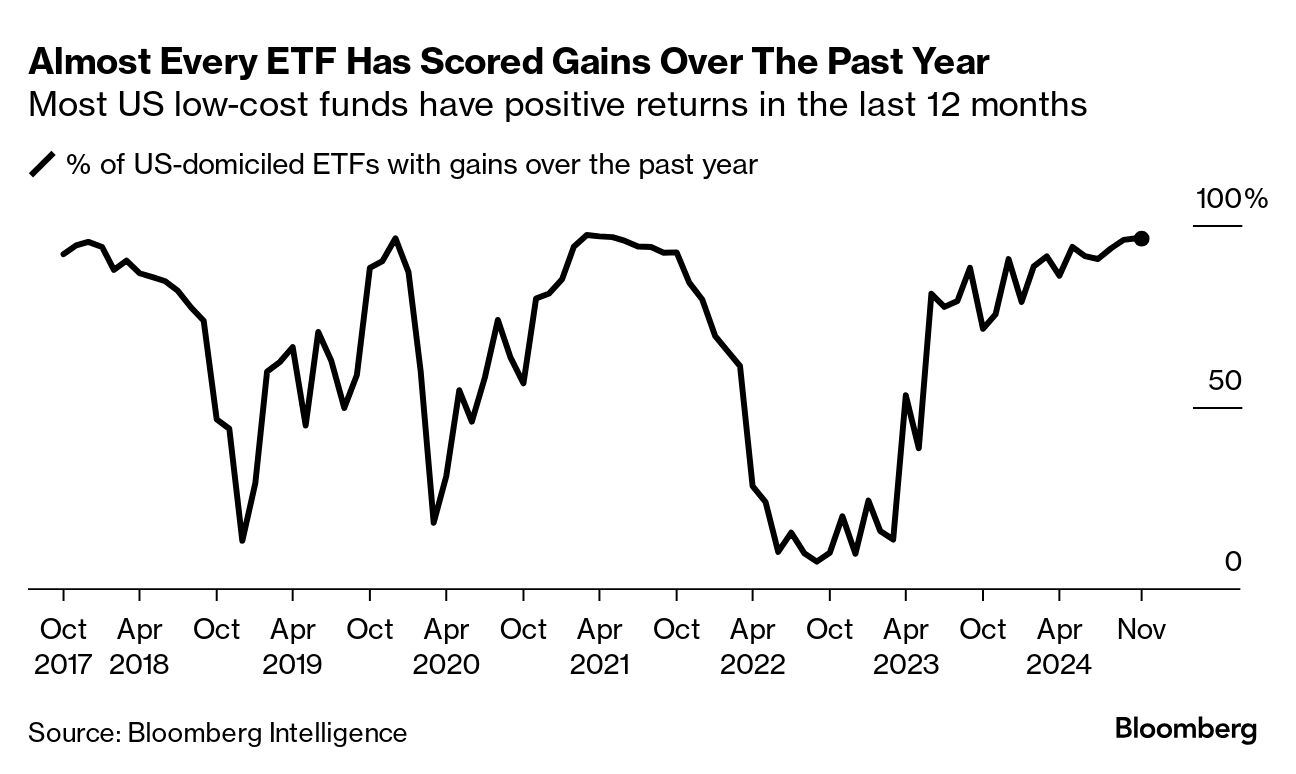

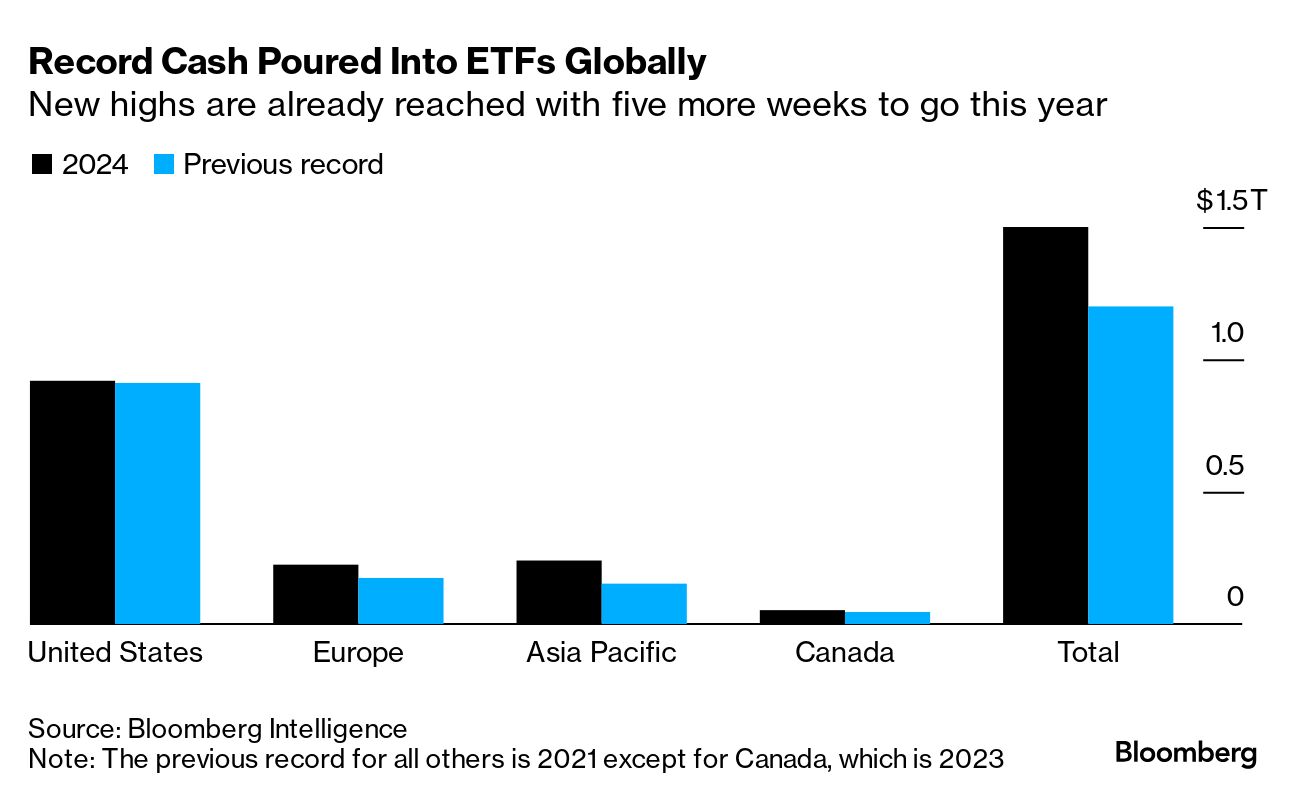

ETFs on a tear, except the fancy ones

Bloomberg Intelligence notes that 96% of ETFs have delivered positive returns – often double-digit positive returns – over the past year. The average US-traded ETF is up 14% over the past 12 months.

Bloomberg quotes Bloomberg Intelligence analyst Athanasios Psarofagis: “Not only are ETFs generally inexpensive, but it would have been virtually impossible to lose money this year.”

The worst performers are the high-fee, fancy ETFs, which Bloomberg describes as “too complex for their own good.”

A few points of commentary:

1) Complexity is usually – not always, but usually – a bad thing for investing returns. I believe this is supported by academic research. Complexity often leads to high fees without higher returns. So Bloomberg’s finding makes sense.

2) A lot of the more complex hedge fund-style strategies lean toward either absolute returns (generally modest returns, but regardless of market condition) or hedging, and in a bull market those will lag by definition. If we were to suddenly get a bear market, some of them would suddenly look smarter. I am not defending them categorically by saying this – Wall Street, almost by definition, is all about charging high fees for complexity and expertise; rather, I’m saying that there’s an insurance-y element to many strategies that doesn’t show its value in an “up” market.

3) Some of the spicier leveraged ETFs are designed for day traders (they “reset” daily in a sense), and their long-term returns are highly path-dependent and often in a non-intuitive way – in other words, their 12-month returns may look “weird” but they’re only designed to have a daily benchmark: If they’ve doubled or tripled or 1.5x-ed or whatever their underlying investment (Nvidia, the S&P 500, or even Berkshire Hathaway) every trading day, they’ve done their job. That said, if their underlying asset’s returns are generally trending up, they tend to trend up – often powerfully so. Often, but not always: Bloomberg earlier referenced a Granite Shares 3x daily leveraged MicroStrategy product that was down 82% despite MicroStrategy’s rising 100%. (See the BBAE Blog article about this here.)(See the BBAE interview with GraniteShares CEO Will Rhind here.)

I don’t love high fees. I’m not against hedging (“insurance”), and in a bull market, hedging looks boneheaded. And leveraged “daily return” ETFs arguably shouldn’t be evaluated.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.