Higher Interest Rates, US Consumers, Bitcoin, and a Featured Stock

Welcome, BBAE Blog readers!

I’m testing a news recap with commentary format this week, along with a featured stock (not a recommendation, of course) at the bottom.

I hope you find this format helpful.

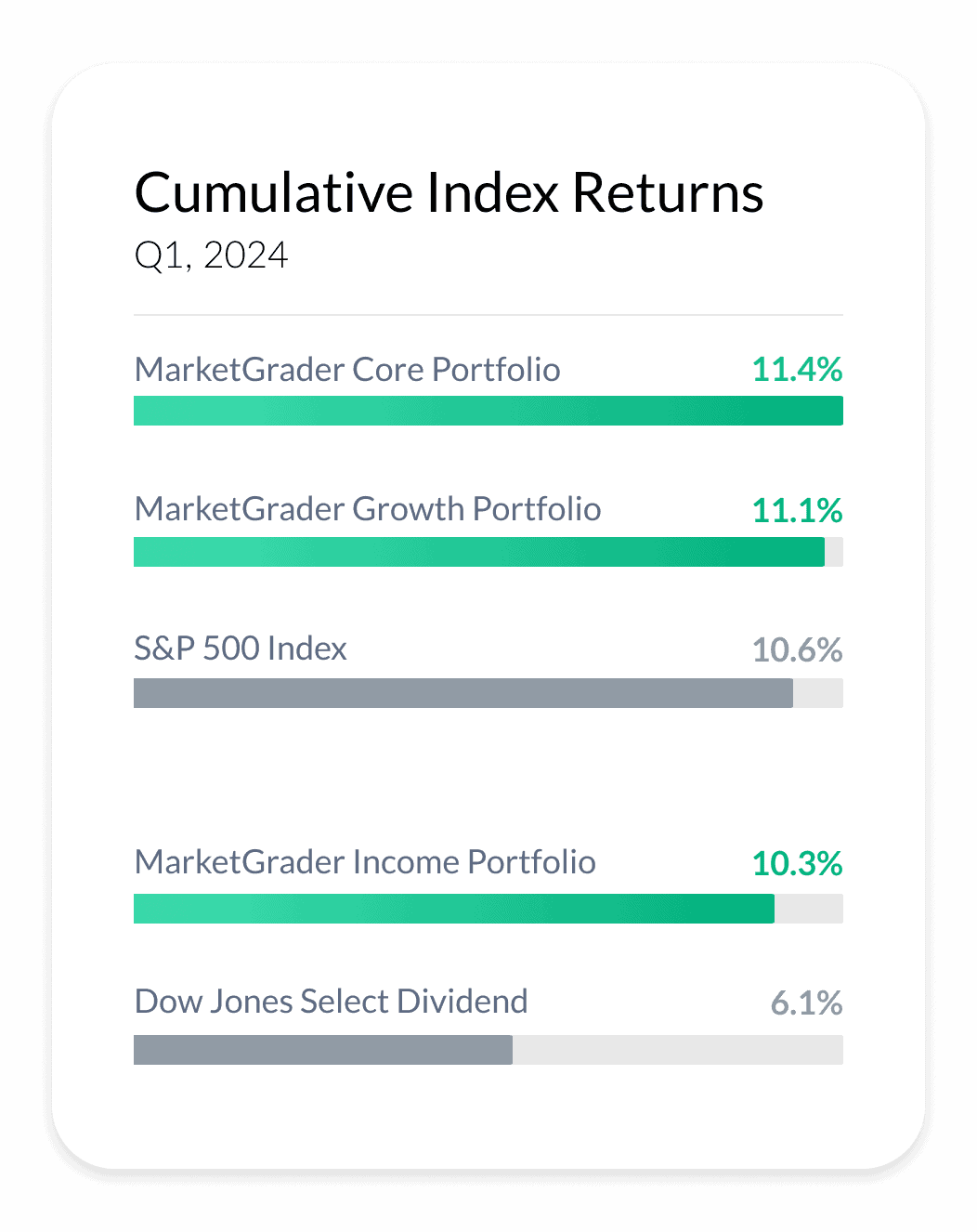

MarkerGrader Beats Benchmarks

Before the news, allow us a tiny victory lap. As our CEO Barry wrote last week, the first quarter of results for our three BBAE MarketGrader portfolios (found in BBAE MyAdvisor) is in. While MarketGrader’s indexes in general have beaten their benchmarks over the past 10 years, and while the three indexes our portfolios follow performed excellent in backtests, there’s something special about seeing real-world benchmark-beating results roll in.

It’s only a quarter, and past results don’t guarantee future performance. But it’s a good feeling when things work as intended, and we’re proud to offer MarketGrader portfolios here at BBAE.

If you’d like to learn more about the BBAE MarketGrader portfolios – smart beta portfolios designed to serve as better-than-an-index fund core positions in your roster – it’s easy! Just click here.

Interest Rates: Higher for longer

You might have noticed two things in the past week or so:

- Stocks have gone down

- Stocks appear to have gone down because Jerome Powell (Chairman of the Federal Reserve) has indicated that interest rates will stay higher for longer.

You might also know that “interest rates” is an overly broad term in that context: The Fed doesn’t set all interest rates.

It sets (technically, influences) the Fed Funds rate, which is the rate that Fed member banks (all nationally chartered banks and some state banks) charge each other on overnight loans to make sure they’re keeping enough “Fed Funds” on deposit at the Fed. And after the Fed began paying interest on Fed Funds deposits, Fed Funds lending became less of a thing anyway.

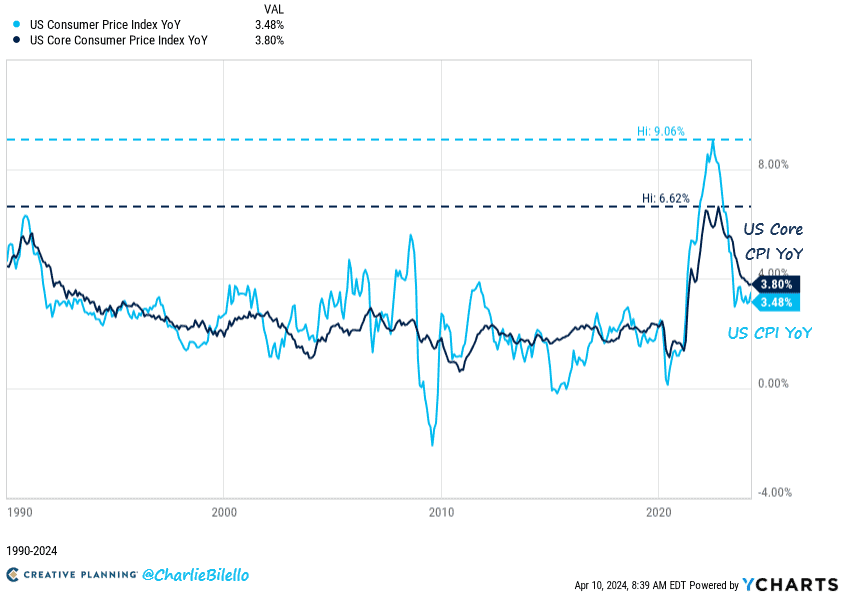

Anyway, the issue here is that while inflation isn’t really bad, it’s not getting better. Blogger Charlie Bilello notes that the US just had its first uptick in core inflation (minus food and energy costs, which are volatile) since March of 2023.

It was a teeny tiny uptick – from 3.76% to 3.80% – but an uptick nonetheless.

Source: Charlie Bilello

In a lesson on how unpredictable economics can be, back in December, futures markets were predicting a > 80% chance of a March rate cut. Now, people are wondering if the Fed’s next move might be a rate hike.

Source: CNN

So against this backdrop, it’s no surprise why stocks are down. Higher interest rates are like a brake pedal (at least in normal market conditions) for an economy, and to the extent that stocks follow the economy, for stocks, too.

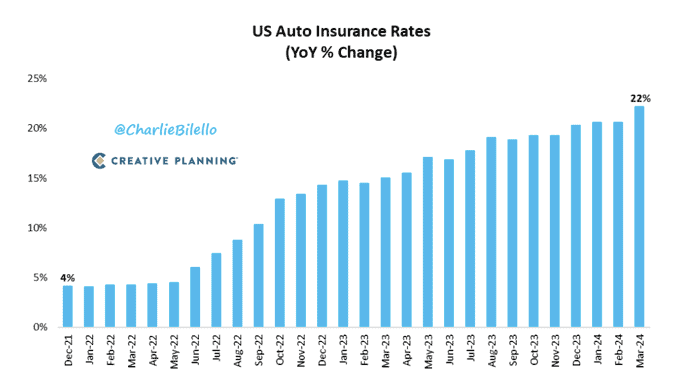

Incidentally, inflation is mostly high from transportation, electricity, and medical care price increases, but one more chart Charlie showed caught my eye. Who knew car insurance rates had been rising so quickly?

Source: Charlie Bilello

US consumer: Healthy or not?

Sam Ro of Tker.co makes a great contrary point about the health of the US consumer (important to the US economy because US consumer spending has typically been about ⅔ of GDP, which is one of the highest ratios among developed economies).

Sam argues in his article that contrary to prevailing wisdom, the US consumer (i.e., the US individual) is financially healthy.

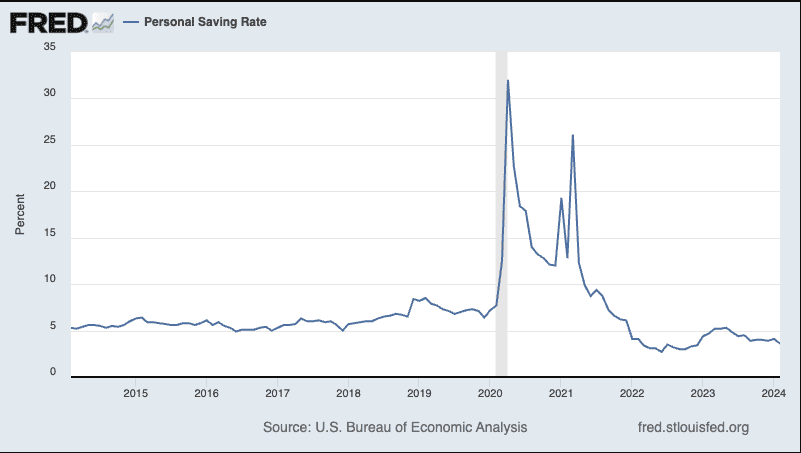

But in first presenting the opposing case, he cites a few legitimately compelling data points, including the unimpressive US personal savings rate:

Source: FRED; cited by Sam Ro

Sam also cites research from Wells Fargo and Renaissance Macro claiming that increasing wealth can lower saving rate, as people feel less need to save.

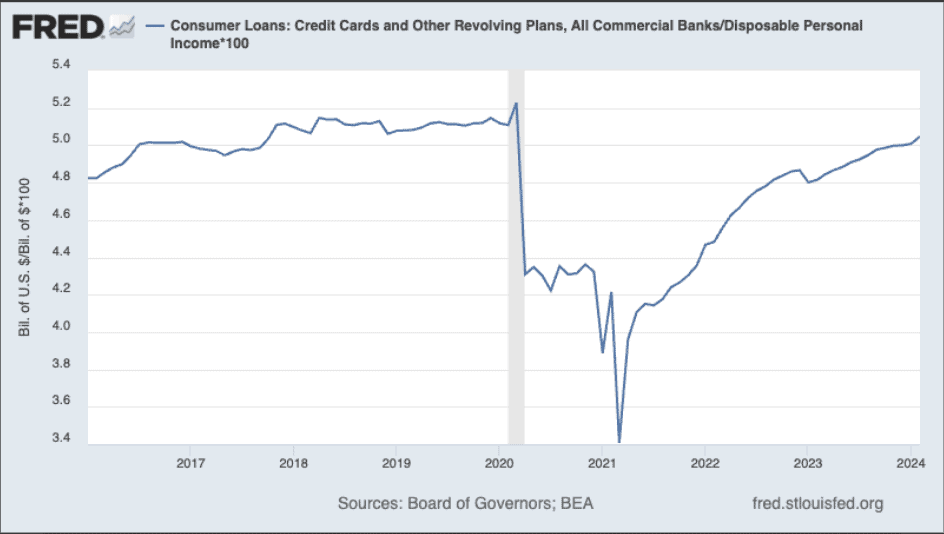

Another bearish point is that consumer loans as portion of disposable personal income have climbed back up to pre-pandemic levels.

Source: FRED; cited by Sam Ro

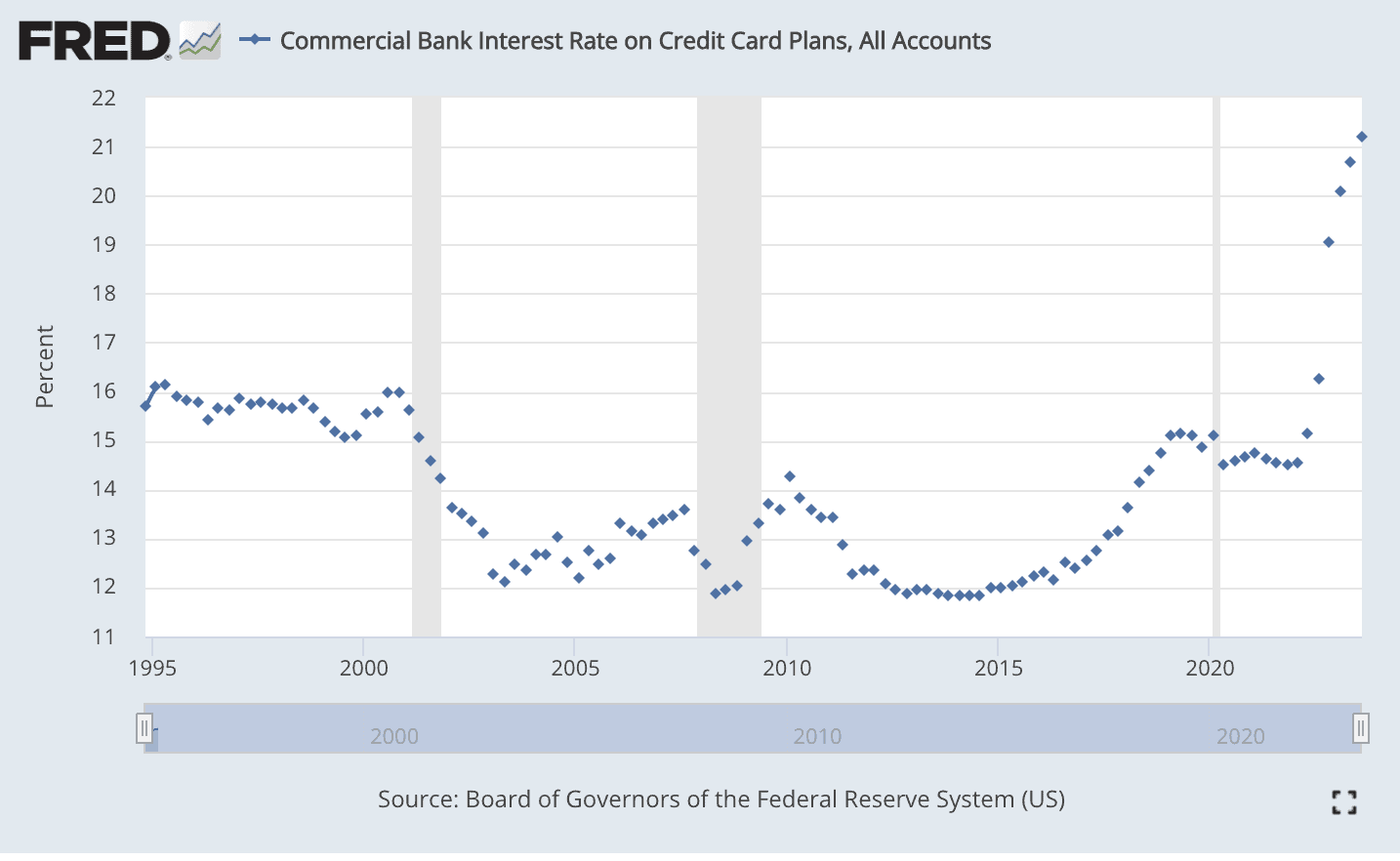

I’ll add another FRED graph (below) to make it even worse: Consumer interest rates are a lot higher now than in pre-pandemic times, so even if the debt principal levels are comparable, the debt burden is far higher, for the same reason that homebuyers can generally only afford half as costly a house with mortgage rates at 7% instead of 3%.

Source: FRED

Sam notes that per the NY Federal Reserve, credit card limits have risen over the last few years, and consumers have quite a bit of available credit before they’re maxed out.

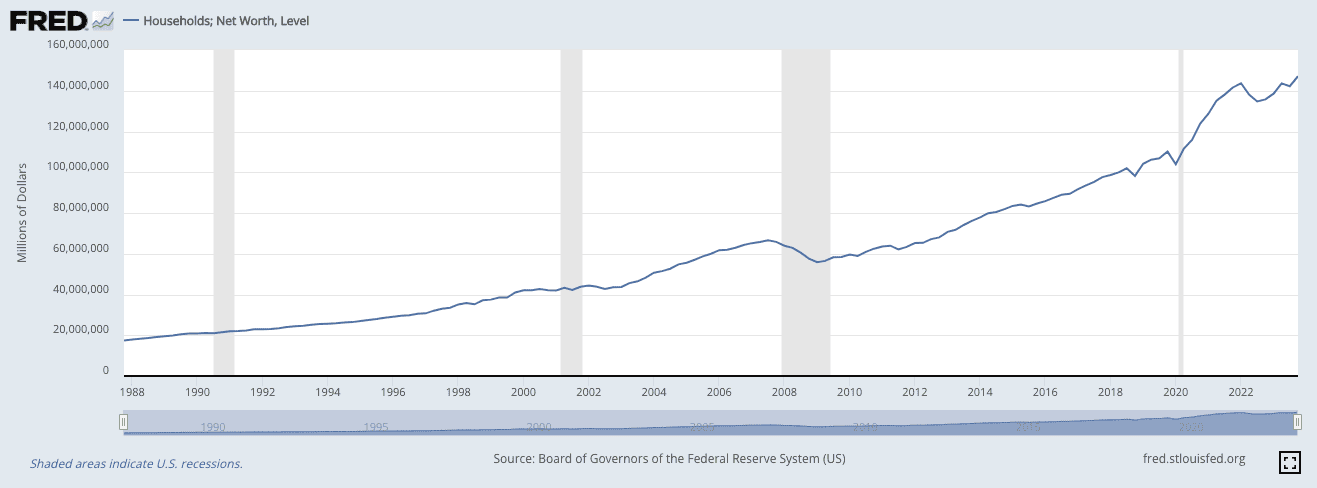

I’d take that as a small positive, but not a big one. And, yes, American households have their highest net worths ever, which is great:

Source: FRED

But looking at the FRED chart (which shows household net worth, in case it’s hard to read, and begins in 1988), you can see that that’s true most of the time.

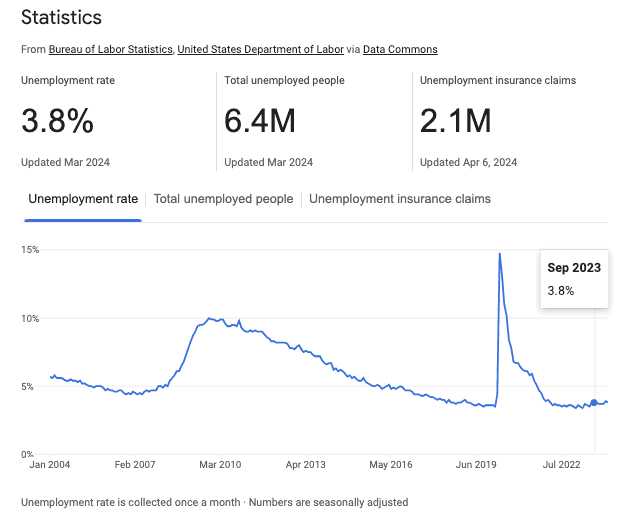

I think Sam is broadly right in that the sky is not falling for the US consumer. Most importantly, the US has an incredibly strong job market (see below), and wages have been growing faster than inflation lately.

For years, alarmists have warned that the sky is about to fall, and for years, they’ve been wrong. That doesn’t mean it can’t happen. It likely does mean – and this is a good thing – that moderately higher-than-expected inflation is not enough to make it happen. It’s possible to tell all sorts of stories by cherry picking economic statistics, but I personally think any real trouble would be indicated by a rise in unemployment along with price growth rising back above wage growth.

Source: Google

Bitcoin: Meme stock, not a safe haven

One of the original selling points of bitcoin was that it was supposed to be digital gold: a refuge, or at least an independent-moving investment, uncorrelated with traditional financial assets.

Except it’s not.

In the past few weeks we’ve had an inflation scare in the US, and an Iranian attack on Israel. The S&P 500 dropped roughly 3.15% in the past month – a big monthly drop.

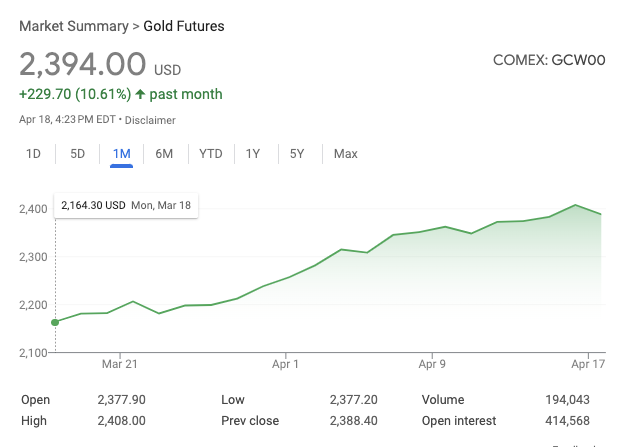

True to form, gold rose 10.6% in the chaos.

Source: Google

Bitcoin, meanwhile, dropped 6%.

Source: Google

I think by now, most of us knew this. Bitcoin doesn’t trade like an independent anything. It trades like just another meme stock, at least in times of crisis.

Featured Stock: WW Grainger

| Each week, BBAE publishes lists of investment ideas from various themes and screeners, like top stocks from the Piotroski Score, and top stocks on MarketGrader’s Growth Compounders list. In this section, we’re featuring a stock from these lists. All stocks in this section, and on our lists, are simply ideas for potential further research, and not presented as recommendations. |

One stock that’s not a meme stock is WW Grainger (NYSE: $GWW).

If you follow our Piotroski lists and our MarketGrader Growth Compounders lists, you may have noticed that WW Grainger has appeared on both lists in recent weeks.

I decided to take a look.

The $46 billion-market cap company makes what most people would see as boring industrial items, ranging from tools to ladders to pneumatic machinery to hard hats.

To me – and I’m a contrarian – “boring” is a feature, not a bug, in a stock, as it tends to keep the speculative (i.e., irrational) money at bay. Boring stocks tend to trade more on their actual economic fundamentals, relative to high-flying tech stocks or – heaven forbid – meme stocks, which usually have a large crowd psychology element mixed in.

Source: Company website

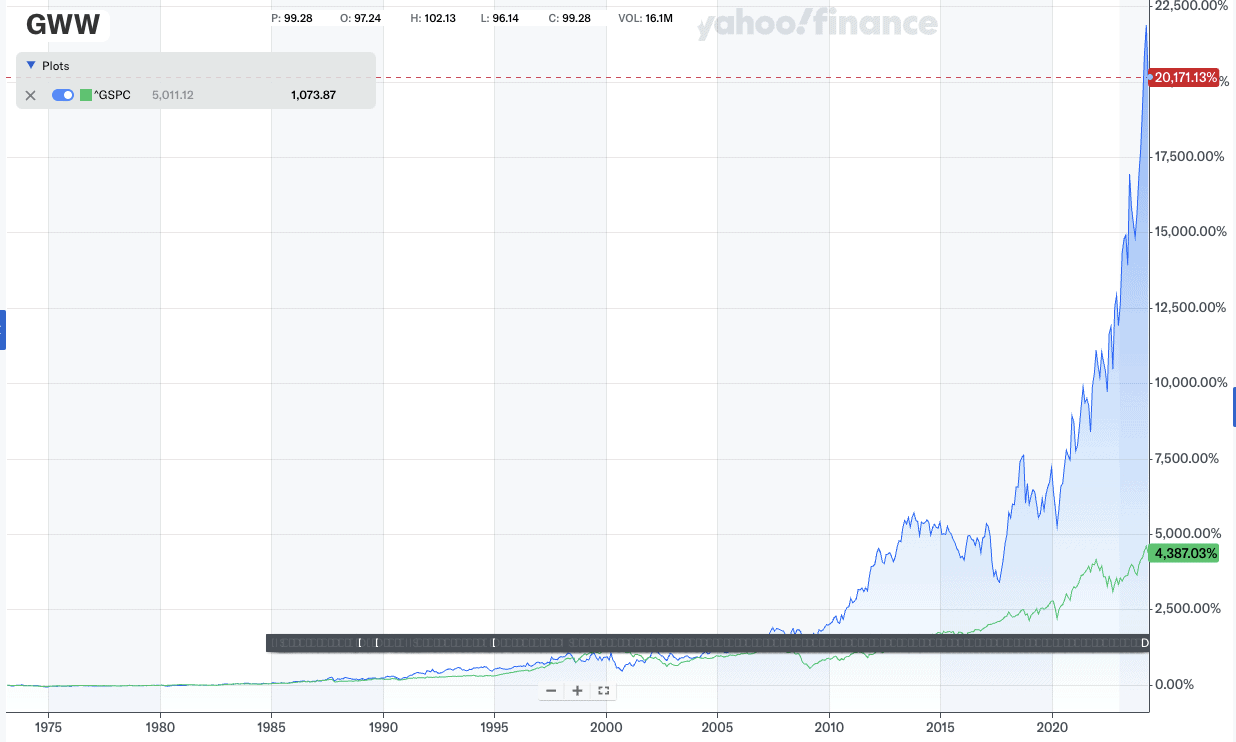

One thing that is not boring is the company’s stock performance (in blue below).

Though it’s slightly hard to see the green S&P 500 line, since WW Grainger went public a bit more than 50 years ago until today, it’s returned more than 20,000%, versus just 4,300% for the S&P 500.

Source: Yahoo! Finance

Whenever I see a meteoric-looking rise on a price chart, I worry about overvaluation. But looking at P/E (not the best way to value a company, but certainly the easiest), WW Grainger’s 25 ratio is roughly in line with the S&P 500’s which is currently 27.

Of course, P/E’s companion variable is earnings growth: All else equal, a faster-growing company should have a higher P/E.

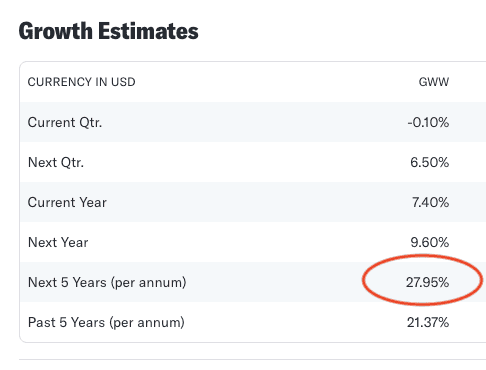

Checking on Yahoo! Finance, we see that the Wall Street analysts covering WW Grainger predict 28% annual earnings growth for the next five years:

Source: Yahoo! Finance

That rate is surprising for a relatively mature company. In fact, it makes WW Grainger’s PEG ratio (price to earnings divided by earnings growth) less than one. LIke P/E, PEG also isn’t the most ideologically sound way to value stocks, but PEG users will tell you that < 1 PEG stocks are hard to come by, and undervalued by that metric.

WW Grainger holds 6% global and 7% US market share per Morningstar; it’s surprisingly dominant in its industry (the maintenance, repair, and operations, or MRO, industry). In fact, Morningstar notes that it’s now the 11th largest e-retailer in the US.

The company, which sells more than 2 million SKUs (stock keeping units, which is industry-speak for individual products), notes on its investor relations page that it’s increased its dividend for 52 consecutive years now, which is generally considered a sign of shareholder-friendly stewardship.

Of course, all companies have risks, and WW Grainger’s biggest may be Amazon – specifically the encroachment of Amazon into the B2B MRO space.

I’d guess another is a US recession. I’m presuming that most of WW Grainger’s customers are small-to-medium-sized businesses, and those tend to sell mostly to the domestic market.

Looking at the stock chart, I certainly wish I’d bought shares in WW Grainger five or 10 years ago – and bet you do, too – but I have no position in the company and am not presenting any investment guidance on it.

As always, do your own research to decide which investments are right for your own portfolio.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. Neither the author nor BBAE has a position in any investment mentioned.