Senate Plan to End Solar Tax Credits Shakes U.S. Solar Stocks

The Senate has introduced a sweeping budget proposal that would phase out federal solar and wind tax credits by 2028—accelerating the timeline set under the Inflation Reduction Act. The Investment Tax Credit (ITC), which currently covers 30% of solar project costs, would be cut to 60% in 2026, 20% in 2027, and eliminated entirely by 2028. Meanwhile, tax incentives for nuclear, geothermal, hydro, and energy storage projects would remain in place through 2036.

This move signals a strategic pivot from intermittent renewables to “reliable baseload” energy sources, aligning with the Trump administration’s energy priorities. Though not yet law, the proposal has already triggered a steep selloff in solar stocks and introduced significant policy risk to the sector.

Market Fallout

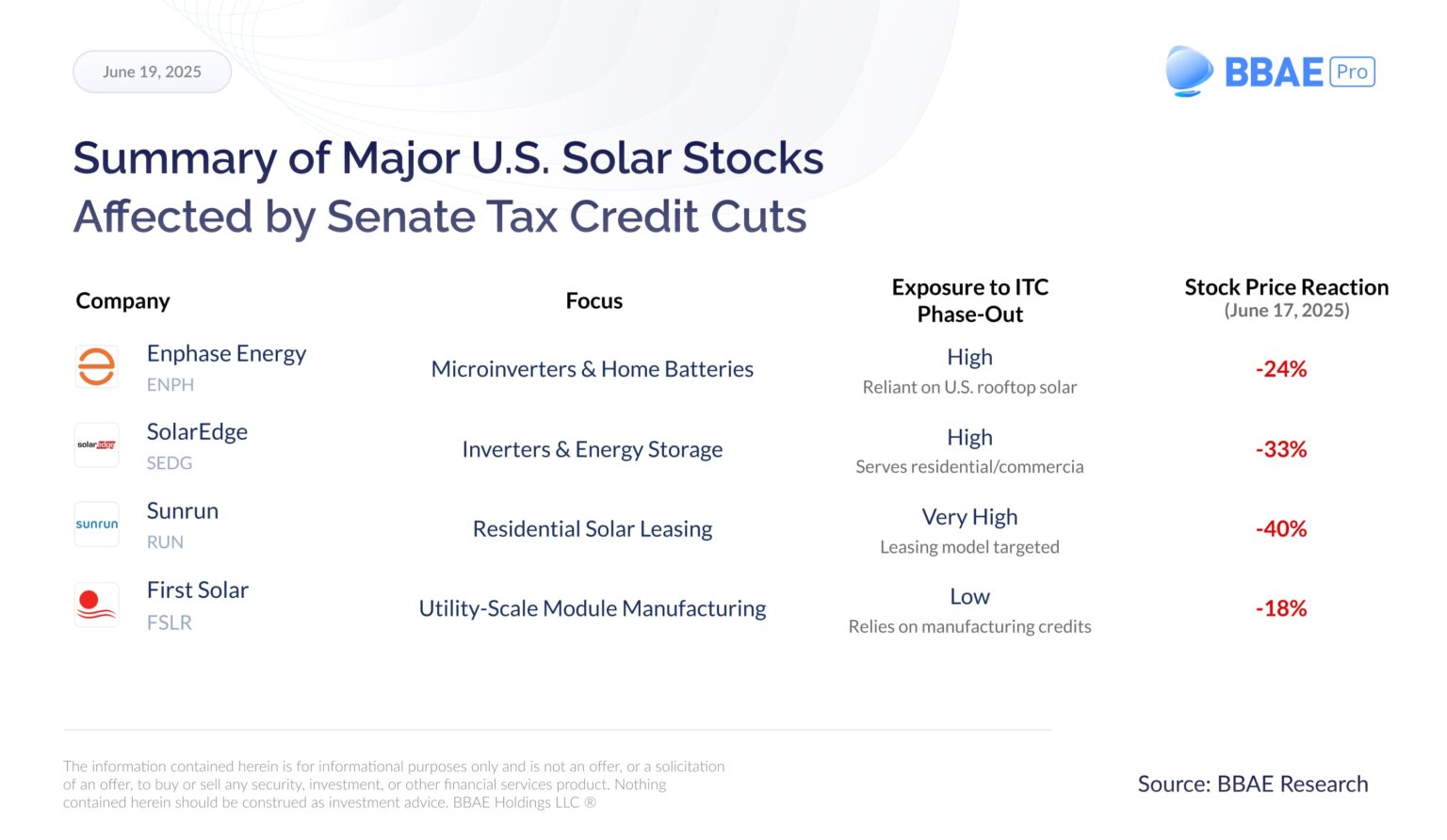

Investor reaction was immediate. Shares of Sunrun ($RUN) plunged 40%, SolarEdge Technologies ($SEDG) fell 33.4%, Enphase Energy ($ENPH) dropped 24%, and First Solar ($FSLR) declined 18%. Investors reacted so sharply because the Senate plan strikes at a central pillar of the industry’s growth model: federal tax credits have been critical in making solar projects financially viable. If those incentives are curtailed years earlier than expected, future profits and project pipelines for these companies could be dramatically lower than previously forecast.

Company-by-Company Impact

Enphase ($ENPH)

Enphase Energy is a top supplier of microinverters and residential energy storage systems. Its plug-and-play microinverter architecture has made it a popular choice for rooftop solar installations, particularly in the U.S. and Europe. The company has also expanded into home battery storage, enabling homeowners to pair solar with backup power.

ENPH’s business has historically benefited from robust U.S. residential solar demand, but that’s also its vulnerability, while it doesn’t directly benefit from the ITC—it sells hardware to installers—the company indirectly depends on it, since the credit has historically made rooftop solar more affordable and boosted hardware demand.

The proposed ITC rollback could lead to fewer residential installations in the U.S., directly impacting ENPH’s volume. Management had already cited policy uncertainty in April 2025 as a factor weighing on guidance.

SolarEdge ($SEDG)

SolarEdge provides DC optimizers, inverters, and residential battery solutions that compete with Enphase. It traditionally served both residential and commercial customers, and while it leads in centralized inverter architecture, its exposure to rooftop solar demand is significant.

SEDG suffered a brutal 2023–2024. Its stock fell nearly 90% from peak levels due to softening demand, high inventory, and severe losses. Q1 2025 offered signs of stabilization: revenue of $219 million beat estimates, gross margin turned positive at 8%, and the company generated $20 million in free cash flow.

Still, SolarEdge continues to operate at a loss (Q1 operating loss was $103 million) and is in recovery mode. It cut 900 employees in January 2025 and has shifted its focus to conserving cash.

The Senate proposal threatens to disrupt that recovery. About 62% of SolarEdge’s Q1 revenue came from the U.S., with 22% from Europe. A large share of its systems are installed via third-party ownership models, like leases and PPAs, which are directly targeted by the bill. If those models become ineligible for tax credits starting in 2026, SolarEdge could lose a significant portion of its residential market.

Sunrun ($RUN)

Sunrun is the largest residential solar installer in the U.S. and a pioneer in solar-as-a-service. Its model revolves around leasing rooftop systems to homeowners and monetizing federal tax credits through those agreements. In most cases, Sunrun retains ownership of the systems, collects the ITC, and passes savings to consumers via monthly payments.

That model is now under direct threat. The Senate bill proposes ending credits for leased systems in 2026—sooner and more decisively than for homeowner-purchased systems. This change strikes at the heart of RUN’s economics. If credits disappear, Sunrun would either have to raise prices or accept lower returns on its projects.

First Solar ($FSLR)

First Solar is the largest U.S.-based solar panel manufacturer, specializing in cadmium telluride (CdTe) thin-film modules used primarily in utility-scale solar projects. Unlike its peers, FSLR doesn’t target the residential market and doesn’t rely on the ITC to drive customer demand. Instead, it benefits from Section 45X manufacturing credits—payments it receives per watt of solar capacity produced in the U.S.

Those manufacturing credits, which run through 2031, remain intact in the Senate’s draft. This gives First Solar a significant advantage: its financial support comes directly from federal industrial policy rather than customer-side incentives.

The Senate bill could eventually reduce demand from developers if utility-scale projects lose access to the ITC, but First Solar’s current pipeline and manufacturing support provide a strong buffer. The company also benefits from anti-China trade provisions, as it uses a fully U.S.-based supply chain.

FSLR’s 18% stock drop reflects overall sector sentiment, not specific weakness.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investment involves inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Always conduct thorough research or consult with a financial expert before making any investment decisions. BBAE has no position in any investment mentioned.