Financial Stocks Under Pressure After 10% Credit Card Rate Cap Proposal

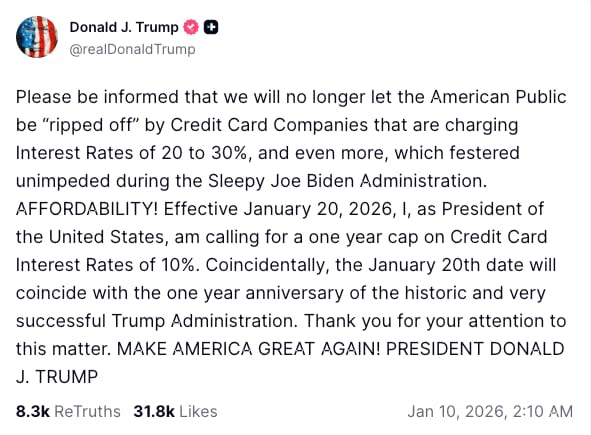

President Donald Trump announced last week that he plans to impose a one-year cap of 10% on credit card interest rates, effective January 20, 2026. The proposal is framed as a way to prevent Americans from being overcharged by credit card rates that often reach 20% to 30%. If implemented, the cap would sharply reduce interest income for card lenders, as average credit card APRs stood near 21% in late 2025. The policy is intended to ease the burden on consumers facing record levels of credit card debt, which reached $1.17 trillion in 2024, but it would significantly pressure issuer profitability. Markets reacted quickly to the announcement, with shares of major credit card lenders falling roughly 8% to 11% in the immediate aftermath. In this article, we examine the impact across different parts of the industry, including card issuers, payment networks, and consumer-focused fintech lenders, and break down which companies are most exposed.

Credit Card Issuers (Banks and Lenders)

Credit card issuers, including banks and consumer finance companies that lend directly to cardholders, would be the most exposed to a 10% interest rate cap. These firms typically charge some of the highest rates in consumer finance, often between 18% and 25% APR or higher. A legal ceiling at 10% would significantly compress interest income and, in some cases, could make card portfolios unprofitable. Wall Street analysts estimated that such a cap could reduce large bank earnings by roughly 5% to 18%, while profits at card focused lenders could be nearly wiped out. Markets reflected this risk immediately, with shares of several major issuers falling sharply following the announcement.

Below are the key publicly traded U.S. issuers with market capitalizations above $1 billion and how they may be affected.

Capital One Financial ($COF)

Capital One is one of the largest credit card issuers in the U.S. and relies heavily on interest income from revolving card balances, particularly among consumer and subprime borrowers. A 10% cap would materially reduce revenue from its card portfolio and could turn a profitable business into a loss making one. Analysts warned that lenders like Capital One could see profits effectively eliminated under the cap. Reflecting these concerns, $COF shares fell about 9% after the announcement.

Synchrony Financial ($SYF)

Synchrony specializes in store branded credit cards and installment financing for major retailers such as Amazon and Lowe’s. Its business model depends largely on interest income from retail card balances, which typically carry higher APRs. A 10% cap would sharply reduce Synchrony’s interest yield, putting significant pressure on earnings. The stock dropped roughly 10% on the news, as investors priced in a major hit to profitability. Analysts noted that for pure card lenders like Synchrony, the cap could wipe out most earnings during the capped period.

American Express ($AXP)

American Express serves a more affluent customer base and generates revenue from a mix of card interest, annual fees, and merchant discount fees. While many Amex customers pay balances in full, the company does offer revolving credit products that would be affected by the cap. The impact on American Express is likely more moderate than for other issuers due to its diversified revenue streams. AXP shares fell around 3% to 4% following the announcement, suggesting investors see a smaller relative hit. Still, interest margins would be reduced, and Amex could tighten lending to higher risk borrowers.

Bread Financial ($BFH)

Bread Financial, formerly Alliance Data, provides private label and co-branded credit cards through retail partners, including its Comenity Bank platform. These store cards typically carry high APRs, making the business particularly vulnerable to a rate cap. A 10% ceiling would directly pressure Bread’s earnings, and the stock fell roughly 8% to 11% after the news. As a smaller, specialized issuer, Bread Financial may be forced to reduce exposure to higher risk customers to preserve margins.

Major Diversified Banks ($JPM, $BAC, $C, $WFC)

Large U.S. banks such as JPMorgan Chase, Bank of America, Citigroup, and Wells Fargo each operate sizable credit card businesses as part of broader consumer banking operations. A 10% cap would reduce interest income from cardholders and weigh on consumer banking revenue. However, because these banks are highly diversified, the relative impact is smaller than for pure card issuers. Shares of major banks declined a more modest 2% to 5% following the announcement. Among them, Citigroup has one of the highest exposures to credit cards as a share of total loans, meaning it could feel the impact more acutely. Overall, large banks are likely to absorb the shock, though card profitability would decline and lending standards may tighten, particularly for riskier borrowers.

Credit Card Networks (Visa and Mastercard)

Visa and Mastercard operate the payment networks that process card transactions but do not lend directly to consumers. Their revenue is generated primarily from transaction and processing fees rather than interest income, meaning a 10% cap on credit card APRs does not directly reduce their earnings. Even so, both stocks fell roughly 5% following the announcement, suggesting investors are factoring in potential second-order effects rather than direct exposure. Those indirect impacts could include slower transaction growth if banks respond by tightening credit availability or reducing credit limits, particularly for higher-risk customers. On the other hand, lower interest rates could encourage some consumers to use credit cards more actively, supporting transaction volumes. Overall, the proposed cap does not change the core business models of Visa or Mastercard, and their long-term growth drivers, including the ongoing shift from cash to digital payments, remain intact. The market reaction appears to reflect broader uncertainty around issuer behavior rather than a fundamental threat to the networks’ economics.

Bottom Line

The proposed 10% credit card interest rate cap poses the greatest risk to credit card issuers, particularly those that rely heavily on high interest revolving balances for profitability. These companies may respond by tightening credit standards, reducing rewards, or increasing fees to offset lost interest income. Payment networks like Visa and Mastercard appear largely insulated and could even see modest benefits if lower borrowing costs support higher card usage.

If implemented, the cap would represent a rare policy experiment in U.S. consumer credit. For retail investors, the key will be watching how companies adapt through changes in underwriting, product mix, and pricing strategies. While legal and political challenges may still shape the policy’s outcome, market reactions so far suggest investors are already differentiating clearly between the most exposed issuers and those positioned to weather or benefit from a lower rate environment.