Ethos Technologies ($LIFE) IPO: Everything You Need to Know

Ethos Technologies Inc. is preparing to go public and has started marketing its IPO. The offering is expected to include just over 10.5 million shares, split between new shares issued by the company and shares sold by existing investors. The proposed price range is $18 to $20 per share, and the stock is expected to trade on the Nasdaq under the ticker symbol $LIFE. In this article, we review the company’s S-1 filing to outline its business model, financial performance, and key considerations for investors.

Business Model and Revenue Streams

Ethos operates a three-sided technology platform that connects consumers, insurance agents, and insurance carriers. Each group plays a distinct role in how policies are distributed and underwritten through the platform.

Consumers

Ethos offers a fully digital life insurance application and underwriting experience. Applicants typically complete the process online by answering a limited number of health-related questions, often without medical exams, and receive a coverage decision within minutes. According to the company, roughly 95 percent of applicants receive an instant underwriting decision, compared with traditional life insurance processes that can take several weeks. The streamlined process is designed to make life insurance easier and faster to obtain.

Insurance agents

For licensed agents and agencies, Ethos provides an integrated operating system that brings quoting, applications, and policy management into a single platform. Much of the administrative work is automated, and commissions are paid out quickly, allowing agents to spend more time on sales and client relationships. As of mid-2025, more than 10,000 active agents were using Ethos’s platform, suggesting growing adoption among insurance professionals.

Insurance carriers

Ethos partners with established life insurance carriers that issue the policies and assume the insurance risk. Ethos handles digital distribution and underwriting, helping carriers reach new customers and agents more efficiently. Its underwriting engine evaluates up to 250,000 data points per application, including prescription history, credit-based insurance scores, and motor vehicle records, to assess risk and deliver instant decisions. In many cases, carriers rely on Ethos to administer underwriting under agreed guidelines. Ethos does not take insurance risk onto its balance sheet and operates as a capital-light technology and distribution platform.

Revenue Model

Ethos generates revenue through commissions paid by insurance carriers on policies sold via its platform. These commissions are typically calculated as a percentage of the policy premium. While Ethos negotiates commission rates with its carrier partners, premium pricing is determined by the carriers based on actuarial models and regulatory requirements. As a result, changes in carrier pricing, commission structures, or regulatory conditions can affect Ethos’s revenue.

Because Ethos does not underwrite insurance or hold capital against insurance liabilities, its model is designed to scale without the balance sheet constraints faced by traditional insurers. Growth is driven primarily by increases in policy volume, agent adoption, and carrier participation rather than underwriting margins.

Ethos’s business centers on digitizing life insurance distribution. Consumers benefit from a faster and simpler purchasing experience, agents gain tools that reduce administrative burden and improve efficiency, and carriers gain access to digital distribution and data-driven underwriting. Ethos sits in the middle of this ecosystem, earning commission-based revenue while remaining capital-light and avoiding direct insurance risk.

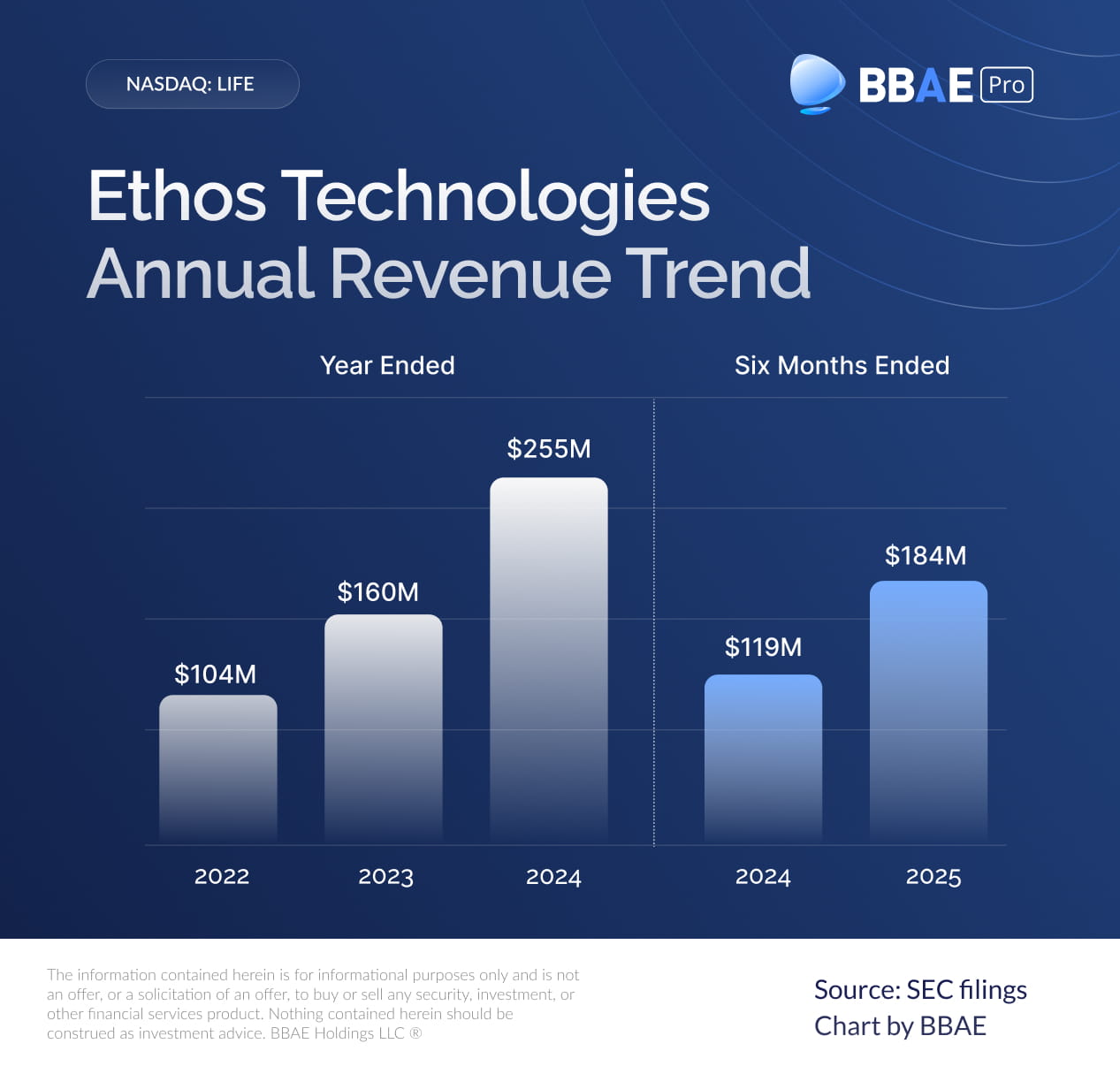

Financial Performance and Growth

Ethos’s IPO filings show a company that has scaled quickly while improving profitability over a relatively short period. Revenue increased from $160 million in 2023 to $255 million in 2024, representing year-over-year growth of roughly 60 percent. That growth was largely driven by higher policy volume, with activated policies rising from about 72,000 in 2023 to nearly 128,000 in 2024, a 77 percent increase.

Margins remained high throughout this period. Gross profit margins were 96 percent in 2023 and improved slightly to 97 percent in 2024, reflecting Ethos’s commission-based, asset-light model. Because insurance carriers bear the underwriting risk and claims costs, Ethos’s cost structure is primarily tied to operations, technology, and marketing rather than insurance liabilities.

Profitability also improved meaningfully. Net income margin expanded from roughly 1 percent in 2023 to 19 percent in 2024, marking a sharp shift from near break-even results to sustained profitability. Adjusted EBITDA margin rose from 4 percent to 23% over the same period, indicating improving operating leverage as revenue scaled. The company notes in its filings that while it has recently reached profitability, results may vary by quarter as growth continues.

Momentum carried into 2025. For the first six months of the year, Ethos reported revenue of $184 million, up 55 percent from $119 million in the comparable period of 2024. Net income margin during the period was approximately 17 percent, slightly higher than the prior year, while adjusted EBITDA margin reached 24 percent. These figures suggest that as volumes increase, a larger share of revenue is flowing through to the bottom line.

Ethos attributes this operating leverage to higher contribution margins and platform efficiencies. Contribution margin increased from 32 percent in 2023 to 41 percent in 2024, reflecting lower average costs per policy as the platform scaled. According to the company, higher data volume and repeat usage improve underwriting accuracy and marketing efficiency, reducing acquisition costs over time.

Since inception, Ethos has facilitated more than 450,000 life insurance policies sold through its platform. The company has also expanded its product lineup, growing from a single product in 2019 to ten insurance and estate-planning products by the end of 2024, including term life, whole life, indexed universal life, and estate planning services. This broader offering has helped increase average revenue per user and expand the addressable market.

Other Notable Highlights from the IPO Filing

Beyond financial performance, Ethos’s filings highlight several structural and strategic factors relevant to public investors.

The company will operate with a dual-class share structure after the IPO. Founders and insiders will hold shares with significantly higher voting power, allowing them to retain control over corporate decisions even after the company goes public. As a result, a relatively small group of insiders and early investors will control a majority of the voting rights, limiting the influence of public shareholders on matters such as board elections and strategic transactions.

Revenue concentration is another key consideration. Ethos currently relies on a small number of insurance carrier partners, with three carriers accounting for approximately 98 percent of total revenue in both 2023 and 2024. While the company plans to expand its carrier relationships, this level of concentration means changes in partner relationships or commission terms could materially affect revenue and growth.

Ethos also frames its strategy around a large unmet market opportunity. According to the company’s filings, a significant portion of U.S. adults who believe they need life insurance have not purchased coverage, often due to complexity or inconvenience. Ethos’s digital model is designed to address this gap by offering faster underwriting and simpler access to coverage. The company notes that its customer base spans a wide range of ages, income levels, and educational backgrounds, suggesting that the platform may be reaching segments historically underserved by traditional insurance distribution.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investments involve inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Investing in initial public offerings (IPOs) carries additional risks, such as volatility, limited operating history, lack of liquidity, and potential overvaluation. IPO stocks may experience significant price fluctuations and may not perform as expected. Always conduct thorough research or consult with a financial expert before making any investment decisions. BBAE has no position in any investment mentioned.