Chime ($CHYM) IPO: Everything You Need to Know

Chime Financial, the San Francisco-based fintech disruptor known for its fee-free banking services, has officially filed for an initial public offering (IPO) on the Nasdaq under the ticker symbol “CHYM.” The company’s S-1 filing offers a detailed look into its financial health, growth trajectory, and strategic initiatives as it aims to solidify its position in the digital banking sector.

Chime Overview: Business Model & Core Offerings

Chime is a fintech company targeting U.S. consumers who are often underserved by traditional banks (primarily “everyday Americans”). It offers no-fee banking services via a mobile app, partnering with FDIC-insured banks (Bancorp Bank and Stride Bank) rather than operating as a traditional bank.

Its main products include checking accounts (Spending Accounts), high-yield savings, and tools like:

- Get Paid Early (early paycheck access)

- SpotMe (fee-free overdrafts)

- Credit Builder (a secured credit card to build credit)

Chime doesn’t charge monthly, overdraft, or minimum balance fees. Instead, it earns primarily from interchange fees—a portion of what merchants pay when users swipe their Chime cards. Because it partners with smaller banks, Chime qualifies for higher interchange rates.

In 2023, Chime’s card purchase volume reached $92.4 billion, with 70% spent on essentials like groceries and gas—indicating it’s often used as a primary account. Additional revenue comes from optional services like:

- MyPay (on-demand paycheck access, free or with a small fee)

- Out-of-network ATM fees

- Partner interest-sharing from deposits

Products like MyPay ($8.8B accessed in 9 months) and SpotMe ($43.3B since 2019) deepen engagement. Chime has also added bill pay, peer-to-peer transfers, credit score tracking, cash-back offers (Chime Deals), and a beta tax service.

In 2025, Chime introduced Chime+, a free premium tier for users with direct deposit, offering perks like higher savings rates (3.75% vs 2.00%), priority support, and exclusive deals.

Chime’s strategy centers on becoming users’ primary spending account. Today, 67% of its 8.6 million active users use Chime this way, averaging 54 transactions per month.

In short, Chime delivers free, digital-first banking, earns through card usage and partnerships, and grows by aligning its success with that of its users—“profiting with them, not from them.”

Financial Performance & Key Metrics

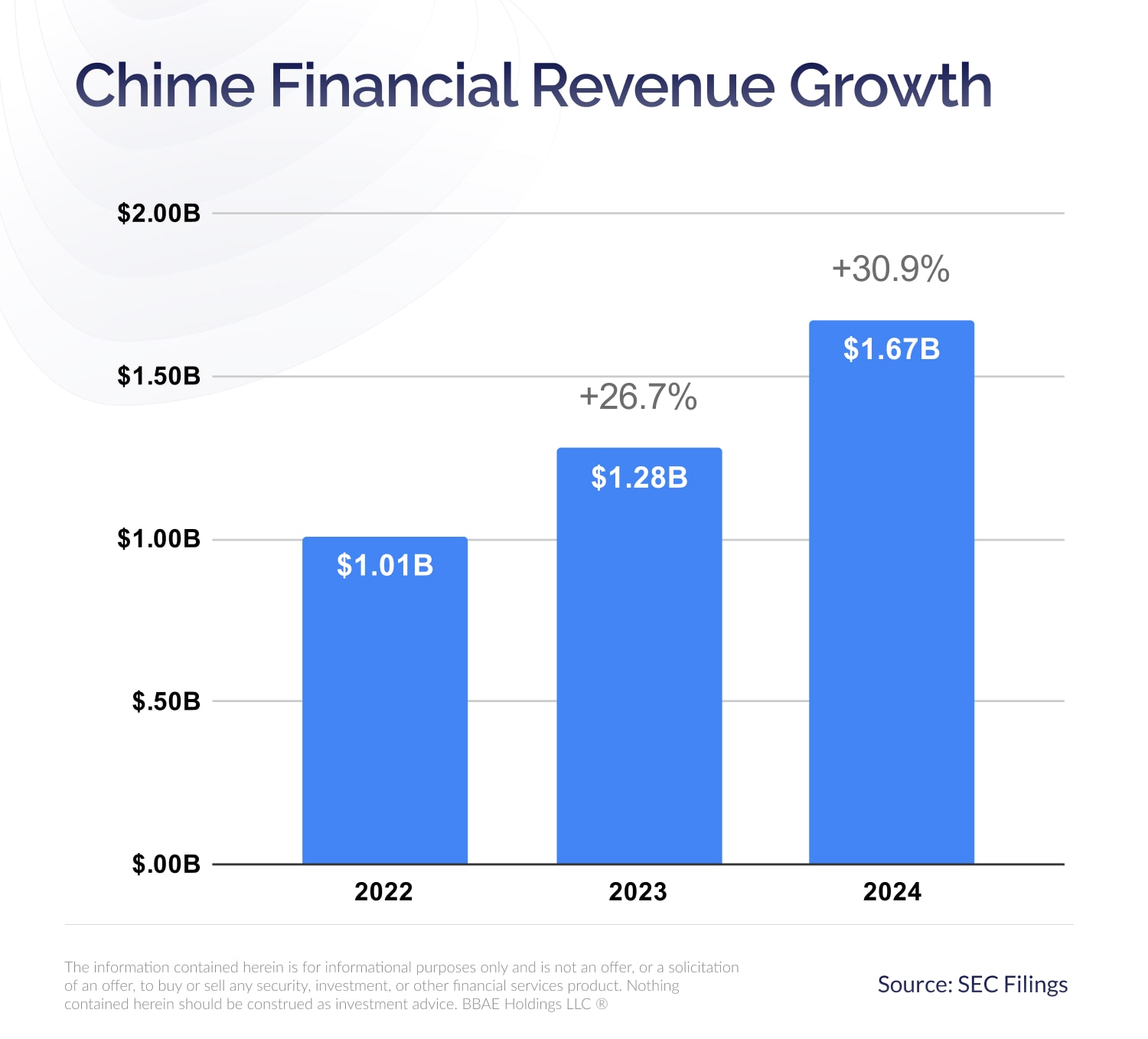

Chime has shown strong revenue growth and improving profitability. Revenue rose from $1.01 billion in 2022 to $1.67 billion in 2024 (+66%), driven by more active users and increased spending per user. In Q1 2025, revenue hit $518.7 million, up 32% year-over-year—boosted by new products like MyPay, which nearly doubled platform-related revenue.

Net losses have narrowed sharply:

- 2022: -$470M

- 2023: -$203M

- 2024: -$25M

- Q1 2025: +$12.9M net income

User metrics:

- 8.6M active members as of March 2025 (+23% YoY)

- ARPAM (Average Revenue per Active Member): $251 (annualized), up from ~$212 in 2023

- Users average 54 transactions/month and use ~3.3 Chime products.

Strategic Initiatives & Growth Plans

Chime’s growth strategy centers on deepening member engagement, expanding its product suite, and boosting monetization per user — primarily through increasing ARPAM.

Product Expansion & Monetization

In mid-2024, Chime launched MyPay, an earned wage access tool that both adds user value and generates revenue through optional instant fees. Chime also introduced ChimeCore, its in-house payment and ledger system, giving it better control over product development and transaction costs.

To further drive usage and retention, Chime launched Chime+ in March 2025, a free loyalty tier offering perks like higher savings rates for members with direct deposit. These features aim to make Chime the user’s primary financial account — increasing transaction volume and cross-sell potential.

Chime reports users who engage with 6+ products generate ~$442 in ARPAM vs. ~$251 overall, highlighting the importance of expanding product usage.

AI & Automation

Chime is increasingly integrating AI and machine learning to improve operations and reduce costs:

- Fraud & Risk Management: AI models cut fraud losses by 29% from 2022 to Q1 2025.

- Customer Support: AI chatbots helped reduce support cost per user by 60% without hurting satisfaction.

- Future Use Cases: Chime is exploring generative AI for financial planning, personalization, and smarter risk models.

AI also supports Chime’s scalability, allowing it to serve a growing user base with a lean team. However, Chime acknowledges regulatory and ethical risks tied to AI use.

Conclusion

Chime’s IPO aims to raise capital to support continued growth and provide liquidity through a public market listing, while its dual-class structure ensures the founders retain control. The proceeds are expected to strengthen the balance sheet and fund expansion—not for any one-off use.

Backed by reputable underwriters and a large, engaged user base, Chime is positioned as one of the most closely watched fintech IPOs since the 2021 cycle. It offers a compelling growth story: a digital-first banking platform with improving financials and strong product engagement.

That said, Chime operates in a competitive and highly regulated environment. Retail investors should carefully consider the company’s fundamentals and risk factors detailed in the S-1 before investing.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. All investments involve inherent risks, including the total loss of principal, and past performance is not a guarantee of future results. Investing in initial public offerings (IPOs) carries additional risks, such as volatility, limited operating history, lack of liquidity, and potential overvaluation. IPO stocks may experience significant price fluctuations and may not perform as expected. Always conduct thorough research or consult with a financial expert before making any investment decisions. BBAE has no position in any investment mentioned.