Forgent ($FPS) IPO: The Infrastructure Company Behind Data Center Power

Forgent Power Solutions is heading to the public markets as demand for data center and power infrastructure continues to surge. The Minnesota-based company, which makes electrical distribution equipment used in data centers, utility grids, and large industrial facilities, has filed to list its Class A shares on the NYSE under the ticker $FPS.

Forgent began its IPO roadshow in January 2026 and plans to sell about 56 million shares in total, with roughly 16.6 million new shares issued by the company and 39.4 million sold by existing shareholders. At the proposed $25–$29 per share range, the deal could raise around $1.5 billion and value the business at over $8 billion. Below is a breakdown of what the company does, how it makes money, and what stands out from its S-1 filing for retail investors evaluating the IPO.

Business Model and Revenue Streams

What Forgent does.

Forgent builds the hardware that moves electricity from the grid or on-site generation to where it’s actually used. That includes equipment found inside data centers, utility substations, factories, and large commercial buildings. Its product lineup ranges from automatic transfer switches and transformers to switchgear, power distribution units (PDUs), generator connection cabinets, electrical houses (eHouses), and prefabricated power skids. Importantly, no single product category represents more than 13% of revenue, suggesting the company is not dependent on one specific piece of equipment.

Heavy tilt toward custom-built projects.

Rather than relying mainly on catalog products, Forgent focuses on custom-engineered systems built for specific customer projects. The company groups its business into Standard Products, Custom Products, and Powertrain Solutions. Standard Products are more off-the-shelf, while Custom Products are engineered-to-order and often designed in close collaboration with customers. Powertrain Solutions bundle multiple custom products into integrated systems, frequently delivered as prefabricated modules such as skids or eHouses. Forgent also earns service revenue from commissioning and maintaining these systems once installed.

This approach tends to favor performance, reliability, and delivery speed over being the lowest-cost option. According to the S-1, Forgent is often brought into projects early in the design phase, which can lead to deeper customer relationships and stickier demand.

Where the money comes from.

Custom work dominates Forgent’s revenue base. In fiscal 2025:

- ~78% of revenue came from Custom Products

- ~13% came from Powertrain Solutions

- ~5% came from Standard Products

- ~4% came from services

That means about 91% of revenue was tied to engineered-to-order solutions. The company notes that these offerings generally carry higher margins than standard catalog equipment. Forgent also manufactures many critical components in-house, including transformers, which can help with cost control and supply-chain reliability.

End markets tied to major infrastructure spending.

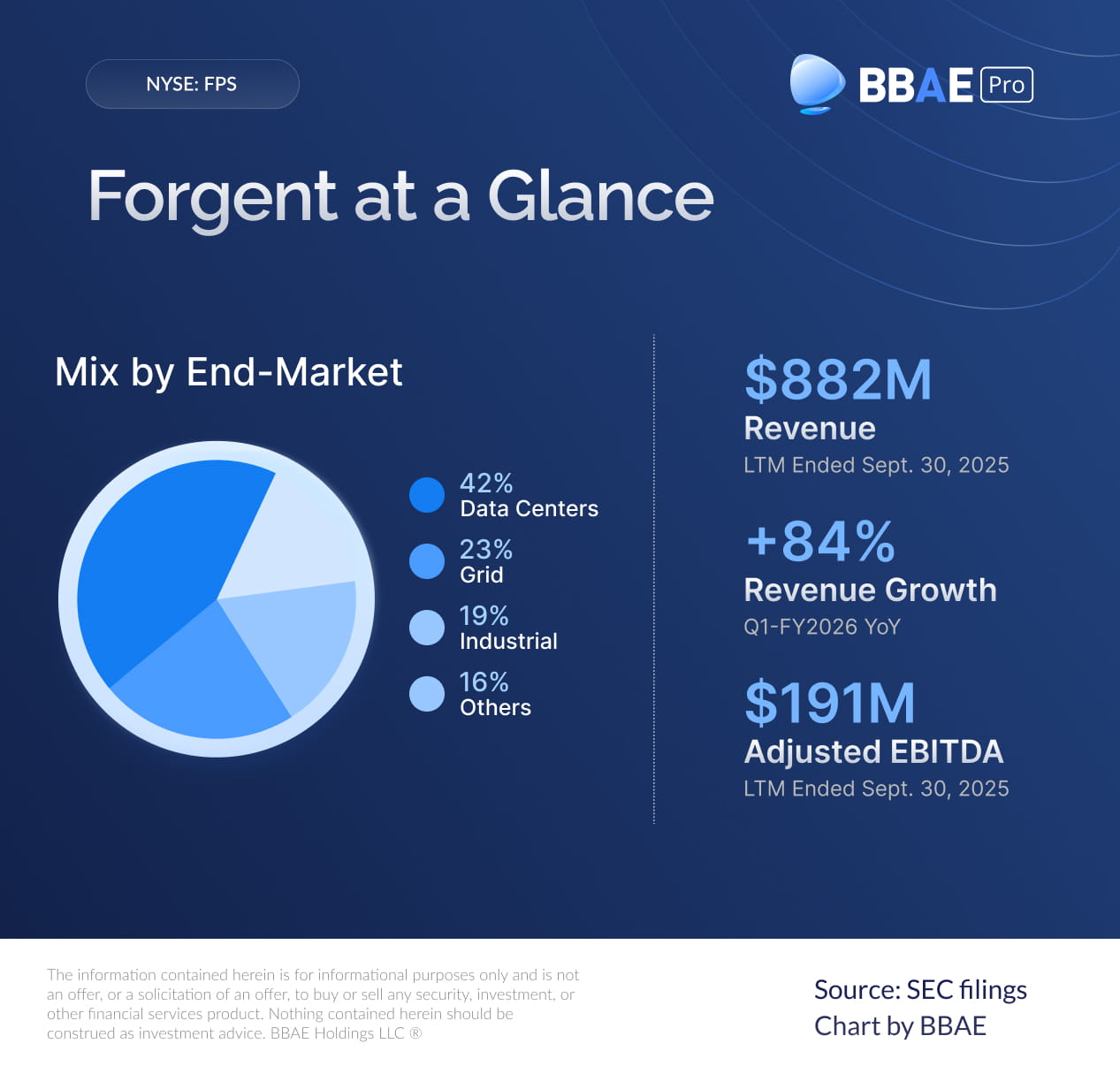

Forgent primarily serves three end markets:

- Data Centers: ~42% of FY2025 revenue

- Grid infrastructure (utilities & power generation): ~23%

- Industrial facilities: ~19%

Together, these markets represented 84% of total revenue in fiscal 2025. The S-1 points to strong long-term demand drivers, including cloud computing and AI workloads, grid modernization, electrification, and factory expansions. Management highlights that U.S. data center investment has grown much faster than overall non-residential construction in recent years, and expects double-digit growth rates for electrical distribution equipment in these markets through 2030.

Manufacturing footprint and capacity.

Forgent operates 10 manufacturing campuses across the U.S. and Mexico and employed around 2,000 full-time workers as of September 2025. Most revenue currently comes from North America. Management says capacity expansion projects launched in 2023 should allow the company to triple FY2025 production volumes by 2026, supporting up to $5 billion in annual revenue without major additional capital spending. For investors, this suggests Forgent is building scale ahead of demand and could handle higher order volumes without a proportional increase in costs.

Financial Performance and Growth

Forgent reported $753.2 million in revenue in fiscal 2025, up 56% from pro forma revenue of about $482.7 million in fiscal 2024. Growth accelerated into fiscal 2026. In the first quarter (ended September 2025), revenue reached $283.3 million, an 84% year-over-year increase.

Management attributes the growth primarily to higher shipments of custom electrical equipment for data center builds, grid projects, and industrial facilities.

The order book also points to continued momentum. As of September 30, 2025, Forgent reported backlog of $1.03 billion, up 44% year over year. That backlog is larger than the company’s entire FY2025 revenue, giving visibility into future sales, though actual timing depends on customer project schedules.

Profitability is improving alongside scale.

- Forgent’s adjusted profitability has expanded as revenue has grown.

- Adjusted EBITDA: $169.2 million in FY2025 vs. $99.2 million in FY2024

- Adjusted EBITDA margin: 22.5% in FY2025 vs. ~20.6% in FY2024

- Adjusted net income: $88.7 million in FY2025 vs. $33.5 million in FY2024

Market Outlook and Key Growth Drivers

Data centers remain the largest driver.

Data center projects accounted for 42% of FY2025 revenue, making this Forgent’s most important end market. Data centers require large amounts of electrical distribution equipment and typically build redundancy into their power systems, which increases equipment intensity per project.

The S-1 cites industry forecasts calling for strong growth in data-center-related electrical equipment demand through 2030, supported by cloud expansion and rising AI workloads. For investors, this positions Forgent as a picks-and-shovels play on AI and digital infrastructure spending.

The flip side is concentration risk. If data center construction slows meaningfully, Forgent’s growth rate could be affected.

Grid modernization and power generation.

About 23% of FY2025 revenue came from utility transmission & distribution and power generation projects. Utilities are upgrading aging infrastructure, adding renewable generation, and expanding capacity to meet rising electricity demand. These projects typically require transformers, switchgear, and control equipment—core products for Forgent.

This end market provides a steadier, longer-cycle source of demand compared with data centers, which can be more cyclical.

Industrial expansion and reshoring.

Industrial customers represented 19% of FY2025 revenue. The company points to trends such as U.S. manufacturing reshoring, factory expansions, and increased use of on-site generation and energy storage. These projects tend to be complex and customized, aligning well with Forgent’s engineering-heavy model.

Bottom line

Forgent is positioned in multiple areas seeing elevated infrastructure spending: data centers, power grids, and industrial facilities. The company is growing rapidly, margins are improving, and backlog is at record levels.

At the same time, this is a capital equipment business tied to construction and large projects. Economic slowdowns, project delays, or pullbacks in data center investment could create volatility in results.

This article is for informational purposes only and is neither investment advice nor a solicitation to buy or sell securities. The information contained herein does not take into account any investor’s specific financial situation, investment objectives, or risk tolerance.

Certain information included in this article is derived from the issuer’s registration statement and other publicly available filings. Such information has not been independently verified. Statements regarding future performance, growth prospects, backlog, capacity expansion, or market trends are forward-looking in nature and are subject to risks, uncertainties, and assumptions that could cause actual results to differ materially from those expressed or implied.

All investments involve inherent risks, including the possible loss of principal, and past performance is not indicative of future results. Investing in initial public offerings (IPOs) involves additional risks, including price volatility, limited operating history, limited public float, lock-up expirations, lack of liquidity, and the possibility that an active trading market may not develop or be sustained following the offering. IPO securities may experience significant price fluctuations and may not perform as expected.

Investors should conduct their own due diligence and consider consulting a qualified financial professional before making any investment decisions. BBAE has no position in any investment mentioned.